Good Thursday AM from your Hometown Lender,

Yesterday, bonds drifted lower on the day from their best levels reached after the US and Iran reached a two-week cease-fire. Mortgage bonds steadily lost ground as the day went on, although they staged a late-day recovery to end flat. Rates today are bouncing between gains and losses, as optimism over the US-Iran cease-fire fades with both sides accusing each other of violating it. Rates are not in danger of moving much today, but we could see continued selling, which would put pressure on bonds and rates

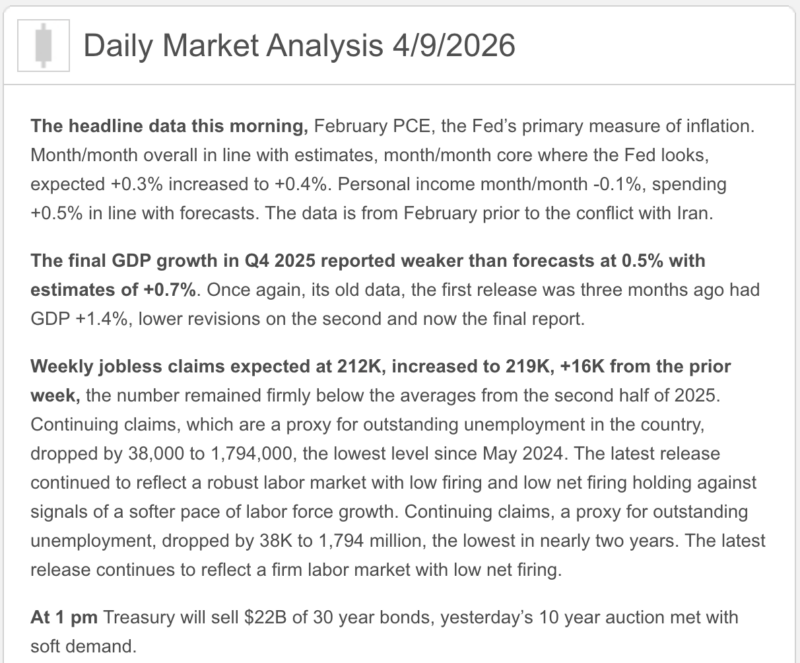

This morning’s PCE inflation data for February came in as expected, with core year-over-year at 3.0% (about 1% higher than the Fed wants to see). This data was before the conflict with Iran started, and doesn’t include any of the energy shock that is expected with the jump in oil prices and gas.

Market Analysis – From a higher and better view:

Quick Snapshot of Market Analysis

- Today’s big release was PCE, and it did not exactly hand the bond market a cupcake. February headline PCE rose 0.4% month over month and 2.8% year over year, while core PCE also rose 0.4% month over month and 3.0% year over year. Consumer spending increased 0.5%, but real spending rose only 0.1%, which tells you some of that “strength” was just higher prices wearing a fake mustache.

- Jobless claims rose to 219,000 for the week ended April 4, but that is still a low level historically, and continuing claims fell to 1.794 million, the lowest since May 2024. Bottom line: layoffs are not surging, so the labor market still is not giving the Fed a reason to rush.

- Q4 GDP was revised down to 0.5% annualized from 0.7%, and consumer spending in Q4 was revised to 1.9% from 2.0%. So the economy is still moving, but the engine is not exactly purring.

- The Fed’s target range remains 3.50% to 3.75%, and yesterday’s minutes showed a growing group of policymakers thought rate hikes might need to stay on the table if inflation remains too sticky.

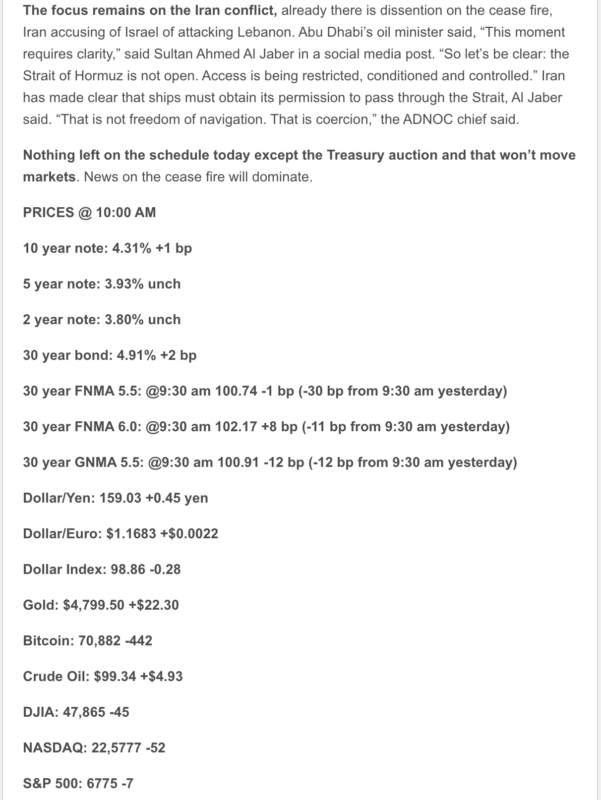

- Stocks were slightly lower late morning, with the Dow down 0.11%, S&P 500 down 0.09%, and Nasdaq down 0.21% at 10:04 a.m. ET. The 10-year Treasury was around 4.31%, and oil was back near $100 as markets questioned how durable the Iran ceasefire really is.

- Mortgage rates remain elevated. Freddie Mac’s latest weekly survey still has the 30-year fixed at 6.46% and the 15-year fixed at 5.77%. MBA’s more recent weekly survey showed the 30-year contract rate at 6.51%, with refis down 2.8% and purchase apps up just 1% week over week and still 7% below last year.

