Good Monday AM from your Hometown Lender. Let’s dive into this week’s market analysis!

Bonds continued to improve through Friday afternoon to end the week close to unchanged after earlier losses.

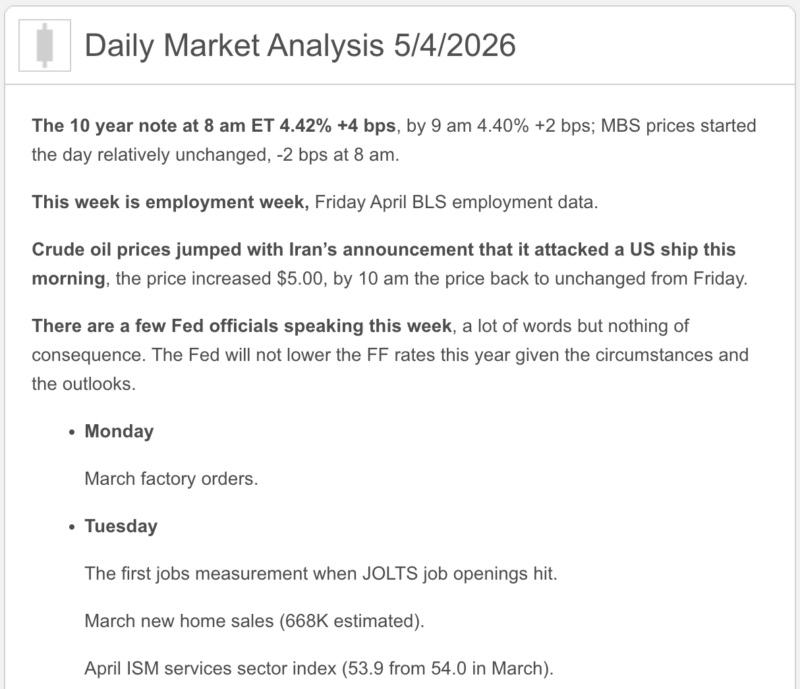

Monday morning is always interesting in the market analysis as weekends are seemingly the preferred time to drop news. The President said the US would escort traffic through the Strait. The Iran said it attacked and hit a US military ship. I don’t know if the first will be true and I’m confident the second is not.

Nonetheless, markets are not liking the disruption. Bonds are struggling today just like Sisyphus to get to the top of the mountain. There is a lot of data this week and while the markets have been quick to ignore it recently, the jobs report will get some attention. I think this week will have increased volatility.

Market Analysis – From a higher and better view:

