Good Friday am from your Hometown Lender. Let’s get into Friday’s market analysis!

Pricing is worse this morning as bonds sell off on a stronger than expected jobs report. Reprice risk on the day is moderate, there’s always a chance that headlines about peace talks with Iran could cause some moves, and there is also some risk that this morning’s selling could snowball (but that’s not looking likely at the moment).

For now I suggest floating, especially loans that don’t close till later in the month or after. This morning’s reaction will subside and we will likely see some recovery next week, especially if we get some positive news out of the Middle East.

Market Analysis – From a higher and better view:

Market Analysis – Quick Snapshot

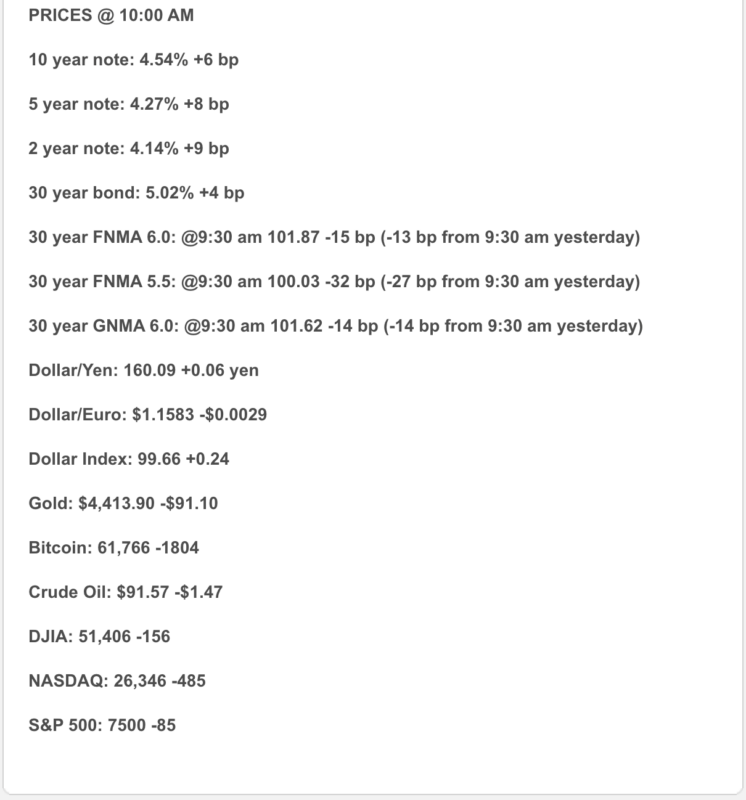

Bonds: The 10-year Treasury moved higher after this morning’s stronger-than-expected jobs report, rising near 4.54% as markets reduced expectations for Fed cuts and increased the odds of a possible hike later this year. Bonds were hoping for a soft labor number. Instead, they got a protein shake and a whistle.

Mortgage Rates: Freddie Mac’s latest weekly survey showed the 30-year fixed at 6.48% as of June 4, down from 6.53% the prior week. The 15-year fixed fell to 5.79%, down from 5.87%. Daily Bankrate tracking is closer to 6.52% for the 30-year fixed and 5.91% for the 15-year fixed, so real-time pricing remains sensitive.

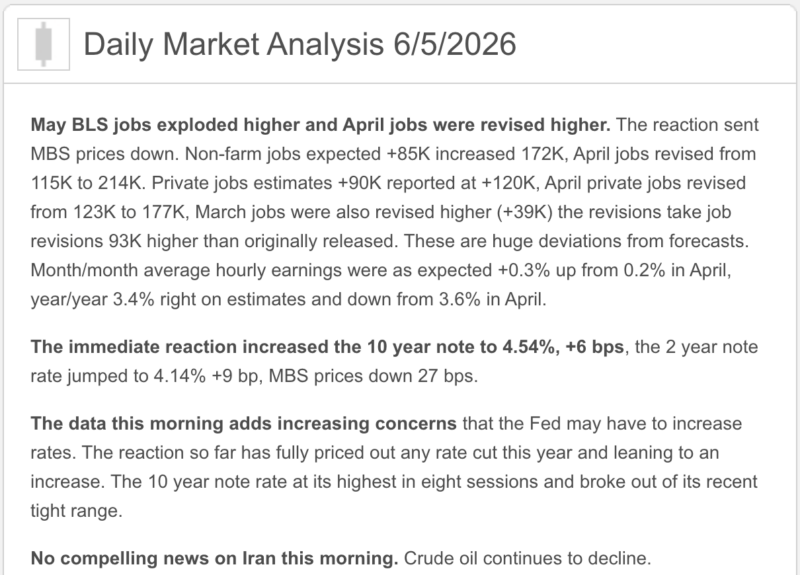

Jobs: May nonfarm payrolls increased by 172,000, well above expectations, while the unemployment rate held steady at 4.3%. Job gains were led by leisure and hospitality, local government, and health care, while financial activities declined.

