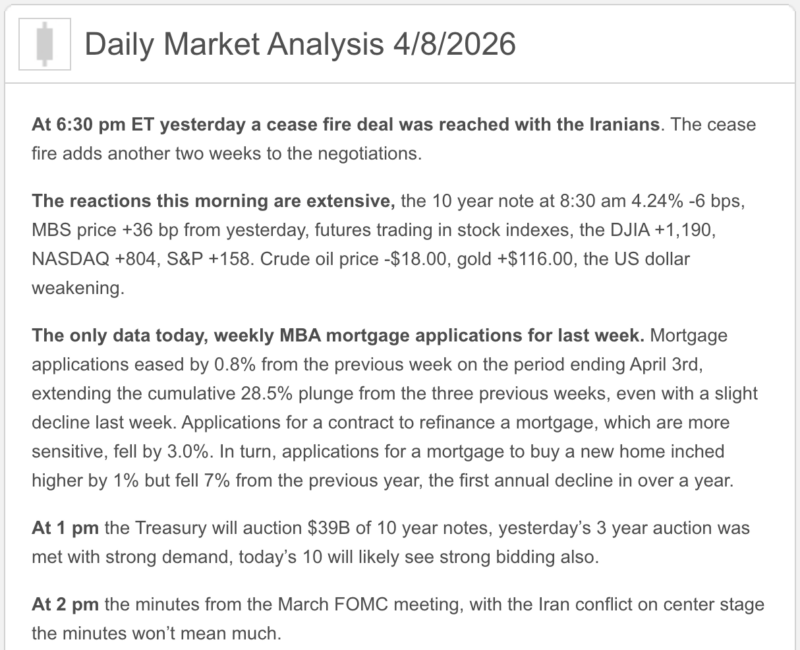

Good morning on this best day of the week Wednesday from your Hometown Lender. Here’s your Wednesday market analysis.

Yesterday saw mortgage bonds improve through the afternoon, reversing from being down on the day when pricing came out to up quite a bit on the day. I would attribute the move to a mini “flight to safety” as traders tried to prepare for whatever was coming as President Trump’s deadline with Iran was coming at 8m ET last night.

Rate sheets today should be quite a bit better, reflecting a relief rally in bonds after a ceasefire was announced last night with Iran. However, this is not a full resolution, as core issues still remain unresolved. Markets speculation that we could see a Fed rate cut by the end of the year jumped after the news, and stocks rallied while oil prices fell the biggest amount in 6 years.

Market Analysis – From a higher and better view:

Oil finally cooled, stocks are smiling again, but the bond market still has trust issues

🚀 Market Analysis – Quick Snapshot

- Fed: The Fed is still at 3.50% to 3.75% after the March 17–18 meeting. In that meeting’s statement, officials said growth was still solid, job gains had remained low, unemployment had been little changed, and inflation remained somewhat elevated. The minutes from that meeting are due today at 2:00 p.m. Eastern.

- Inflation: The latest official CPI reading, for February, was 2.4% headline and 2.5% core year over year. The Fed’s own March projections lifted year-end 2026 PCE and core PCE forecasts to 2.7%, and the New York Fed’s March survey showed one-year inflation expectations rose to 3.4% from 3.0%.

- Mortgage rates: The MBA said the average 30-year fixed fell slightly to 6.51% for the week ended April 3, while refinance applications fell 2.8% and purchase applications rose about 1% week over week but remained 7% below last year. Freddie Mac’s latest weekly survey showed 6.46% for the 30-year fixed and 5.77% for the 15-year fixed as of April 2.

- Housing: Existing-home sales rose 1.7% in February to a 4.09 million annual pace, inventory reached 1.29 million homes or 3.8 months’ supply, and pending-home sales rose 1.8% to 72.1. Reuters’ March housing poll also showed home prices are expected to rise just 1.8% this year.