Market Analysis – Quick Snapshot

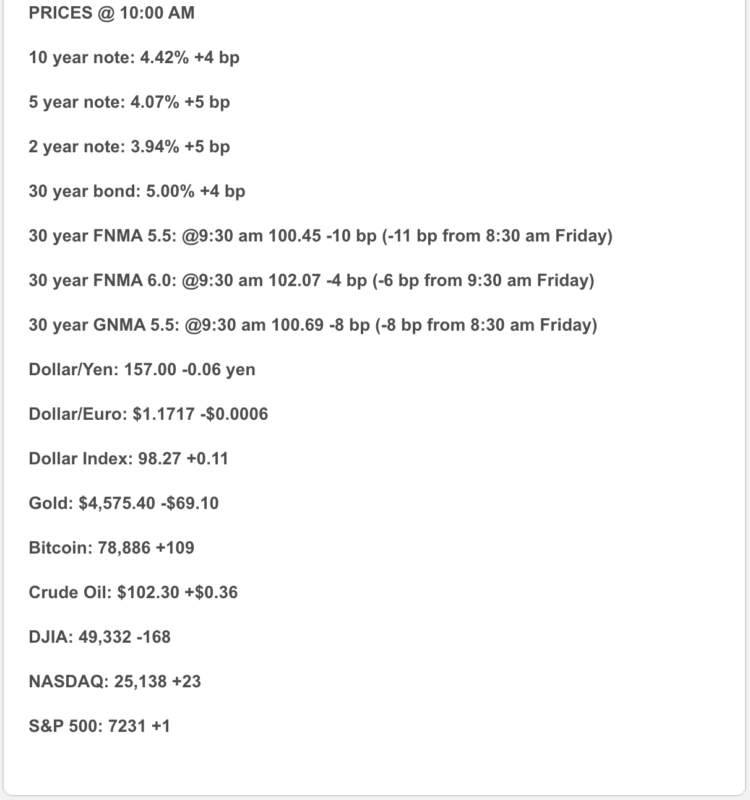

- Oil is back in charge. Brent jumped about 2%, U.S. stocks were mixed, and the 10-year Treasury yield rose to 4.414% after the U.S. disputed Iran’s claim that it halted an American warship in the Strait of Hormuz. Reuters said the Dow was down 0.5%, the S&P 500 slipped slightly, and the Nasdaq edged up 0.12%.

- This morning’s U.S. data were better than expected. March factory orders rose 1.5%, the strongest monthly gain since November, with computers and electronics up 3.6% as AI-related investment stayed strong.

- The Fed story is getting more hawkish, not less. Barclays became the latest major brokerage to forecast no Fed cuts in 2026, pushing its first expected cut to March 2027 after last week’s divided Fed hold.

- Mortgage rates are still improved from early April, but not exactly cozy. Freddie Mac’s latest weekly survey shows the 30-year fixed at 6.30% and the 15-year fixed at 5.64% as of April 30.

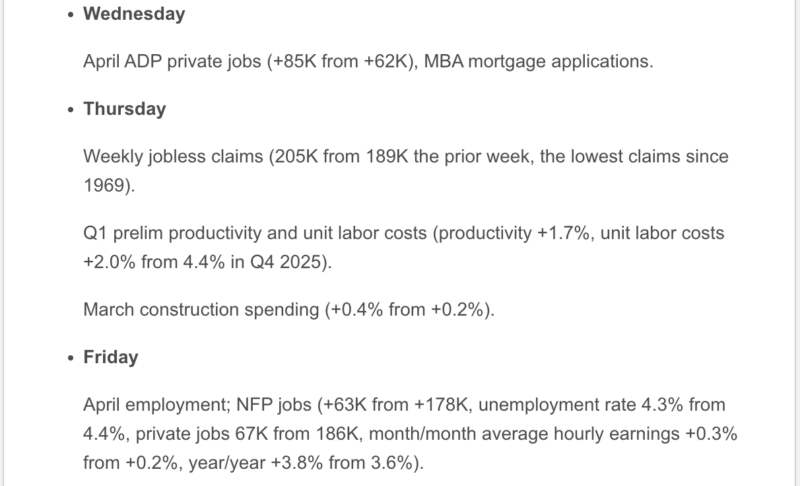

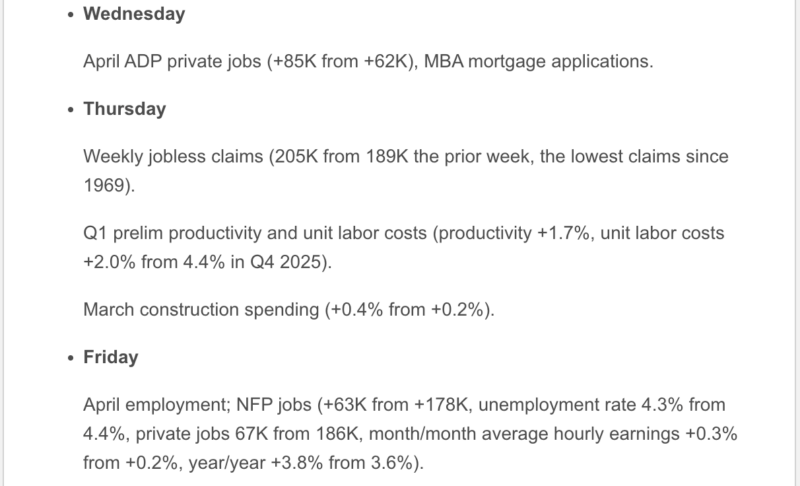

- This week matters. Reuters says the market is watching trade figures, ISM services, JOLTS, ADP, jobless claims, and Friday’s jobs report, with median payroll expectations around +60,000 and unemployment expected at 4.3%.

