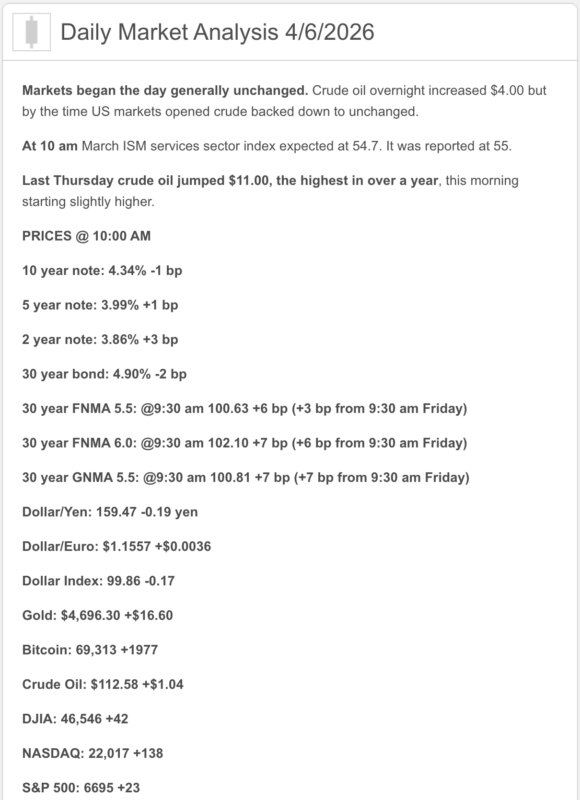

Good Monday morning from your Hometown Lender. Here is your Monday market analysis.

Friday saw rate sheets take a bit of a hit after the jobs data came in stronger than expected, but markets were closed, and today, those losses are all but gone. Friday was a calm day.

Risk today is moderate; the biggest time to worry about is around 10 am when President Trump is going to hold a news conference about Iran. He unofficially pushed back the deadline for action from Iran to tomorrow; we’ll possibly hear more about that when he speaks.

Volatility is high. Rates will improve, but it is not a straight line.

Market Analysis – From a higher and better view

Market Analysis – Quick Snapshot

- Rates: The bond market is starting the week on the defensive. After Friday’s stronger-than-expected jobs report pushed the 10-year Treasury to about 4.35%, today’s tone is still more “higher for longer” than “rate relief is here.”

- Stocks: As of 10:02 a.m. ET, the Dow was up 0.15%, the S&P 500 up 0.31%, and the Nasdaq up 0.52% as investors weighed possible Iran ceasefire talks against sticky inflation risk.

- Jobs: March payrolls rose 178,000, unemployment held at 4.3%, and average hourly earnings rose 0.2% month over month and 3.5% year over year. Weekly initial jobless claims also came in low at 202,000. Translation: the labor market is not exactly waving a white flag.

- This morning’s data: ISM services slowed to 54.0 from 56.1, but the prices-paid index jumped to 70.7, the highest since October 2022. The New York Fed’s Global Supply Chain Pressure Index also rose to 0.68 from 0.54 in February. So growth cooled a bit, but inflation nerves got louder.

- Fed: The Fed’s target range remains 3.50% to 3.75%, and its March statement said inflation remains “somewhat elevated” while uncertainty is elevated. This week’s next catalysts are FOMC minutes on April 8, PCE on April 9, and CPI on April 10.

- Mortgage / housing: Freddie Mac’s weekly survey has the 30-year fixed at 6.46% and the 15-year fixed at 5.77%. MBA’s prior-week survey showed application volume down 10.4%, purchases down 3%, and refis down 17%. Existing-home sales for February ran at 4.09 million, with 1.29 million homes for sale, 3.8 months of supply, and a $398,000 median price.

1) Market Analysis – What Hit This Morning

This morning’s market message was basically: the economy is still expanding, but inflation is acting like it had espresso before sunrise. Services activity stayed in growth territory at 54.0, but the price component surged, which matters because services inflation is exactly the kind of thing the Fed does not ignore. Add in the New York Fed’s hotter supply-chain reading, and bonds had every reason to stay grumpy.

Narrative you can use:

“Today’s data were mixed in the most annoying way for rates: growth slowed a little, but pricing pressure heated up. That keeps the Fed patient and keeps mortgage-rate improvement from arriving with any real urgency.”

