Good Tuesday morning from your Hometown Lender. Let’s dive into today’s market analysis!

Range trading is the norm. That is the typical market posture, and it is where we currently are, all be it for different reasons this time. Oil is our lever and it will be that way for the foreseeable future (at least until the war is over and oil is flowing through the strait of Hormuz). Oil prices have moved up above $100/barrel. Markets pivoted a few weeks ago from a posture of reacting to every headline to one of muted interest until something ‘real” seems to be happening.

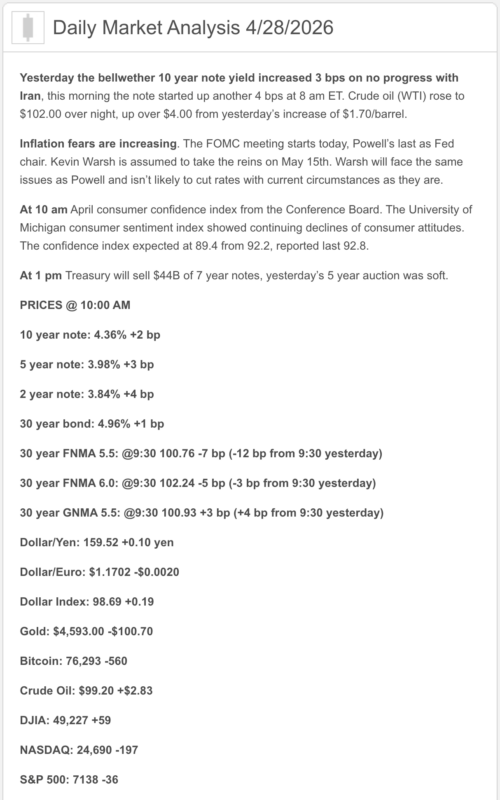

The Fed meeting starts today and concludes tomorrow with the Fed policy statement and Fed Chair Powell’s press conference. This should be Chairman Powell’s last meeting as Chair and potentially as fed Governor. Typically, Fed Chairman’s step down from the Fed when they leave the Chairmanship. That is an interesting nuance as stepping down would allow President Trump to appoint another Fed Governor (another dove). This Fed meeting will likely not help rates so today is likely a good day to lock some loans if risk averse or closing soon, unless committed to floating into the Fed meeting tomorrow.

Market Analysis – From a higher and better view:

Market Analysis – Quick Snapshot

- This morning actually did bring fresh data: the Conference Board’s Consumer Confidence Index rose to 92.8 in April from an upwardly revised 92.2 in March, with the Expectations Index at 72.2 and the Present Situation Index at 123.8. That is better than expected, but it is still not exactly “consumers are back to doing cartwheels in Costco.”

- Housing gave us a quieter but important update: FHFA said single-family home prices were unchanged in February from January and up 1.7% year over year. Translation: home prices are no longer sprinting, but affordability is still not sending apology flowers.

- Oil is back in the starring role. Reuters reported Brent at about $111.40 and WTI at about $100, while S&P 500 futures were down 0.7% and Nasdaq futures were down 1.3% as stalled U.S.-Iran talks kept inflation fears alive.

- The Fed begins its two-day meeting today, April 28, with the decision due tomorrow, April 29. The current target range is still 3.50% to 3.75%, and the schedule shows Powell’s press conference tomorrow afternoon.

- Mortgage rates remain improved from the early-April spike. Freddie Mac’s latest weekly survey shows the 30-year fixed at 6.23% and the 15-year fixed at 5.58%.

- This week’s next major macro checkpoints are Thursday, April 30: Q1 GDP advance, March Personal Income and Outlays, and Q1 Employment Cost Index are all scheduled for 8:30 a.m. ET.

1) Market Analysis – What Hit This Morning

Today’s actual economic story was consumer confidence plus home prices. Consumer confidence unexpectedly improved, which says households are not completely folding under higher gas prices and war headlines. But Reuters also noted that comments inside the survey were still largely pessimistic about prices, oil, gas, and the broader impact of the Middle East conflict. So the headline was better; the mood underneath it still needs a pep talk and maybe a nap.

The second piece was FHFA home prices. Nationally, prices were flat month over month in February and up 1.7% year over year, with some softness in the Mountain and Pacific regions. That matters because it suggests home values are no longer running away at the national level, but high mortgage rates are still doing plenty of damage to affordability.

Narrative you can use:

“Today’s data said the consumer is hanging in better than expected, but housing affordability is still tight and oil is still the bigger problem for rates. The bond market is paying a lot more attention to $111 Brent than to a modest improvement in confidence.”

2) Market Analysis – Fed Watch

Officially, the Fed is still in a 3.50% to 3.75% target range, and its two-day meeting starts today, April 28, with the decision due tomorrow, April 29. Markets broadly expect no change this week.

