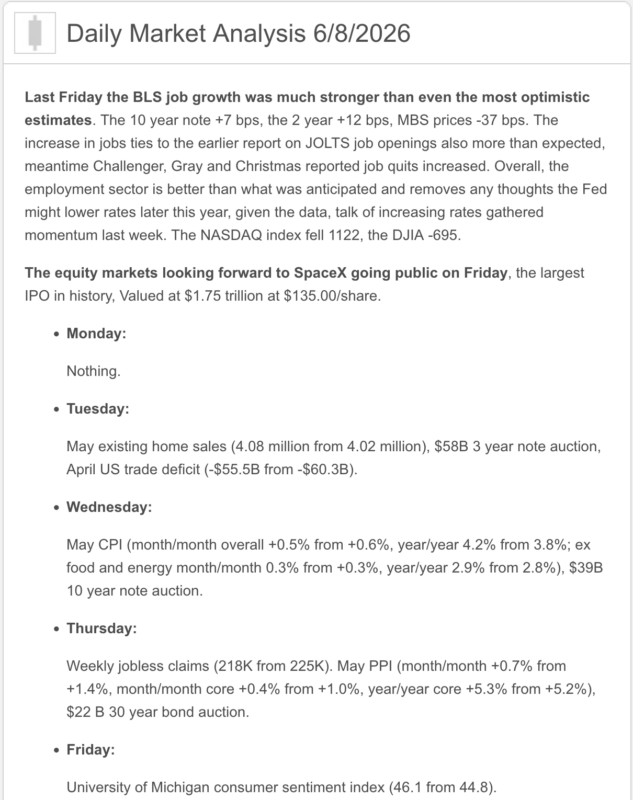

Good Monday Morning from your Hometown Lender. Let’s dive into Monday’s market analysis!

Friday saw bonds sell off early after jobs data came in much stronger than expected. Unfortunately though, rate sheets were the worst we have seen. Pricing today should rebound a bit, although it won’t be much. Talks with Iran continue to drag on, not helped by military strikes between Iran and Israel over the weekend.

Nothing today on the economic calendar, bonds will likely follow the headlines or drift on the day, meaning we likely won’t see any big moves either way and reprice risk is low on the day.

Market Analysis – From a higher and better view:

Market Analysis – Quick Snapshot

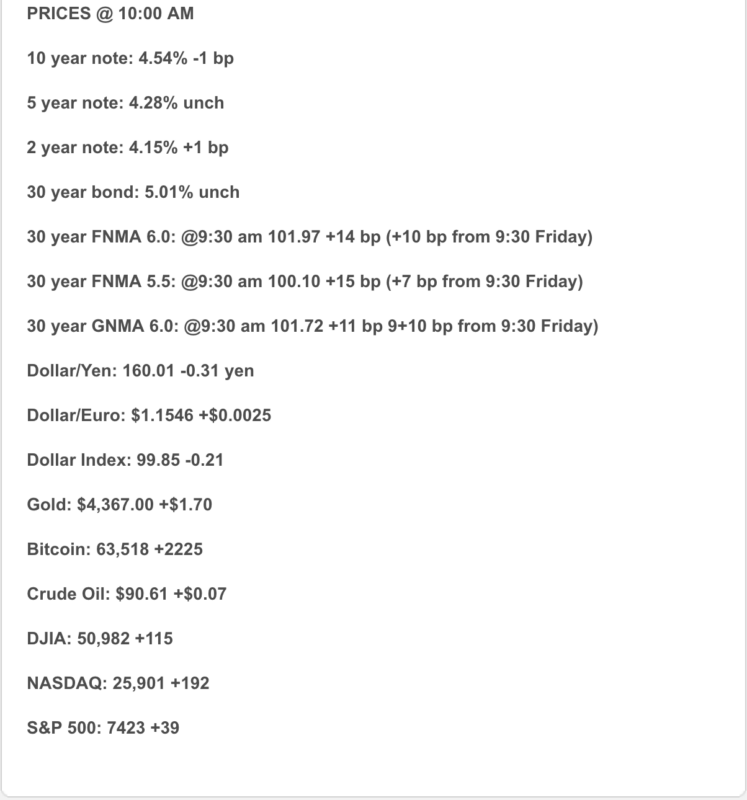

Bonds: The 10-year Treasury is back near the mid-4.5% range, with Barron’s reporting it hit roughly 4.57% this morning as markets reacted to stronger jobs data and renewed Middle East/oil risk. Translation: bonds wanted a quiet Monday and got handed a leaf blower.

Mortgage Rates: Daily tracking shows the 30-year fixed around 6.53% and the 15-year around 5.89% today. Freddie Mac’s latest weekly survey showed the 30-year at 6.48% as of June 4, so real-time pricing remains a little higher than the weekly average.

Fed Watch: Strong May jobs data is pushing rate-cut expectations further out. Goldman Sachs now expects no Fed rate cuts until 2027, citing stronger activity, job growth, tariffs, oil prices, and inflation pressure.

Oil / Geopolitics: Oil jumped early after renewed Israel-Iran tensions, then pared gains after Iran said it would halt attacks for now. Brent was still around the mid-$90s, keeping energy prices central to the inflation story.

Markets: Stocks are trying to recover from Friday’s sharp selloff, but the big theme remains the same: AI optimism is helping risk assets, while higher yields and Fed uncertainty are keeping investors jumpy. Citigroup raised its year-end S&P 500 target to 8,100, citing earnings strength and the AI investment cycle.

Market Analysis – What It Means

Today’s market is being pulled in two directions: growth still looks resilient, but inflation and geopolitical risk are not going away quietly. That combination keeps the Fed cautious and keeps mortgage rates in the mid-6% range.

The key message for buyers and agents is simple: this is not a “wait for the perfect rate” market. It is a structure-the-payment market.

Fed & Political Backdrop

The Fed is still under pressure, but the data is not giving it much room to cut. The strong jobs report gives the Fed cover to stay patient, and the political backdrop remains delicate as Chair Kevin Warsh faces pressure between calls for lower rates and policymakers worried about inflation staying too high.

In plain English: the Fed wants proof before it moves. Right now, jobs are strong, oil is elevated, and inflation risk is still hanging around like that last guest who will not leave the party.

Market Analysis – Housing & Mortgage Strategy

Mortgage rates are still workable, but not forgiving. The best conversations right now are not just about the rate; they are about the full payment strategy:

seller credits, temporary buydowns, permanent buydowns, ARM options where appropriate, and a realistic refinance path later.

Buyers are not gone. They are doing math. Sellers and builders who help solve the monthly payment problem have the best chance of turning interest into contracts.

Lock vs. Float

Lock bias: If closing within 30 days, the borrower is payment-sensitive, or the file is tight, locking is still the cleaner recommendation.

Float bias: Floating only makes sense with time, flexibility, and a clear trigger. With yields back near the mid-4.5% range and oil headlines moving fast, floating without a plan is not strategy

Stay safe and make today great!