2) Fed Watch

The Fed is still officially in wait-and-see mode. At the March 17–18 meeting, it held the fed funds target at 3.50% to 3.75% and said inflation remains somewhat elevated. Friday’s jobs report plus today’s hotter services-price data make it harder to argue for near-term easing.

Street thinking has shifted in a hawkish direction fast. Reuters reported that Wells Fargo no longer expects any Fed cuts in 2026, while Citigroup pushed its expected start of cuts back to September from June. That does not make it gospel, but it tells you where expectations are moving.

3) Where Mortgage Rates Actually Are

Freddie Mac’s survey has the 30-year fixed at 6.46% and the 15-year fixed at 5.77% as of April 2. MBA’s more market-sensitive weekly survey showed the contract rate on a 30-year mortgage at 6.57% for the week ended March 27, with demand falling as rates climbed.

The practical takeaway: mortgage pricing is still being driven more by the 10-year Treasury, oil, inflation expectations, and risk premium than by any theoretical future Fed cut. In other words, borrowers do not get to refinance off vibes.

4) Market Analysis – Housing Market Check

Housing is still moving, but it is not exactly gliding. February existing-home sales rose 1.7% to a 4.09 million annual pace. Inventory increased to 1.29 million units, or 3.8 months’ supply, and the median price rose to $398,000. Affordability improved to 117.6, the best reading since March 2022.

There is also a useful regional nugget for Western markets: the West posted an 8.2% month-over-month increase in sales, while the regional median price was down 1.9% year over year. That is not a crash headline, but it is a reminder that some local markets are softening at the margin even while national supply remains tight.

5) Political Backdrop & Fed Independence

The biggest political-macro story is still the Iran / Strait of Hormuz situation. Reuters reported Monday that a framework is being discussed that could create an immediate ceasefire and reopen the Strait of Hormuz, but as of the report, it was still only a proposal. At the same time, oil remained elevated, with Brent at $109.13 and WTI at $112.31 in Monday trading.

That matters for rates because energy feeds inflation expectations fast. Reuters also reported that the Hormuz disruption has pushed oil well above $100 and helped drive fears of stagflation, while Dimon warned in his annual letter that the Iran war could mean higher inflation and higher interest rates than markets currently expect.

Trade policy is still part of the inflation backdrop too. After the Supreme Court struck down Trump’s prior tariff program, Reuters reported he replaced it with a temporary 10% global import duty for 150 days while launching new trade probes. On top of that, Trump’s new budget proposal asks for a 10% cut in non-defense spending and a jump in military spending to $1.5 trillion. For bonds, that is not exactly a spa package.

6) Market Analysis – What This All Means for Rates Going Forward

- Base case:

Mortgage rates stay choppy to slightly elevated near term. Strong jobs, hot services prices, higher oil, and fresh supply-chain pressure are all arguing against a clean rally in bonds. Reuters’ poll also has this Friday’s March CPI expected at 0.9% headline and 0.3% core, which keeps the inflation spotlight bright. - Better case for rates:

Ceasefire talks stick, the Strait reopens, oil backs off, and this week’s PCE and CPI prints come in softer than feared. If that happens, the market can start unclenching a bit and Treasury yields could ease. That is an inference, but it is grounded in what markets are currently reacting to. - Worse case for rates:

Oil stays above $100, supply chains tighten further, and services-price pressure bleeds into broader inflation data. In that setup, the Fed stays patient even longer, mortgage spreads stay sticky, and the “maybe next week” crowd gets another character-building experience.

7) Market Analysis – Practical Takeaways

- For buyers: this is still a market where structure matters. Concessions, buydowns, product choice, and strategy can matter more than waiting around for a miracle quarter-point drop.

- For agents: the labor market is still supportive, affordability is better than a year ago, and inventory is improving. But rates are high enough that monthly-payment sensitivity is still the main character.

- For referral partners and current homeowners: the market is not frozen, but it is selective. Smart financing still wins deals; lazy financing still writes motivational quotes and loses them.

8) Lock vs Float

- 0–15 days from closing:

I would lean lock. Too many moving parts this week, and most of them are inflation-sensitive. - 15–30 days:

This is a case-by-case zone. If the borrower is tight on DTI or highly payment-sensitive, I would still lean protective. If they have room and can tolerate movement, April 9 and April 10 are real volatility points. - 30+ days:

A cautious float can make sense, but only if you are actively watching the data and have a line in the sand. This market can turn on one inflation print or one Middle East headline.

Stay safe and make today great!