Good Friday Morning from your Hometown Lender! Let’s get Friday’s market analysis started!

Rates today are starting off better than we ended yesterday. There is a small decoupling of the 10yr note and 30yr mortgage rates for the moment. Mortgage rates are the winner for now but know they always regress to the mean.

Reprice risk on the day is moderate, markets are overreacting to any Middle East headline, but two things remain true that are keeping rates locked up tight.

The first is that if the ceasefire holds, and there is no military escalation, we won’t see rates move that much higher. Sure, we’re going to see this slow, painful bleeding in pricing, but rates really aren’t moving. We don’t have to worry about rates pushing up to the highs we saw in March if there is talk of ending this conflict.

The second thing is that until the Strait of Hormuz is truly open once again to traffic, we can’t see rates move that much lower. It’s become a game of one-upmanship with both Iran, and the US blocking ships from sailing. Each side is trying to outlast the other, to gain the upper hand in negotiations. We saw last Friday how markets will react when the strait is open, as bonds rallied along with stocks on the news that it would be open. Unfortunately, though, that lasted all of about 24 hours.

Market Analysis – From a higher and better view:

Market Analysis – Quick Snapshot

- Today’s headline is a split-screen market. Stocks are leaning risk-on, but oil is still acting like the office fire alarm. At 9:45 a.m. ET, the Dow was down 0.35%, the S&P 500 was up 0.21%, and the Nasdaq was up 0.63% as renewed hopes for U.S.-Iran talks lifted tech and broader sentiment.

- Oil remains the biggest macro headache. Reuters reported Brent was down 0.6% to $104.49 and WTI down 2.1% to $93.54 by midday Friday, but Brent was still about 16% higher for the week and Reuters said Brent remained roughly 44% above pre-war levels because Hormuz shipping is still badly disrupted.

- Consumers are waving a caution flag. The University of Michigan’s final April sentiment reading fell to a record low 49.8, down from 53.3 in March. One-year inflation expectations were 4.7%, and five-year expectations rose to 3.5% from 3.2%.

- The Fed is still on hold at 3.50% to 3.75%. In its March statement, the Fed said inflation remains somewhat elevated and that uncertainty about the outlook and Middle East developments remains elevated. Markets currently see about a 99.5% chance of another hold next week.

- Mortgage rates improved again this week. Freddie Mac’s latest survey shows the 30-year fixed at 6.23% and the 15-year fixed at 5.58%, both down from last week and the lowest 30-year reading of the last three spring homebuying seasons.

- Housing is still moving, but with a limp. March retail sales rose 1.7%, and core retail sales rose 0.7%, which helps Q1 growth. On housing, pending home sales rose 1.5% in March, but they were still down 1.1% year over year, and higher mortgage rates plus tight inventory remain constraints.

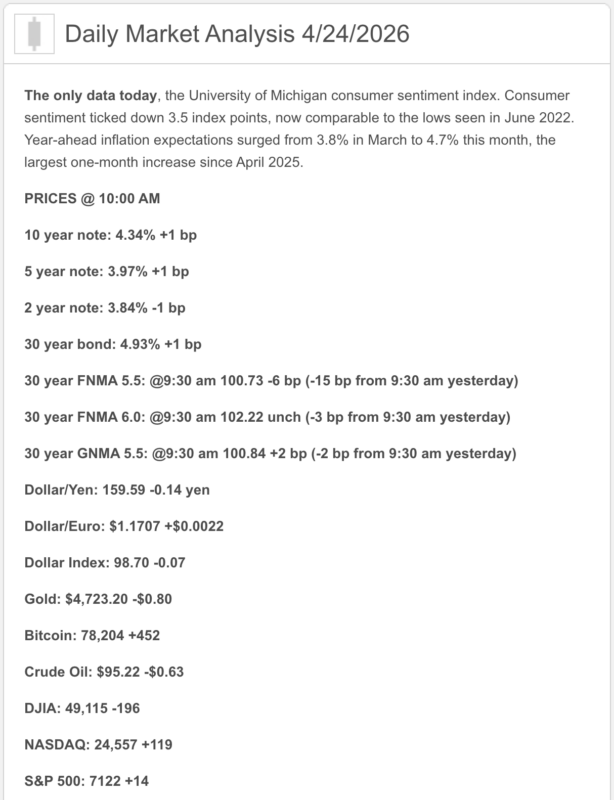

1) Market Analysis – What Hit This Morning

This morning’s fresh economic headline was consumer sentiment, and it was ugly. The University of Michigan’s final April reading fell to a record low 49.8, even though it improved a bit from the preliminary 47.6. Inflation expectations also stayed elevated, with the one-year view at 4.7% and the five-year view at 3.5%. In plain English: consumers are not feeling great, and they are not convinced prices are done misbehaving.

The market, though, is not trading sentiment alone. Stocks are getting support from fresh hopes for U.S.-Iran talks and from a huge Intel-led chip rally, which is helping the Nasdaq shrug off some of the war gloom. So today’s tape is basically: consumers feel lousy, traders see opportunity, and oil is still the adult supervision problem.

Narrative you can use:

“Today’s market is balancing two competing stories: consumer confidence is weak and inflation fears are still high, but investors are willing to buy stocks on the belief that peace talks could ease some of the energy shock. Mortgage rates are improving, but the oil story still matters a lot more than anybody would like.”

2) Fed Watch

Officially, nothing has changed. The Fed kept the target range at 3.50% to 3.75% in March and said inflation remains somewhat elevated while uncertainty around the outlook and Middle East developments remains elevated.