1) Market Analysis – What Hit This Morning

Today’s cleanest domestic read was factory orders, and it was a solid one. Orders rose 1.5% in March, with notable strength in electronics and instruments, which reinforces the idea that business investment — especially AI-linked spending — is still helping the economy. That is good news for growth, even if it is not automatically good news for rates.

The bigger market mover, though, is still oil. As long as Hormuz headlines are pushing crude higher, bonds are likely to care more about inflation risk than about one decent U.S. data point. Today’s setup is basically: factory orders say growth is alive; oil says inflation is too.

2) Fed Watch

The Fed held rates at 3.50% to 3.75% last week, but the tone after that meeting has shifted more toward longer restraint than late-year relief. Barclays now expects no cuts in 2026, joining the camp that thinks energy-driven inflation keeps the Fed sidelined well into next year.

The political overlay is still very real. Reuters reported over the weekend that the criminal probe into Jerome Powell was dropped, but the Fed Inspector General review remains live, and Powell has said he plans to remain a governor after his chair term ends on May 15. That keeps both Fed independence and the Warsh transition squarely in focus.

3) Market Analysis – Where Mortgage Rates Actually Are

The latest Freddie Mac benchmark still has the 30-year fixed at 6.30% and the 15-year fixed at 5.64%. That is not low, but it is still better than the uglier early-April stretch.

The practical issue is that mortgage pricing is still being driven more by oil, inflation expectations, and Treasury yields than by wishful chatter about Fed cuts. With the 10-year at 4.414% today and oil back up, the market is reminding everyone that rate relief still bruises easily.

4) Market Analysis – Housing Market Check

There is no major fresh housing release driving today’s tape, so the best current mortgage/housing read is still Freddie Mac’s weekly survey and the broader theme of a spring market that is functioning but still payment-sensitive. The main takeaway today is not a new housing data surprise — it is that rates and affordability remain hostage to energy and bond-market volatility.

5) Political Backdrop & Fed Independence

The macro story is still the Strait of Hormuz. Reuters says the latest U.S.-Iran clash over naval activity pushed crude higher again, and markets remain highly sensitive to any sign that supply disruptions could persist. That is the political story most directly feeding into rates this morning.

On the Fed side, the Powell/Warsh transition remains a live market variable. Reuters says the dropped criminal case cleared the way for Kevin Warsh’s confirmation path, even though the separate IG review continues. In other words, this is not just about today’s inflation risk — it is also about who will be steering policy soon.

6) Market Analysis – What This All Means for Rates Going Forward

Base case: mortgage rates stay choppy to slightly elevated because oil is climbing, yields are firm, and the Fed is sounding less interested in cuts. Better case: Hormuz tensions cool and this week’s labor data come in soft enough to calm the bond market. Worse case: crude stays hot, jobs hold up, and the market pushes the first cut even farther out.

7) Market Analysis – Practical Takeaways

For buyers, this is still a market where structure beats hope. The Freddie rate is a little better than the recent highs, but the monthly payment story is still sensitive to every oil spike and yield move.

For agents and partners, this week is about jobs and inflation expectations. If the data soften, rates could breathe a bit. If not, the “higher for longer” crowd will keep winning the microphone.

8) Lock vs Float

0–15 days: lean lock.

15–30 days: case by case.

30+ days: cautious float, but only if the borrower can handle headline-driven swings. Right now, oil is still the loudest voice in the room.

Stay safe and make today great!