The more interesting part is the leadership backdrop. Reuters reports that Kevin Warsh’s nomination is set for a Senate Banking Committee vote on Wednesday at 10 a.m. EDT, the same day the Fed meeting wraps up, and that he could plausibly be in place for the June meeting. Reuters also says Warsh is preparing for what he called a “good family fight” inside a Fed that is still divided between hawks focused on inflation and doves more worried about labor softness.

So the Fed story this week is not just “hold or cut.” It is also “what does the next Fed look like, how hawkish is it, and how independent does the market believe it will be?” That is a big reason tomorrow’s Powell press conference matters beyond the actual rate decision.

3) Market Analysis – Where Mortgage Rates Actually Are

Freddie Mac’s latest weekly survey still shows the 30-year fixed at 6.23% and the 15-year fixed at 5.58%, both lower than the prior week. Freddie Mac also noted the 30-year is at its lowest level of the last three spring homebuying seasons, which is the kind of sentence the purchase market would like framed and hung in the lobby.

But today is a good reminder that mortgage pricing is still being pushed around more by oil, inflation expectations, and Treasury-market mood than by happy speculation about future Fed cuts. Reuters said crude surged as peace talks stalled and global markets turned more cautious, which is exactly the kind of setup that can make mortgage improvement feel temporary if it lasts only until the next headline.

4) Market Analysis – Housing Market Check

Today’s fresh housing data were about prices, not sales. FHFA’s February read showed home prices were flat month over month and up 1.7% year over year, while Reuters said the shortage of starter homes is still supporting values even as higher rates squeeze affordability. That is a pretty good summary of the market: prices are no longer flying, but they are not exactly falling out of bed either.

The broader housing backdrop is still mixed. Freddie Mac is showing better mortgage-rate momentum, but Reuters noted that rates had bounced from 5.98% in late February to 6.46% in early April before easing again, and that volatility has made affordability a bigger political and consumer issue. So housing is still moving, just not gracefully. More cautious shuffle than victory lap.

5) Political Backdrop & Fed Independence

The biggest macro-political story remains the Iran war and the Strait of Hormuz. Reuters says oil jumped as Washington rejected Iran’s latest proposal and as supply through Hormuz remained badly impaired. Reuters also reports roughly 10 million barrels per day of supply are still disrupted, which is why energy is back to doing body slams on inflation expectations.

The other story is Fed independence and succession. Reuters says Warsh’s nomination is expected to advance this week, and that his hearing comments made clear he would face a real internal fight if he tries to push a more aggressive cut agenda than current hawks want. That matters because markets are now pricing not just the Fed we have, but the Fed we might have in a few weeks.

6) Market Analysis – What This All Means for Rates Going Forward

Base case:

Mortgage rates stay choppy and vulnerable near term. Consumer confidence improved, yes, and home prices were flat month to month, but oil back above $111 Brent is the piece the bond market is most likely to obsess over.

Better case for rates:

The better path is that diplomacy restarts in a serious way, oil backs off, and Thursday’s GDP / income / wage-cost data do not show a broad inflation re-acceleration. That is an inference, but it is grounded in the fact that this week’s market tone is being driven heavily by oil and Fed expectations rather than by runaway domestic strength.

Worse case for rates:

If peace talks stay stuck, oil remains elevated, and the Fed sounds more worried about inflation than the market wants to hear tomorrow, mortgage rates can easily give back some of the recent improvement. Reuters’ reporting on Warsh, Powell, and the current hawk-dove split makes that risk very real.

7) Market Analysis – Practical Takeaways

For buyers, this is still a market where structure beats hope. The Freddie Mac rate is better, but not low enough to make payment sensitivity disappear. Buydowns, concessions, and smart product choice still matter a lot.

For agents, today’s message is balanced: consumers are not collapsing, home prices are no longer climbing fast, and rates are a little better — but oil and inflation are still capable of messing up the mood quickly. The market is alive. It is just not exactly wearing roller skates and a cape.

For refi and move-up conversations, the honest message is still not “rates are about to tumble.” The smarter message is that windows may open, but they are still being driven more by oil and bond sentiment than by any clear Fed pivot.

8) Lock vs Float

0–15 days from closing:

I would still lean lock. This is Fed week, oil is hot again, and the market is too headline-sensitive to get cute with a near-term close.

15–30 days:

This is still case by case. If the borrower is tight on DTI or very payment-sensitive, I would favor protection. If they have room, tomorrow’s Fed and Thursday’s GDP / ECI / income data are real volatility checkpoints worth watching. 30+ days:

A cautious float can make sense, but only with discipline. Right now the market is trading oil, Fed succession, and incoming inflation-growth signals all at once.

Stay safe and make today great!