Good Tuesday AM from your Hometown Lender,

Yesterday started off with some red flags but at least bonds were in the green… and green is good, it means better pricing on the rate sheet. But then quickly, bonds started to sell off and hit the worst levels of the day.

So, since hitting a high point on Friday May 29th of 100.50, bonds were down almost -60bps in a little over a week, meaning rates had moved .125-.250 higher.

Market Analysis – From a higher and better view:

Market Analysis – Quick Snapshot

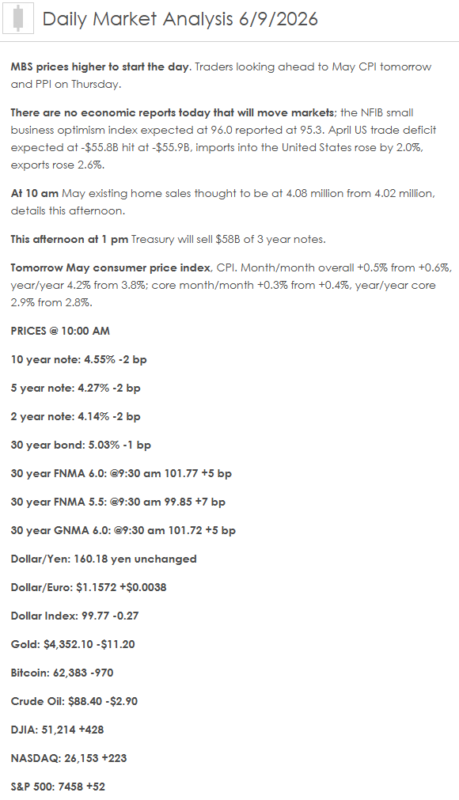

Bonds: The 10-year Treasury is holding around the mid-4.5% range, near 4.55%, as markets wait for tomorrow’s CPI report and continue digesting strong labor data, sticky inflation risk, and oil/geopolitical headlines. Bonds are not panicking, but they are definitely not lounging by the pool either.

Mortgage Rates: Daily tracking shows the 30-year fixed around 6.57% and the 15-year fixed around 5.94% today. Freddie Mac’s latest weekly survey showed the 30-year fixed at 6.48% as of June 4, so real-time pricing is running a bit hotter than the weekly average.

Fed Watch: A Reuters economist poll now shows a strong majority expecting the Fed to keep its 3.50%–3.75% target range unchanged for the rest of 2026. The market has moved from “when are cuts coming?” to “could the next move actually be higher?”

Inflation: Tomorrow’s CPI report is the big event. Economists expect May CPI to rise around 4.2% year over year, which would be the hottest reading since 2023. Inflation is still the guest who said goodbye and then started another conversation at the door.

Small Business: Small-business optimism slipped in May, and more owners are planning price increases. That matters because it suggests inflation pressure may still be spreading through the real economy.

Markets: Stocks are mixed after an early tech rally faded. Investors still like the AI growth story, but higher rates and inflation uncertainty are keeping the market a little jumpy.

1) Market Analysis – What Hit This Morning

Today’s market theme is waiting on inflation.

We did not get the big CPI number yet — that comes tomorrow — but markets are already positioning for it. The concern is that inflation may reaccelerate because of energy prices, tariffs, supply-chain pressure, and resilient demand.

Small-business data added to that concern. The NFIB Small Business Optimism Index fell to 95.3, still below its long-term average, while a growing share of owners reported raising prices or planning to raise prices. That is not the inflation story the Fed wants to hear before CPI day.

Narrative you can use:

The market is in a holding pattern today. Jobs are strong, inflation risk is still sticky, and tomorrow’s CPI report could shape the next move in bonds and mortgage pricing. In mortgage terms: this is a “have a plan before the data hits” market.

2) Fed Watch

The Fed remains in a cautious position. A fresh Reuters poll shows most economists now expect the Fed to hold rates steady for the rest of 2026. That is a major shift from earlier expectations that rate cuts could arrive this year.

Why the shift? Stronger jobs, higher oil prices, persistent inflation, and concern that cutting too early could damage Fed credibility.

Bottom line:

The Fed wants proof that inflation is cooling. Right now, the data is not giving it enough proof. The next major test is tomorrow’s CPI report.

3) Market Analysis – Where Mortgage Rates Actually Are

Daily mortgage-rate tracking shows the 30-year fixed around 6.57% and the 15-year fixed around 5.94% today. Freddie Mac’s latest weekly number, released last Thursday, showed the 30-year fixed at 6.48%, but weekly surveys can lag daily repricing.

Practical read:

Rates are workable, but not forgiving. The best conversation is not simply:

“What is the rate?”

It is:

What is the payment? What credits are available? Is a buydown smart? Does an ARM make sense? What is the refinance path if the market improves?

That is where deals are getting built right now.

4) Market Analysis – Housing Market Check

Housing remains payment-sensitive. Buyers are still active when price, inventory, credits, and monthly payment line up — but they are not chasing bad math.

What this means:

Sellers and builders who help solve the payment problem have the advantage. That may mean seller credits, temporary buydowns, permanent buydowns, builder incentives, or more realistic pricing.

This is not a dead market. It is a disciplined market. Buyers are not gone; they are doing the monthly payment calculation — sometimes twice, just to make sure it hurts the same both times.

5) Political Backdrop & Fed Independence

The political backdrop remains heavily tied to rates. Inflation, oil prices, tariffs, Middle East risk, and Fed independence are all part of the market conversation.

President Trump continues to call for lower rates, but the Fed is facing a very different math problem: strong jobs, elevated inflation, and oil risk. That makes it harder for the Fed to cut without looking like it is ignoring inflation.

Translation:

Mortgage rates are not just following housing data. They are following jobs, CPI, oil, tariffs, Treasury yields, Fed credibility, and global conflict. A rate sheet now apparently needs a policy analyst and a passport.

6) Market Analysis – What This All Means for Rates Going Forward

| Scenario | What Needs to Happen | Likely Rate Impact |

| Best Case | CPI comes in cooler, oil stays lower, Fed rhetoric calms | Mortgage rates drift lower |

| Base Case | CPI stays hot, Fed stays cautious, bonds remain range-bound | Rates stay choppy in the mid-to-upper 6s |

| Risk Case | CPI surprises higher, oil jumps, Fed sounds more hawkish | Rates push higher and repricing risk increases |

My read: base case remains choppy, not catastrophic. The market is waiting for CPI before making its next big move. Until then, mortgage strategy matters more than rate guessing.

7) Market Analysis – Practical Takeaways

For buyers:

Do not wait for the perfect rate. Perfect rates are like perfect inspection reports — beautiful, rare, and usually followed by fine print. Focus on payment, credits, buydowns, program fit, and long-term flexibility.

For homeowners:

Refinance decisions remain case-by-case. Cash-out, debt consolidation, HELOC alternatives, ARM reset planning, and future refinance strategy should all be reviewed individually.

For agents:

This is a payment strategy market. The strongest agents are not just saying, “rates are high.” They are showing buyers how credits, buydowns, price negotiation, and loan structure change the monthly payment.

8) Lock vs. Float

Lock bias: If closing within 30 days, the borrower is payment-sensitive, or the file is tight on ratios, locking remains the cleaner recommendation.

Float bias: Floating can make sense only with more time, stronger borrower flexibility, and a clearly defined trigger. With CPI due tomorrow, floating blindly is not strategy — it is cardio with disclosures.

Today’s guidance:

Bias toward locking short-term closings. For longer timelines, cautious floating may be reasonable only if the borrower understands tomorrow’s CPI risk and has a clear ceiling for pain.

Stay safe and make today great!