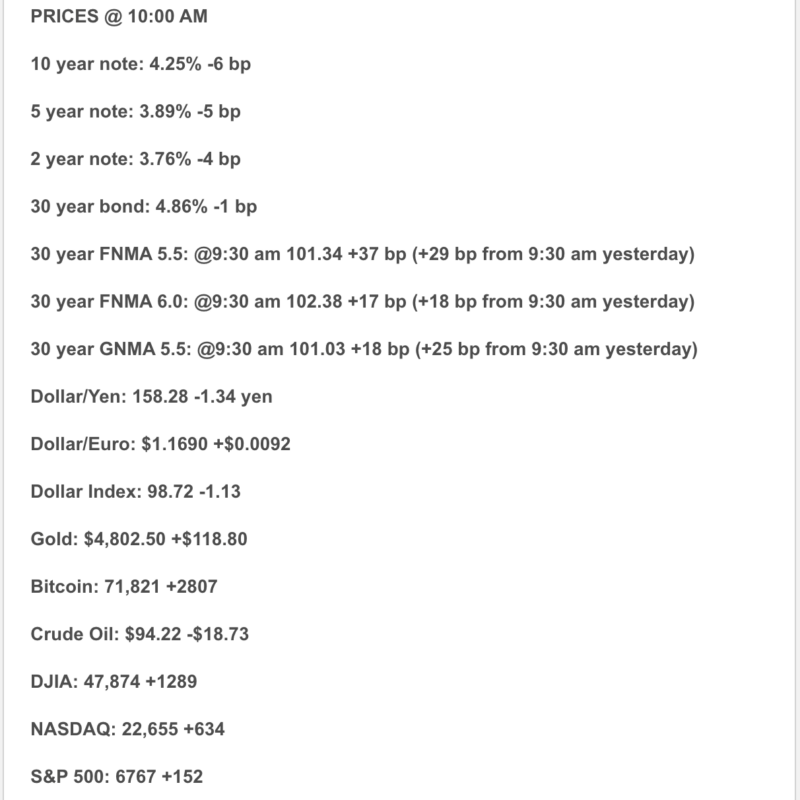

- Markets today: Wall Street jumped after a two-week U.S.-Iran ceasefire announcement, with the Dow up 2.33%, the S&P 500 up 2.13%, and the Nasdaq up 2.56% at 11:30 a.m. ET, while crude slipped below $100. But bond investors are still acting like inflation may stay hotter for longer.

The big takeaway:

Today’s market mood is better, but not fully healed. Stocks are celebrating the ceasefire and lower oil, mortgage rates finally caught a tiny break, and buyers at least got a little oxygen. But bonds are still saying, “That’s cute — call me when inflation actually behaves.”

🎯 Market Analysis – What Happened Today?

The headline move today is geopolitical, not domestic economic data. The U.S. and Iran agreed to a two-week ceasefire, which sent crude below $100 and sparked a broad relief rally in stocks around the world. By late morning, the Dow, S&P 500, and Nasdaq were all up sharply, and travel and industrial names were among the winners while oil stocks lagged.

At the same time, the rate market is not giving a full all-clear. Reuters reported that even with the truce, bond investors do not expect a full return to pre-war rate-cut optimism because energy prices and inflation are still expected to run hotter for longer, and many of the “cut” bets that existed before the conflict are gone. Benchmark 10-year Treasury yields were around 4.23%, basically back to mid-March levels rather than back to anything truly comfortable.

Translation:

The market got a relief rally, not a clean bill of health. Better mood, yes. Full forgiveness, not yet.

🏦 Fed Watch

The Fed’s official posture is still wait-and-see. At the March meeting, officials kept rates unchanged at 3.50% to 3.75% and gave little sign that a near-term move was likely. Reuters’ preview of today’s minutes says policymakers already knew the war-driven oil shock would lift inflation this year, and the minutes may show just how intensely they debated the tradeoff between higher inflation and weaker growth or employment.

Fed Vice Chair Philip Jefferson reinforced that caution yesterday, saying he sees downside risk to the labor market and upside risk to inflation, and that current policy is still appropriately positioned while the Fed watches how the economy evolves. That is central-bank language for: nobody is eager to get cute here.

Plain English:

The Fed is not ready to play hero for mortgage rates. It wants more proof that inflation is calming down before it starts thinking about easier policy again.

📈 Market Analysis – Where Mortgage Rates Actually Are

Here’s where all of that turns into real payment math:

- MBA weekly application market: 6.51% average contract rate for a 30-year fixed, down 6 basis points from the prior week.

- Freddie Mac weekly average: 6.46% for a 30-year fixed and 5.77% for a 15-year fixed as of April 2.

- Mortgage demand: Refi applications fell 2.8%, and purchase applications rose about 1% week over week but were still 7% lower than a year earlier.

Real-world takeaway:

Rates finally moved in the right direction this week, but only a little. This was more of a “tiny exhale” than a victory lap. The market basically loosened its tie, not its standards.