Unofficially, the Fed story got more political today. The Justice Department said it is closing its investigation into Jerome Powell, removing a major obstacle to Kevin Warsh’s confirmation path. Reuters reported that Powell’s chair term still ends on May 15, and ending the probe could clear the way for Warsh’s confirmation by then.

Warsh is also still talking about changing how the Fed thinks about inflation and shrinking the balance sheet over time. That does not change next week’s meeting, but it matters because markets are now trying to price not just the current Fed, but the possible next one. The near-term takeaway remains simple: next week still looks like a hold, and the rate-cut story has been pushed back hard by war-related inflation risk.

3) Market Analysis – Where Mortgage Rates Actually Are

This week’s Freddie Mac survey is a real improvement. The 30-year fixed averaged 6.23% and the 15-year fixed averaged 5.58%, both down from 6.30% and 5.65% last week. Freddie Mac also said the 30-year is now at its lowest level of the last three spring homebuying seasons.

That is the good news. The less-fun news is that mortgage pricing is still being pushed around more by oil, inflation expectations, and Treasury sentiment than by cheerful talk about future Fed cuts. Reuters noted mortgage rates track Treasuries, and they spiked from 5.98% just before the war to 6.46% in early April before settling back down. So yes, we’ve improved — but this market still bruises easily.

4) Market Analysis – Housing Market Check

The March housing read was a little better on contracts than on closings. Pending home sales rose 1.5% to 73.7, beating expectations, but they were still down 1.1% from a year ago, and Reuters noted higher mortgage rates and tight inventory remain real constraints. The strongest contract activity came in the Northeast and South, while the West and Midwest weakened.

The broader housing message is still the same: the market is alive, but payment-sensitive. March retail sales rose 1.7%, with core retail sales up 0.7%, which suggests consumers still spent in Q1, but Reuters also warned that a lot of the strength was tied to higher gasoline receipts and that weakness may still be coming as fuel costs bite. That matters for housing because if gas keeps eating the household budget, affordability gets hit from another angle.

Freddie Mac’s own commentary was mildly encouraging, pointing to lower mortgage rates, improving purchase applications, refinance activity, and better pending sales as signs of improving momentum. That is good. It is just not the same thing as “housing is off to the races.” More like the market found its shoes and is considering a brisk walk.

5) Market Analysis – Political Backdrop & Fed Independence

The macro-political story is still overwhelmingly about Iran, Hormuz, and whether peace talks actually go anywhere. Reuters reported that Iranian Foreign Minister Abbas Araqchi is expected in Islamabad and that talks with the U.S. are likely to resume, which is helping stocks today. At the same time, Reuters also reported only five ships passed through the Strait of Hormuz in 24 hours, versus a pre-war average of about 140 daily passages, which tells you the supply-chain problem is very much not solved.

That is why oil is still such a problem for rates. Reuters says the strait normally handles about one-fifth of global oil flows, and Goldman estimates about 14.5 million barrels per day of Gulf crude output — about 57% of pre-war supply — was offline in April. Even if talks restart, the recovery in output and shipping is not expected to be instant.

The Fed-independence angle also got louder today with the Powell investigation ending and Warsh’s path looking clearer. That does not immediately change mortgage pricing, but it absolutely matters for how markets think about the next chapter of policy. When the identity and philosophy of the next Fed chair are in play, bonds tend to listen.

6) Market Analysis – What This All Means for Rates Going Forward

Base case:

Mortgage rates stay choppy but a bit improved, as long as peace-talk optimism keeps oil from making another sharp move higher. The better Freddie Mac reading is real, but the broader environment still includes high oil, fragile shipping, and a Fed that is not in a hurry to cut.

Better case for rates:

The better path is that talks resume in a meaningful way, shipping through Hormuz gradually improves, and the next inflation prints do not confirm a broader re-acceleration. That is an inference, but it is grounded in today’s stock rally on peace hopes, falling intraday oil prices, and the recent improvement in mortgage rates.

Worse case for rates:

If talks fizzle, shipping stays frozen, and energy pressure keeps feeding inflation expectations, the market can keep pushing cuts further out and mortgage rates can easily give back some of this week’s improvement. Reuters’ economist poll already showed a big shift toward the Fed staying steady through September, and consumer inflation expectations are still elevated.

7) Market Analysis – Practical Takeaways

For buyers, this is still a market where structure beats hope. The 30-year at 6.23% is better than where we were a few weeks ago, but it is not low enough to make payment sensitivity disappear. Buydowns, concessions, and smart product choice still matter a lot.

For agents, the message is balanced: contracts improved in March, and Freddie Mac is seeing some signs of better momentum, but housing is still rate-sensitive and consumers are clearly more nervous. That means realistic pricing and strong financing strategy still do more work than motivational speeches and a ring light.

For refi and move-up conversations, the honest message is still not “rates are about to tumble.” The smarter message is that windows can open, but they are being driven more by oil and bond sentiment than by any clear Fed pivot.

8) Lock vs Float

0–15 days from closing:

I would still lean lock. This week’s improvement is helpful, but there is still too much geopolitical headline risk to get cute with a near-term closing.

15–30 days:

This is still case by case. If the borrower is tight on DTI or highly payment-sensitive, I would still favor protection. If they have room, there is at least a reasoned case for cautious patience because mortgage rates have improved and talks may resume.

30+ days:

A cautious float can make sense, but only with discipline. Right now the market is trading peace hopes, oil risk, Fed succession, and inflation expectations all at once.

Stay safe and make today great!