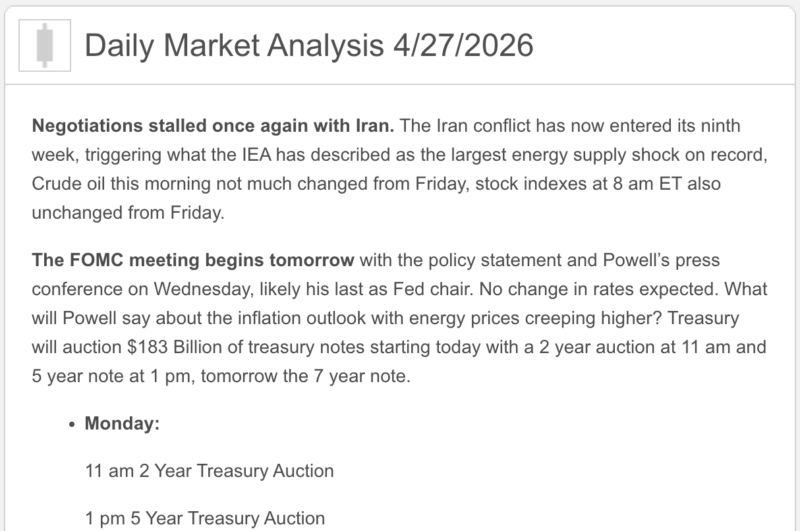

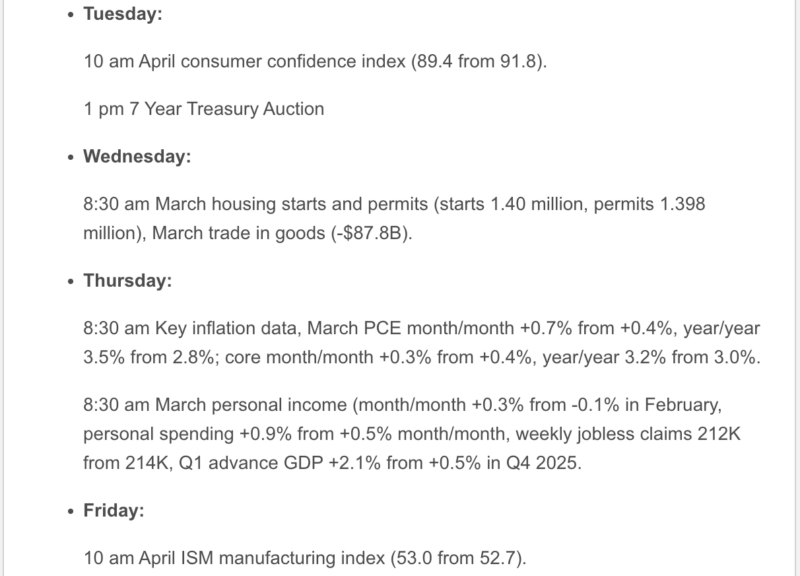

Good Monday morning from your Hometown Lender. Let’s get to Monday’s market analysis!

Friday was a good day for bonds after some early volatility, helping rate sheets to improve a bit to end the week. What started out as a bad day saw a reversal when news broke that the DOJ was dropping the probe into Fed Chair Jerome Powell, opening the door for the confirmation of Kevin Warsh as his successor. Bonds liked the news since this increases the odds of a Fed rate cut this year, rallying into the late morning and holding the gains through the day.

Rate sheets today likely to be about the same as Friday, basically treading water. Reprice risk on the day is low, markets are calm despite a lack of progress in negotiations with Iran. This week brings something new to focus on with the Fed meeting on Wednesday, but I’m not expecting rates to move much anyway. Remember, rates are not likely to fall much until the Strait of Hormuz is open to commercial traffic.

Market Analysis – From a higher and better view:

Market Analysis – Quick Snapshot

- No major 8:30 a.m. macro bomb today. The market opened the week focused more on stalled U.S.-Iran talks, higher oil, big tech earnings, and this week’s Fed meeting than on fresh domestic data. Wall Street was only modestly lower early, with the Dow down 0.05%, the S&P 500 down 0.07%, and the Nasdaq down 0.27%.

