Good Tuesday morning from your Hometown Lender. Here is today’s market analysis!

Yesterday was a calm, boring day. Mortgage bonds picked up a few more basis points in the late afternoon, but nowhere near enough to make any lenders think about repricing better. Rates today likely similar to yesterday, maybe a bit worse as bonds slip a bit around 10am as lenders start to issue pricing. Reprice risk on the day is low, nothing happening on the economic calendar, quiet headlines… just bonds drifting through a summer day.

Market Analysis – From a higher and better view:

Market Analysis –Quick Snapshot

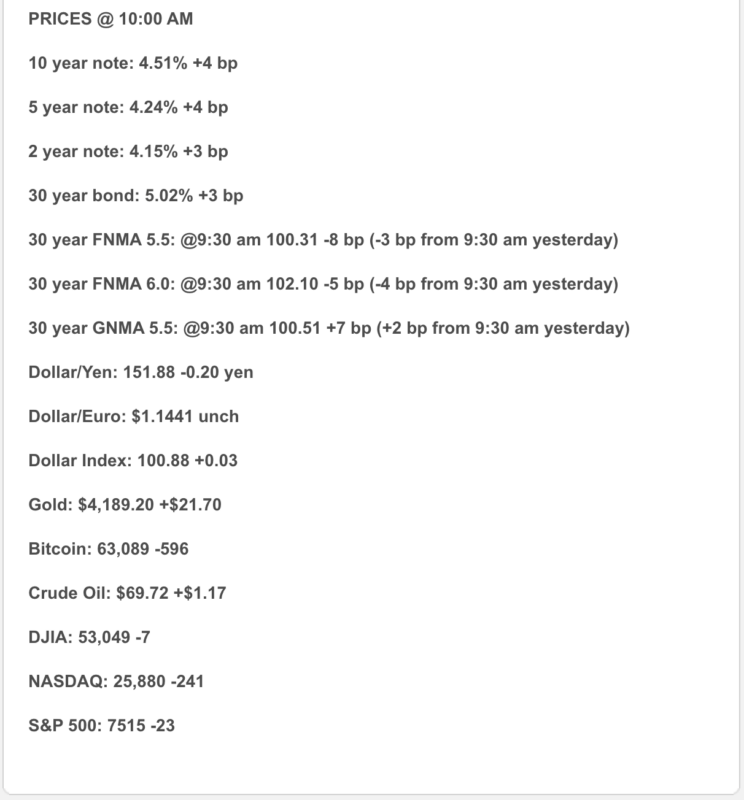

Bonds: The 10-year Treasury is back around 4.50%, with longer-term yields moving higher as inflation expectations ticked up and oil prices rose after renewed shipping tension near the Strait of Hormuz. Bonds were hoping for calm seas and got a geopolitical cannonball.

Mortgage Rates: Daily tracking shows the 30-year fixed around 6.61% and the 15-year fixed around 5.92%. Freddie Mac’s latest weekly survey showed the 30-year fixed at 6.43% and the 15-year fixed at 5.79%, so daily pricing is running noticeably hotter than the weekly average.

Inflation Expectations: The New York Fed’s June survey showed one-year inflation expectations rising to 3.7%, the highest since September 2023. That matters because inflation expectations are one of the Fed’s “do not ignore” dashboard lights.

Fed Watch: New York Fed President John Williams sounded a little more comfortable on inflation because energy prices had been retreating, but he also emphasized policy remains data-dependent. Translation: the Fed is not cutting because everyone asks nicely.

Oil / Geopolitics: Oil moved higher after reported attacks on vessels near the Strait of Hormuz, with Brent around the low-to-mid $70s and WTI near $70. Energy risk remains a key inflation and mortgage-rate driver.

Housing: Housing remains mixed. Buyers are active when payment, price, and inventory line up, but affordability is still the gatekeeper. This is not a dead market — it is a market that makes everyone show their math.

Market Analysis –What It Means

Today’s tone is a little more cautious. Higher oil, higher inflation expectations, and higher Treasury yields are keeping mortgage rates choppy in the mid-6s.

In plain English: the market is not panicking, but it is not handing out easy payments either.

Market Analysis –Housing & Mortgage Strategy

This remains a structure-the-payment market.

The best conversations right now are about:

Seller credits, temporary buydowns, permanent buydowns, builder incentives, ARM options where appropriate, and a realistic refinance plan if rates improve later.

Buyers are still active, but they are doing math. Sellers and builders who help solve the monthly payment problem have the best chance of turning interest into contracts.

Lock vs. Float

Lock bias: If closing within 30 days, the borrower is payment-sensitive, or the file is tight, locking remains the cleaner recommendation.

Float bias: Floating may make sense only with time, flexibility, and a clear trigger. Oil headlines, Fed commentary, and inflation expectations can still move bonds quickly.

Today’s guidance:

Bias toward locking short-term closings. For longer timelines, cautious floating may be reasonable only with a clear risk ceiling and daily monitoring.

Stay safe and make today great!