Good Thursday morning from your Hometown Lender. Let’s get today’s market analysis started!

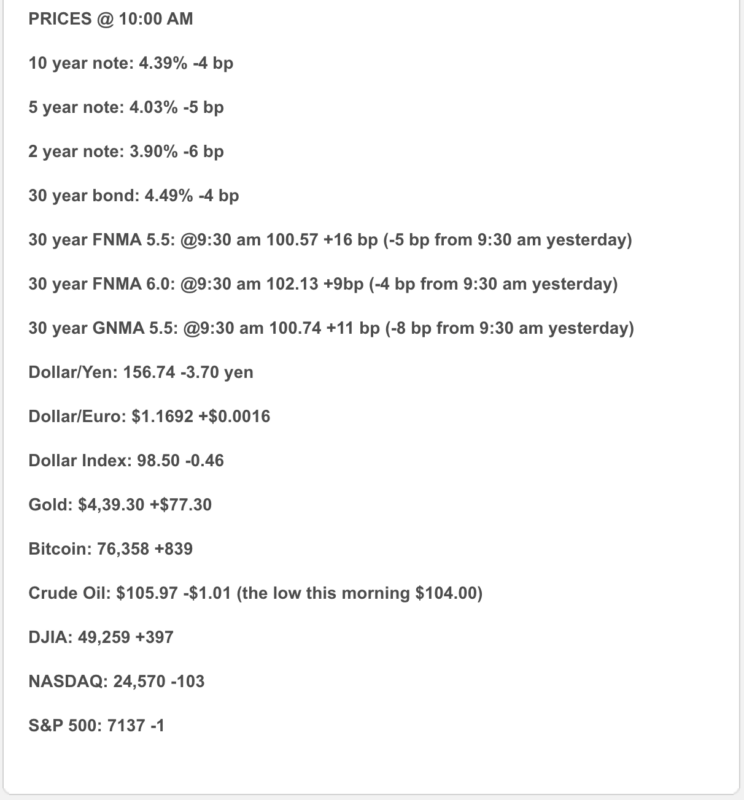

Yesterday bonds lost ground early (-31 bps at the open) and well before the Fed meeting. They held steady for a bit but started falling again ahead of the Fed policy statement at 2pm. Bonds again drifted a bit lower early as Powell shared his prepared remarks but were basically flat through the rest of the press conference. Then right before the end of the day, bonds sold off once again to drop to the worst levels of the day. Mortgage bonds enjoying a bit of a rebound this morning. The likely reasons are due more to an overreaction yesterday and month’s end trading than a reversal although we can hope.

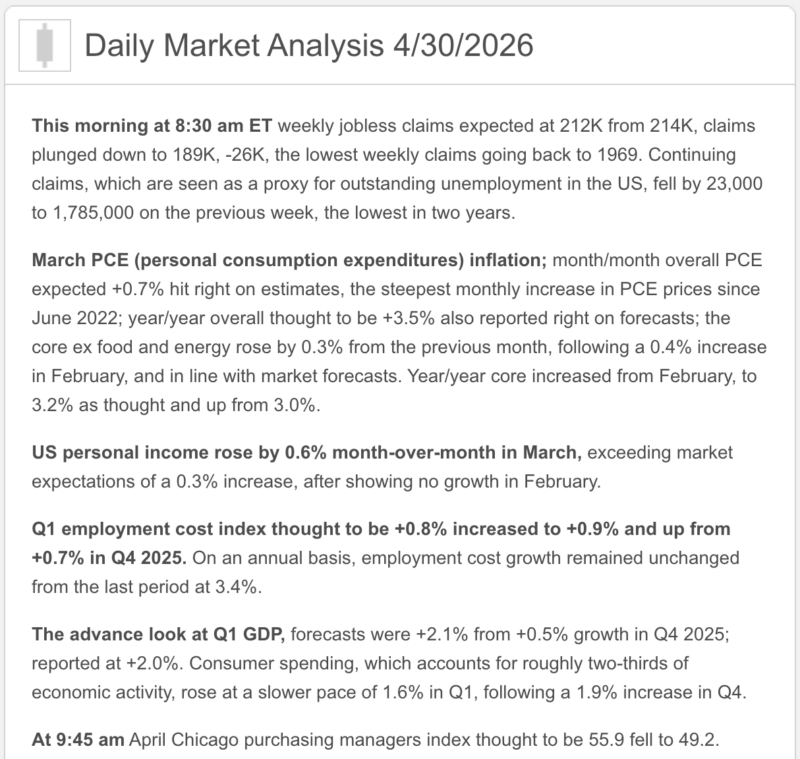

This morning’s market analysis – GDP data came in showing the economy is doing just fine, and jobless claims were the lowest level since ’69. It’s hard to argue that the Fed needs to cut rates when the economy continues to push through trouble spots caused by tariffs and the Iran conflict, and the labor market isn’t falling apart. Incoming Fed Chair (still pending full Senate confirmation but made it through the Banking Committee) Kevin Warsh will have his hands full trying to convince other voting members of the Fed that rate cuts are necessary.