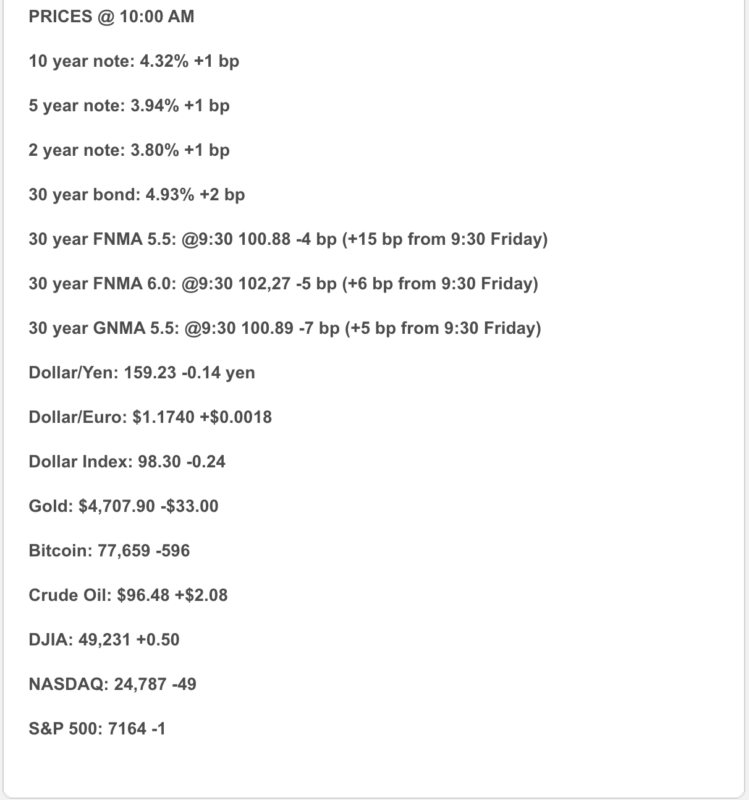

- Oil is back in charge of the room. Reuters reported Brent at $107.49 and WTI at $95.72 around mid-morning, with shipments through Hormuz still badly impaired and peace talks stalled. Reuters also cited estimates that 10–13 million barrels per day are still not reaching the global market.

- The Fed is still at 3.50% to 3.75%, and Wednesday is widely expected to be another hold. Reuters says this meeting may be Jerome Powell’s last as chair, with Kevin Warsh’s path clearer after the DOJ dropped its Powell probe and Senator Thom Tillis said he’s ready to advance Warsh’s confirmation.

- Mortgage rates improved again last week. Freddie Mac’s latest survey shows the 30-year fixed at 6.23% and the 15-year fixed at 5.58%, both down from the prior week. Freddie Mac says the 30-year is now at its lowest level of the last three spring homebuying seasons.

- Consumers still look uneasy. The University of Michigan’s final April sentiment reading fell to a record low 49.8, while 1-year inflation expectations rose to 4.7% and 5-year expectations rose to 3.5%.

- Housing is still moving, but it is not exactly gliding. Pending home sales rose 1.5% in March, but were still down 1.1% year over year. Meanwhile, existing-home sales fell 3.6% to 3.98 million, inventory rose to 1.36 million, and supply increased to 4.1 months.

- Consumer spending held up in March, but a lot of that strength came from higher gas prices. Retail sales rose 1.7%, while core retail sales rose 0.7%.

1) Market Analysis – What Hit This Morning

Today’s market story is mostly about what didn’t hit this morning: there was no top-tier domestic release strong enough to overpower oil, geopolitics, earnings, and the Fed. Reuters said Wall Street opened cautiously as stalled U.S.-Iran talks kept investors on edge heading into a huge week for earnings and central-bank decisions.

That leaves crude as the main macro narrator again. Brent is back above $107, WTI is back near $96, and Reuters says the diplomatic standoff plus limited Hormuz traffic are keeping global energy supplies tight. Translation: the market came into Monday hoping for a normal earnings week and got another reminder that oil still has main-character energy.

Narrative you can use:

“Today’s bond-market setup is pretty simple: there wasn’t a big U.S. data release to move markets, so oil and geopolitics took over again. As long as Hormuz stays constrained and peace talks stay stuck, inflation fears are going to keep mortgage-rate relief on a short leash.”

2) Fed Watch

Officially, nothing changed. The Fed’s target range remains 3.50% to 3.75%, and the March statement said the Committee would carefully assess incoming data, the evolving outlook, and the balance of risks.

Unofficially, this week’s meeting has a lot more drama than a routine hold normally deserves. Reuters says Powell will likely oversee another hold on Wednesday, but this may be his last meeting as Fed chair, because the end of the DOJ probe removed a key obstacle to Warsh’s confirmation and Powell had previously tied his departure from the Board to resolution of that issue. Reuters also says Powell could face questions about whether he will remain on the Board even after his chair term ends.

The policy backdrop itself is still messy. Reuters says the Fed is weighing elevated inflation risks tied to the Iran war against signs of a softer labor market, and that policymakers could even begin signaling the possibility of hikes later this year if inflation accelerates further. That is not base case yet, but it is absolutely not the language of a central bank itching to rescue borrowers.

