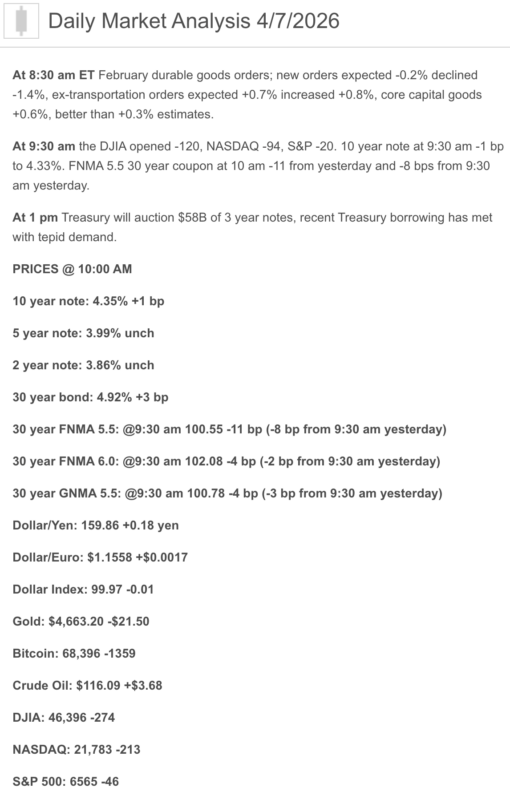

Good Tuesday morning from your Hometown Lender. Here is your market analysis.

Yesterday saw mortgage bonds pickup gains early, wiping out the losses from Friday’s stronger than expected jobs data. Bonds held the gains through the day on lower-than-normal trading volume. Overall, it was a good day for bonds and rate sheets.

Rates today are worse in advance of tonight’s deadline with Iran. While the President has moved deadlines previously, it would be surprising if he did so again without a commitment from Iran to open the Strait of Hormuz. There were more missile attacks on Iran last night than on any other night since the war started and much of it was the military bunkers and radar near the oil refining infrastructure on Karg island, pushing Oil prices higher and taking rates with it.

I think the spike today will be short lived. Either Iran capitulates and oil drops or the US takes control of the Oil and it drops. It may take a bit to settle (the elevator up and the stairs down analogy) but it is coming soon.

Market Analysis – From a higher and better view:

Market Analysis – Quick Snapshot

- Fed: The Fed is still at 3.50% to 3.75%, and the March 18 statement said growth has been solid, job gains have remained low, inflation is still somewhat elevated, and uncertainty tied to the Middle East remains high.

- Inflation: The latest official CPI is 2.4% headline and 2.5% core year over year for February. The latest official PCE is 2.8% overall for January, while Reuters reported core PCE at 3.1%. New York Fed President John Williams said today the war-driven energy shock will push headline inflation higher this year and could take it above 3% in the near term.

- Mortgage rates: Freddie Mac’s latest weekly survey shows the 30-year fixed at 6.46% and the 15-year fixed at 5.77% as of April 2. The MBA’s more real-time weekly read had the 30-year at 6.57%, the highest since August.

- Housing: Existing-home sales were running at a 4.09 million annual pace in February, inventory was 1.29 million homes or 3.8 months’ supply, pending sales rose 1.8%, and new-home sales were 587,000 with 9.7 months’ supply. Builders are still working the incentive muscle: 37% cut prices in March and 64% used incentives.

- Big drivers today: mixed durable goods, hotter inflation signals from recent services data, oil above $110, physical crude near $150, and Trump’s Iran deadline tonight.

The big takeaway:

Today’s market story is basically this: the pre-war February manufacturing data looked okay, but the current market is trading the war, oil, and inflation risk far more than it is trading one factory report. That is why rates still feel tense even when the economic data is not outright ugly.

🎯 What Happened Today?

This morning’s headline data was the delayed February durable goods report. Headline orders fell 1.4%, mostly because commercial aircraft orders got smoked, but the parts of the report that matter more for business investment were better: core capital goods orders rose 0.6% and core shipments rose 0.9%. Ex-transportation durable goods orders rose 0.8%. In plain English, business investment looked reasonably firm heading into the Iran shock.

The problem is that markets are not living in February anymore. Reuters reported oil above $110 this morning, Wall Street opened mixed to lower, the dollar stayed near recent highs, and traders are no longer pricing any Fed cuts this year as the war-and-energy story keeps feeding stagflation nerves.

Translation:

Today’s domestic data said, “the economy wasn’t falling apart.” The market replied, “cool, but have you seen oil?”

🏦 Market Analysis – Fed Watch

The official Fed stance has not changed since March 18: rates are unchanged, inflation is still above target, and uncertainty around the outlook is elevated. The Fed specifically said the implications of developments in the Middle East for the U.S. economy are uncertain and that it is watching both sides of its dual mandate.

But the tone from officials has gotten more caution-colored than comfort-colored. Chicago Fed President Austan Goolsbee said inflation is going from “orange to red lately,” while Cleveland Fed President Beth Hammack said inflation is at a brighter, more vibrant orange because it has been above target for five years and mostly sideways for two. Today, John Williams added that the war’s energy shock will lift headline inflation this year, could push it above 3% in the near term, and does not create any imminent need to change policy because current policy is “well positioned.”