🏠 Market Analysis – Housing Market Check

The good news:

- Existing-home sales rose 1.7% in February to a 4.09 million annual rate.

- Inventory rose to 1.29 million homes, equal to 3.8 months’ supply.

- Pending-home sales rose 1.8% in February to 72.1, with gains in the West, South, and Midwest.

The not-as-fun news:

- Purchase applications are still 7% below year-ago levels, which tells you affordability is still doing its thing.

- Reuters’ March poll of housing analysts forecast home prices will rise only 1.8% this year because the market remains constrained by high mortgage rates and a shortage of affordable homes.

- The spring rebound story is still fragile because February’s housing momentum happened before the war-driven backup in yields and rates. Reuters explicitly noted further gains in pending sales were likely to be limited by the conflict’s effect on oil prices and inflation fears.

What that means:

Housing is moving, but carefully. Inventory is improving enough to make buyers feel like they have choices again, but monthly payment still decides whether those choices turn into contracts.

🌍 Market Analysis – Political + Global Market Backdrop

Today’s political story is the market story. The U.S.-Iran ceasefire announcement helped calm fears about the Strait of Hormuz and energy supply, which is why oil fell so hard and stocks rallied. But Reuters also reported there were still renewed attacks elsewhere in the region, and bond markets are treating the ceasefire as temporary relief rather than final resolution.

That matters because inflation psychology has already been bruised. The New York Fed’s March survey found one-year inflation expectations rose to 3.4%, expected gasoline-price growth jumped to 9.4%, and longer-run expectations stayed above the Fed’s 2% target. Even with lower oil today, the market is still dealing with the aftertaste of the shock.

Why that matters:

Mortgage rates do not just react to what oil does today. They react to whether traders think the inflation scare is truly over. Right now, traders are saying, “better, but not forgiven.”

🔮 Market Analysis – What This Means for Rates Going Forward

Base Case

Rates stay choppy but somewhat better than last week if the ceasefire holds and oil stays below the panic zone. Mortgage pricing can improve modestly in that setup, but probably not dramatically because the bond market still thinks inflation will stay sticky. This is an inference from today’s market rally, lower oil, and Reuters’ reporting that pre-war rate-cut bets are unlikely to fully return.

Best Case

The best case is that the ceasefire proves durable, oil keeps cooling, the Fed minutes come off as cautious but not more hawkish, and Friday’s CPI behaves. That would give bonds a better chance to rally and mortgage rates a chance to improve further. This is an inference supported by today’s relief move and the upcoming CPI calendar.

Worst Case

The uglier path is that the ceasefire cracks, oil rebounds, and Friday’s CPI confirms that the recent energy shock is bleeding into broader inflation. In that case, this week’s improvement in mood could disappear fast. This is an inference supported by Reuters’ reporting on fragile ceasefire conditions and persistent inflation worries.

Bottom line:

Today was a relief rally, not a reset. Mortgage rates may have stopped getting worse for the moment, but they have not suddenly become friendly neighborhood rates.

🧠 Practical Takeaways

For buyers:

This is still a strategy market, not a perfection market. The slight dip in mortgage rates is helpful, but homes are still expensive and affordability is still tight.

For agents:

There is finally a little breathing room in the rate conversation this week, but the message is still structure over swagger. Payment, concessions, and realistic expectations matter more than a one-day rally in stocks. This is an inference drawn from the modest mortgage-rate drop and the still-soft purchase-application backdrop.

For homeowners thinking about refinancing:

This week’s dip is a reminder that windows can reopen quickly when macro fear cools. It is not a wide-open window, but it is at least no longer a brick wall. This is an inference based on the MBA rate pullback and today’s ceasefire-driven market relief.

🔒 Lock vs Float

Lock if:

- closing is within 30 days

- the borrower is payment-sensitive

- the file is tight on qualifying

- the deal cannot absorb renewed volatility

That still makes sense because, even with today’s better tone, Reuters reports the bond market does not expect a full return to pre-war rate-cut expectations.

Float cautiously if:

- the borrower has more time

- the file is strong

- everyone understands the risk

- the borrower can handle short-term swings

That argument got slightly better today because rates dipped and oil fell, but it is still a measured-risk call, not a “the coast is clear” call.

Simple rule:

If a worse rate creates a real problem, lock. If the borrower has flexibility and time, a cautious float can still make sense while we watch the ceasefire, the Fed minutes, and Friday’s CPI.

Stay safe and make today great!