3) Market Analysis – Where Mortgage Rates Actually Are

Freddie Mac’s latest weekly survey shows the 30-year fixed at 6.23% and the 15-year fixed at 5.58%, both down 7 basis points from the prior week. Freddie Mac explicitly said the 30-year rate is now at its lowest level of the last three spring homebuying seasons.

That is real improvement, and worth noting. But mortgage pricing is still being pushed around more by oil, inflation expectations, and Treasury-market mood than by happy talk about future Fed cuts. Reuters noted existing-home sales signed earlier in the year were helped when mortgage rates were around 5.98% in late February, only to see rates jump to 6.46% in early April as the war-driven oil shock hit bonds.

So yes, we are better than the early-April ugliness. No, this is not a “welcome back to easy money” moment. This market still bruises easily.

4) Market Analysis – Housing Market Check

The housing picture is mixed, which is another way of saying it still needs caffeine and therapy. Pending home sales rose 1.5% in March to 73.7, beating expectations, which says buyers were still writing contracts despite higher rates. But those pending sales were still down 1.1% from a year earlier, and Reuters noted higher mortgage rates and tight inventory remain real constraints.

The closed-sales side still looks softer. Reuters reported existing-home sales fell 3.6% in March to a 3.98 million annual pace, a nine-month low. Inventory rose to 1.36 million, supply increased to 4.1 months, and the median price climbed to $408,800. Reuters also reported NAR cut its 2026 home-sales growth forecast to 4% from 14%.

The consumer side of the economy matters here too. March retail sales rose 1.7%, but Reuters said the bulk of the increase came from a record 15.5% jump in gasoline-station receipts. So the spending headline looked strong, but the composition says households were also getting whacked by fuel costs. That is not exactly a housing tailwind.

5) Market Analysis – Political Backdrop & Fed Independence

The biggest macro-political story is still the stalemate around Iran and the Strait of Hormuz. Reuters says Trump canceled the planned envoy visit to Pakistan, Iran’s foreign minister traveled to Russia, and mediator Pakistan says work to bridge the gaps has not stopped. That is diplomat-speak for “still messy.”

Meanwhile, the physical bottleneck remains severe. Reuters reported that only about seven ships crossed Hormuz in the last 24 hours, versus a pre-war average near 140 daily passages, and that roughly 20% of global oil supply used to move through the strait before the war began on February 28. That is why oil is still doing pushups on the market’s chest.

The Fed-independence angle is also very much alive. Reuters says the DOJ dropping the Powell probe, Tillis stepping aside, and Warsh moving closer to confirmation have turned this week’s Fed meeting into more than just a rate decision. It is now also part of a live succession story, which means Powell’s press conference could matter as much for governance and credibility as for the rate path itself.

6) Market Analysis – What This All Means for Rates Going Forward

Base case:

Mortgage rates stay choppy and a little vulnerable near term. Oil is high, peace talks are stuck, and the Fed is expected to hold while keeping a wary eye on inflation risk. That is not a clean setup for a big bond rally.

Better case for rates:

The better path is that mediator efforts start producing something real, ships begin moving through Hormuz in more normal volume, oil backs off, and the market decides the inflation shock is easing rather than spreading. That is an inference, but it is grounded in the fact that oil and yields have been reacting sharply to each twist in the diplomacy story.

Worse case for rates:

If talks keep stalling, shipping stays constrained, and oil remains in the mid-to-upper $100s on Brent, the Fed will have even less room to talk about cuts and more reason to lean hawkish. Reuters already says policymakers may have to consider signaling the possibility of hikes later this year if inflation accelerates.

The next big domestic checkpoints are Wednesday’s Fed decision, Thursday’s Q1 GDP and Q1 Employment Cost Index, and Thursday’s next PCE release.

7) Practical Takeaways

For buyers, this is still a market where structure beats hope. Freddie Mac’s 6.23% is encouraging, but not low enough to erase payment sensitivity. Buydowns, concessions, and smart product choice still matter a lot.

For agents, the message is balanced: contract activity improved in March, but closed sales are still soft, inventory is still tight, and consumers are clearly more nervous. The market is moving, just with a noticeable limp.

For refi and move-up conversations, the honest message is still not “rates are about to tumble.” The smarter message is that windows may open, but they are being driven more by oil and bond sentiment than by any clear Fed pivot.

8) Lock vs Float

0–15 days from closing:

I would still lean lock. This market is too headline-sensitive, and today’s oil move is exactly the kind of thing that can undo progress quickly.

15–30 days:

This is still case by case. If the borrower is tight on DTI or highly payment-sensitive, I would favor protection. If they have room, there is at least a reasonable case for cautious patience into Wednesday and Thursday’s data.

30+ days:

A cautious float can make sense, but only with discipline. Right now the market is trading oil, peace-talk credibility, the Fed meeting, and Powell/Warsh succession all at once.

Stay safe and make today great!