Plain English:

The Fed is not in rescue mode. Right now it is much more worried about reigniting inflation than about trimming rates to make everyone feel better. Jerome Powell is not exactly riding in on a white horse here; more like a very cautious spreadsheet.

📈 Market Analysis – Where Mortgage Rates Actually Are

Here’s where all the macro drama turns into actual payment math:

- Freddie Mac weekly average: 6.46% for a 30-year fixed and 5.77% for a 15-year fixed as of April 2.

- MBA weekly application market: 6.57% average contract rate for a 30-year fixed in the week ended March 27. Reuters said that was the highest since August.

- Reuters also reported mortgage rates have climbed by nearly half a percentage point since the war began on February 28.

Real-world takeaway:

Rates had started to behave a little better earlier in March, and then oil, inflation fear, and Fed patience walked back into the room and sat in everyone’s favorite chair.

🏠 Market Analysis – Housing Market Check

The good news:

- Existing-home sales rose 1.7% in February to a 4.09 million annual pace.

- Pending home sales rose 1.8% in February, with gains in the Midwest, South, and West.

- Inventory improved to 1.29 million homes, equal to 3.8 months’ supply.

The not-as-fun news:

- New-home sales fell to 587,000 in January, and supply rose to 9.7 months.

- Builder sentiment in March was still just 38, below the 50 break-even line.

- Builders are still bribing the market with charm and concessions: 37% cut prices, the average cut was 6%, and 64% used incentives.

What that means:

Housing is still moving, but it remains extremely payment-sensitive. More inventory is helping, but higher mortgage rates are still standing at the door asking buyers for ID, proof of income, and emotional resilience.

🌍 Political + Global Market Backdrop

This is where the whole thing gets spicier than lenders would prefer. Reuters reported that Trump’s deadline for Iran to agree to reopen the Strait of Hormuz expires Tuesday night, while Iran is rejecting a temporary ceasefire and seeking a lasting end to the war instead. Markets are in a wait-and-see mood because any escalation could threaten Gulf energy infrastructure even more.

That is why oil remains such a problem. Brent was up to $111.69 this morning, more than 50% above where it was when the war started, and Reuters separately reported that some physical crude grades in Europe and Asia are trading near $150 a barrel because refiners are scrambling for immediate supply after at least 12 million barrels per day, about 12% of global supply, were effectively shut in by Hormuz disruptions.

Why that matters:

Mortgage rates do not need a fresh Fed meeting every day to move higher. Sometimes oil, war, and one deadline with bad vibes are more than enough.

🔮 Market Analysis – What This Means for Rates Going Forward

Base Case

My base case is that rates stay choppy and elevated near term. Durable goods were not bad, but the bigger forces are still oil, rising input costs, and a Fed that sounds far more inflation-sensitive than growth-sensitive. That is an inference based on today’s durable goods report, yesterday’s ISM services price spike, and current Fed commentary.

Best Case

The friendlier path for rates would be an actual off-ramp in the Iran conflict, oil cooling materially, and Friday’s CPI coming in softer than feared. That would give bonds room to rally and mortgage pricing room to exhale. This is an inference supported by how markets have been reacting to oil and inflation risk.

Worst Case

The uglier path is also pretty obvious: the deadline passes badly, energy infrastructure risk escalates, oil spikes again, and Friday’s CPI confirms that the inflation hit is spreading. In that setup, mortgage rates likely stay under pressure or worsen. This is an inference based on current oil dynamics, market pricing, and Fed rhetoric.

Bottom line:

This still looks like a market where one decent economic report can help for a few minutes, and one ugly oil headline can body-check it before lunch.

🧠 Practical Takeaways

For buyers:

This is still a strategy market, not a perfection market. More inventory exists than there used to be, but payment matters more than ever and rate volatility is still very real.

For agents:

The best conversations right now are about structure: concessions, buydowns, price realism, and monthly-payment math. Buyers are still there, but they are not casually strolling through a 6.5% world pretending math is a lifestyle choice.

For homeowners thinking about refinancing:

This week is another reminder that rate windows can close fast when macro fear returns. The market rarely sends a warning text before changing its mind.

🔒 Lock vs Float

Lock if:

- closing is within 30 days

- the borrower is payment-sensitive

- the file is tight on qualifying

- the deal cannot absorb more volatility

That case is stronger while Freddie Mac is at 6.46%, MBA is at 6.57%, and the market is staring at an oil-sensitive geopolitical deadline.

Float cautiously if:

- the borrower has more time

- the file is strong

- everyone understands the risk

- the borrower can handle short-term swings

That is a measured-risk call, not a “let’s manifest a rally” call. The Fed, oil market, and inflation setup still argue for caution.

Simple rule:

If a worse rate creates a real problem, lock. If the borrower has time and flexibility, a cautious float can still make sense.

Stay safe and make today great!