Market Analysis – From a higher and better view:

Market Analysis – Quick Snapshot

- Growth picked up, but inflation picked up with it. Real GDP rose at a 2.0% annualized rate in Q1, up from 0.5% in Q4. But the GDP report also showed Q1 PCE inflation at 4.5% annualized and core PCE at 4.3%, while real final sales to private domestic purchasers rose 2.5%.

- This morning’s monthly inflation read was not exactly bond-friendly. March personal income rose 0.6%, consumer spending rose 0.9%, and real spending rose only 0.2%. The headline PCE price index rose 0.7% month over month and 3.5% year over year, while core PCE rose 0.3% on the month and 3.2% from a year earlier.

- Labor costs ran a little hotter than expected, while layoffs stayed low. The Employment Cost Index rose 0.9% in Q1, up from 0.7% in Q4, with benefits up 1.2% and wages and salaries up 0.8%. Weekly jobless claims fell to 189,000, and continuing claims fell to 1.785 million.

- The Fed held rates steady yesterday at 3.50% to 3.75%, but the tone was more hawkish than cuddly. The statement said inflation is elevated, in part because of higher global energy prices, and that Middle East developments are adding high uncertainty. Powell also said yesterday was his last press conference as Chair and that he plans to remain a governor for a period of time after May 15.

- Mortgage rates are still better than the early-April spike, but they are not exactly relaxed. The latest available Freddie Mac weekly survey shows the 30-year fixed at 6.23% and the 15-year fixed at 5.58%. Freddie Mac says that is the lowest 30-year reading of the last three spring homebuying seasons.

- Housing is still mixed. March single-family housing starts jumped 9.7% to a 13-month high, but single-family permits fell 3.8%, and FHFA said national home prices were flat month over month in February and up 1.7% year over year.

- Markets are still trading oil, earnings, and the Fed all at once. At 10:14 a.m. ET, the Dow was up 0.88%, the S&P 500 was flat, and the Nasdaq was down 0.31%. Oil retreated from its intraday peak but still hovered around $110 a barrel after hitting a nearly four-year high.

1) Market Analysis -What Hit This Morning

Today’s data drop was one of those “good headline, annoying details” mornings. GDP rebounded to 2.0%, helped by stronger government spending, investment, exports, and consumer spending. But the same report showed that quarterly inflation ran hotter, with the gross domestic purchases price index up 3.6%, headline PCE up 4.5%, and core PCE up 4.3% at an annualized pace. That is the kind of combo that keeps the Fed from doing anything dramatic besides practicing patience.

The monthly PCE report told a similar story. Income and spending both rose, which says the consumer is still functioning, but real spending only grew 0.2%, because higher prices ate a lot of the nominal gain. In other words, consumers are still spending, but inflation is still sneaking a cover charge into the evening.

On labor, the message remains: low fire, low hire. Claims fell to 189,000, continuing claims dropped, and the unemployment rate looks consistent with holding near 4.3%. At the same time, the ECI came in a touch hot at 0.9%, driven more by benefits than a wage breakout. That is not a wage spiral, but it is also not the kind of labor-cost report that screams “all clear.”

Narrative you can use:

“Today’s data said the economy is still moving, but inflation is still too warm for comfort. Growth rebounded, consumers kept spending, and layoffs stayed low, but hotter PCE and labor-cost data mean the Fed is still not in a hurry to give the market what it wants.”

2) Fed Watch

Yesterday’s Fed decision was a hold, but not a quiet one. The Fed kept the target range at 3.50% to 3.75% and said inflation is elevated partly because of higher global energy prices, while Middle East developments are contributing to a high level of uncertainty.

The more important wrinkle is that the decision was highly divided. The Fed statement shows Stephen Miran wanted a quarter-point cut immediately, while Beth Hammack, Neel Kashkari, and Lorie Logan supported holding rates but opposed keeping an easing bias in the statement. Reuters says it was the Fed’s most divided decision since 1992. That is not the kind of vote split that makes near-term cuts look easy.

Powell also made clear that yesterday was his last press conference as Chair, and he said he plans to remain on the Board as a governor for a period of time after May 15. Meanwhile, Warsh is moving closer to taking over. Reuters says he cleared the Senate Banking Committee and could be confirmed by the full Senate as early as the week of May 11.