1) Market Analysis – What Hit This Morning

This morning was a PCE + claims + GDP revision cocktail, and it came with a spicy aftertaste. February PCE showed inflation still running hotter than the Fed wants, especially on the monthly core reading. At the same time, claims rose a bit but remained low, while Q4 GDP got revised lower. That is basically the market’s least favorite combo: slower growth but not enough disinflation.

PCE details:

- Personal income: -0.1%

- Disposable personal income: -0.1%

- Consumer spending: +0.5%

- Real consumer spending: +0.1%

- Headline PCE: +0.4% MoM, +2.8% YoY

- Core PCE: +0.4% MoM, +3.0% YoY

Narrative you can use:

“Today’s data told the market inflation is still sticky enough to keep the Fed cautious, even as economic growth looks softer under the hood. That is not a recession headline, but it is also not the kind of report that usually leads to quick mortgage-rate relief.”

2) Fed Watch

The Fed is still on hold at 3.50% to 3.75%, and the March statement said economic activity has been expanding at a solid pace while inflation remains somewhat elevated.

What changed yesterday was tone. The March 17–18 minutes showed some participants wanted the statement to more clearly acknowledge that upward adjustments in rates could be appropriate if inflation stayed above target. Reuters also reported that many participants were worried prolonged higher oil prices could keep inflation elevated for longer, while most participants still thought a long Middle East conflict could eventually weaken growth enough to justify cuts later. In other words, the Fed is now staring at both sides of the problem at once.

3) Market Analysis – Where Mortgage Rates Actually Are

Freddie Mac’s latest weekly survey, still the cleanest broad consumer benchmark, shows the 30-year fixed at 6.46% and the 15-year fixed at 5.77% as of April 2.

MBA’s weekly application survey, which is more current but narrower, showed the 30-year contract rate at 6.51% for the week ended April 3. Refi applications fell 2.8%, purchase applications rose only 1%, and purchase demand was still 7% lower than a year ago. That tells you the spring market is alive, but it is not exactly breakdancing.

The bigger point: mortgage pricing is still being driven more by Treasury yields, inflation expectations, oil, and geopolitical risk than by “maybe the Fed cuts later.” That story remains very much intact today.

4) Housing Market Check

The latest existing-home sales report showed February sales at a 4.09 million annual pace, up 1.7% month over month. Inventory rose to 1.29 million homes, which equals 3.8 months of supply, and the median price was $398,000, up 0.3% year over year.

One of the more encouraging points for housing was affordability: NAR’s Housing Affordability Index rose to 117.6, the highest since March 2022 and the eighth straight monthly improvement. That does not mean housing is easy, but it does mean conditions are a bit less brutal than they were. A little less “survival reality show,” a little more “competitive obstacle course.”

For the West, sales were up 8.2% month over month, while the regional median price was down 1.9% year over year to $603,100. That is useful for Western-market conversations because it shows some softening is happening even without a broad housing collapse narrative.

5) Political Backdrop & Fed Independence

The biggest political and macro story remains the fragile Iran ceasefire and the Strait of Hormuz. Reuters reported that the market is still doubtful about the truce, Trump said U.S. military assets will remain in the region until Iran complies with the deal, and Israel’s ongoing attacks in Lebanon are putting the peace process under strain.

That matters because oil is still acting like it does not trust the headlines either. AP reported WTI rose to $100.79 and Brent to $98.24 Thursday morning, while Reuters noted the 10-year Treasury rose to around 4.31%. Higher oil keeps inflation fears alive, and that spills directly into rate expectations.

There is also a trade-policy angle still hanging around. Reuters reported earlier this week that Trump threatened 50% tariffs on countries supplying Iran with weapons, which adds another layer of inflation and growth uncertainty into an already messy global backdrop.

6) Market Analysis – What This All Means for Rates Going Forward

Base case:

Mortgage rates stay choppy to slightly elevated in the near term. Sticky PCE, stable labor-market claims, a softer GDP revision, and oil near $100 do not give bonds a clean reason to rally.

Better case for rates:

Tomorrow’s March CPI comes in cooler than feared, the ceasefire stabilizes, and oil backs off. If that happens, the market can start re-pricing toward a little relief in Treasury yields and mortgage pricing. Reuters noted economists expect March CPI to rise about 1.0% month over month and 3.3% year over year, so the hurdle is not tiny.

Worse case for rates:

Oil stays high, the ceasefire frays further, and CPI confirms that price pressure broadened in March. In that world, the Fed stays patient even longer, and the “cuts are coming” crowd gets another lesson in character development.

7) Practical Takeaways

For buyers: this remains a market where structure matters more than hope. Product choice, buydowns, concessions, and timing still matter more than trying to out-guess every headline.

For agents: housing activity is still moving, affordability has improved, and inventory is rising, but elevated rates are still the main monthly-payment villain. The market is not dead; it is just picky and more rate-sensitive than ever.

For refi and move-up conversations: today’s data do not support a “rates are about to drop fast” message. The smarter message is that opportunities still exist, but financing strategy needs to be intentional.

8) Lock vs Float

- 0–15 days from closing:

I would still lean lock. Too many inflation and geopolitical variables are in play, and none of them look especially sleepy right now. - 15–30 days:

This is a case-by-case zone. If the borrower is payment-sensitive or tight on DTI, I would still favor protection. If they have room, tomorrow’s CPI is the next major swing factor. - 30+ days:

A cautious float can make sense, but only with discipline. This market can change direction on one inflation report or one Hormuz headline, which is not exactly the environment for casual optimism

Stay safe and make today great!