The Street has noticed. Reuters reports broker forecasts are now split between no cuts at all in 2026 and a small amount of easing later in the year, while futures pricing after the Fed meeting ruled out cuts for the rest of 2026. That is a meaningful reset from where consensus sat earlier this year.

3) Market Analysis -Where Mortgage Rates Actually Are

The latest available Freddie Mac weekly survey still shows the 30-year fixed at 6.23% and the 15-year fixed at 5.58%. Freddie Mac said that improvement, plus stronger pending sales and better application activity, points to some improving momentum in housing.

That is the good-news version. The less-cuddly version is that mortgage pricing is still being pushed around more by oil, inflation expectations, and Treasury-market mood than by wishful chatter about Fed cuts. Today’s GDP/PCE/ECI combo does not really give bonds a clean reason to celebrate, and oil near $110 is still the market’s least-favorite plus-one.

4) Market Analysis -Housing Market Check

Housing gave us a very mixed signal. On one hand, single-family starts rose 9.7% in March to 1.032 million, the strongest in 13 months. On the other hand, single-family permits fell 3.8%, which suggests builders still do not trust the road ahead. That is basically housing saying, “I’ll show up, but I’m not promising to stay late.”

On prices, FHFA said home values were flat month over month in February and up 1.7% year over year. So national appreciation is no longer sprinting, but affordability still is not exactly breezy.

The broader backdrop remains rate-sensitive. Pending home sales rose 1.5% in March, but existing-home sales previously fell 3.6% to 3.98 million, inventory rose to 1.36 million, and supply climbed to 4.1 months. That is still a market that is moving, just with one hand on the railing.

5) Market Analysis -Political Backdrop & Fed Independence

The macro story is still Iran, Hormuz, and energy. Reuters says oil hit a four-year high today on worries the U.S. may extend the blockade of Iranian ports, and another Reuters poll says analysts have lifted their oil-price forecasts because they increasingly expect the disruption to last longer.

That matters because it feeds directly into inflation and Fed policy. Reuters notes the surge in energy prices is making it harder for markets to keep hoping for a dovish Fed, even with a chair transition underway. Put simply: Warsh may change the tone, but oil is still changing the math.

The Fed-independence question is also not going away. Warsh’s path is getting clearer, Powell says he will stay on as a governor for a period of time, and Reuters says investors are now trying to price not just the Fed we have, but the Fed we might have by June. Bonds do not love uncertainty, and this is uncertainty wearing a necktie.

6) Market Analysis – What This All Means for Rates Going Forward

Base case:

Mortgage rates stay choppy and a little vulnerable. GDP was decent, claims were solid, and housing starts were better, but PCE, ECI, and oil all leaned in the wrong direction for a clean bond rally.

Better case for rates:

The better path is that oil backs off, Middle East shipping risk eases, and the next inflation prints show today’s heat was more energy shock than broad re-acceleration. That is an inference, but it is grounded in how heavily markets are reacting to oil and in the fact that core monthly PCE was 0.3%, not something uglier.

Worse case for rates:

If crude stays hot, the Fed’s hawks gain more traction, and next week’s labor data stay firm, mortgage rates could give back some of the recent improvement pretty quickly. Reuters already says a growing share of brokerages now expects no cuts in 2026, and markets have largely priced out cuts this year.

The next big checkpoints are Friday, May 8, for the April jobs report, and before that the market will keep trading today’s inflation data and the oil tape.

7) Market Analysis -Practical Takeaways

For buyers, this is still a market where structure beats hope. The weekly Freddie Mac rate is better, but not low enough to make payment sensitivity disappear, and today’s oil move is a reminder that rate relief can be a little moody.

For agents, today’s message is balanced: the consumer is still spending, business investment looked better, and housing starts improved, but inflation is still sticky and affordability is still doing heavy defensive work. This market is alive. It just is not exactly breakdancing.

For refi and move-up conversations, the honest message is still not “rates are about to tumble.” The smarter message is that windows may open, but they are still being driven more by oil and bond sentiment than by any clean Fed pivot.

8) Lock vs Float

0–15 days from closing:

I would still lean lock. Hot oil, hotter-than-comfortable inflation data, and a newly more divided Fed are not the ingredients I would choose for extra adventure.

15–30 days:

This is still case by case. If the borrower is tight on DTI or very payment-sensitive, I would favor protection. If they have room, there is at least a reasoned case for cautious patience — but it is patience with a helmet on.

30+ days:

A cautious float can make sense, but only with discipline. Right now the market is trading oil, Fed succession, and inflation data all at once.

Stay safe and make today great!