Wages: Average hourly earnings rose 0.3% in May and 3.4% year over year, with the average hourly wage rising to $37.53. Wage growth is not exploding, but it is still firm enough to keep the Fed cautious.

Fed Watch: Markets are now pricing a higher chance of a Fed hike by December after the jobs report, while still expecting the Fed to hold its current 3.50%–3.75% range at the June meeting.

Oil / Geopolitics: Oil prices fell today after Oman said operations at Mina al Fahal were proceeding normally, easing earlier disruption fears. Brent traded near $94.19, and WTI near $91.91, but both benchmarks are still on track for weekly gains as Middle East risk remains elevated.

1) Market Analysis – What Hit This Morning

Today’s headline is simple: the labor market is stronger than expected.

The U.S. added 172,000 jobs in May, more than double some forecasts, and unemployment stayed at 4.3%. The report also included upward revisions to March and April, adding 93,000 more jobs than previously reported. That matters because the Fed has been waiting for either cooler inflation or softer labor before considering easier policy. Today’s report gave the Fed neither.

The market reaction was immediate: Treasury yields moved higher, the dollar firmed, and rate-cut hopes faded. Reuters reported the 2-year Treasury moved to about 4.15%, while the 10-year rose to roughly 4.54% after the report.

Narrative you can use:

The jobs market is not overheated, but it is still resilient. That is good news for the economy, but not great news for mortgage rates because it gives the Fed less reason to cut. In mortgage terms: buyers still have opportunities, but the payment still needs a game plan.

2) Fed Watch

The Fed’s current target range remains 3.50% to 3.75%, and the next policy decision is scheduled for June 17. In its last statement, the Fed said it would assess incoming data, the evolving outlook, and the balance of risks before adjusting policy.

Today’s jobs report makes a June cut highly unlikely and pushes the market closer to the conversation we have been watching all week: hold vs. hike risk, not hold vs. cut optimism. Reuters reported that rate futures now show a materially higher probability of a Fed hike by December after the strong payrolls number.

Kansas City Fed President Jeffrey Schmid added to that message, saying the Fed’s choice is between patience and potential rate hikes if inflation remains too high. That is not exactly music to a borrower’s ears, but it is the tune the bond market is hearing.

Bottom line:

The Fed wants proof that inflation is cooling or labor is weakening. Today’s jobs report did not provide that proof.

3) Market Analysis – Where Mortgage Rates Actually Are

Freddie Mac’s weekly survey improved slightly, with the 30-year fixed averaging 6.48% and the 15-year fixed averaging 5.79% as of June 4. That is a welcome move lower from the prior week, but Freddie’s survey reflects rates offered during the prior Thursday-through-Wednesday window, so it does not fully capture today’s post-jobs-report bond-market reaction.

Daily tracking is still closer to the low-to-mid 6.5% range, with Bankrate listing the 30-year fixed around 6.52% and the 15-year fixed around 5.91%. Today’s stronger jobs report could put upward pressure on daily repricing if Treasury yields remain elevated.

Practical read:

Rates are workable, but not forgiving. The right conversation is not simply:

“What is the rate?”

It is:

What is the payment? What credits are available? Is a buydown smart? Does an ARM make sense? What is the refinance path if the market improves?

That is where smart deals are getting built right now.

4) Market Analysis – Housing Market Check

Housing remains a payment-sensitive market. The latest mortgage-rate improvement helped sentiment a little, but today’s jobs report and higher Treasury yields are a reminder that rates can reprice quickly.

What this means:

Buyers still have more room to negotiate than they had during the frenzy years, but affordability remains the gatekeeper. Sellers and builders who help solve the monthly payment problem — through credits, buydowns, incentives, or realistic pricing — are more likely to convert interest into contracts.

This is not a dead market. It is a disciplined market. Buyers are not gone; they are doing math.

5) Political Backdrop & Fed Independence

The political and geopolitical backdrop is still directly tied to rates. Oil eased today after Oman calmed concerns about port disruptions, but the broader Middle East situation remains unsettled. Brent is still above $94, WTI is above $91, and both are on track for weekly gains. That keeps energy prices central to the inflation story.

Markets are also watching Fed independence and policy credibility closely. A strong jobs report makes it harder for the Fed to justify cuts, even with political pressure for lower rates. The Fed’s challenge is that inflation is still above target, labor is resilient, and energy prices remain volatile. That is a tricky policy stew — and nobody ordered extra spice.

Translation:

Mortgage rates are not just following housing data. They are following jobs, wages, inflation, oil, Treasury demand, Fed credibility, and global conflict. Apparently, today’s rate sheet needs a labor economist, an oil trader, and a decent cup of coffee.

6) Market Analysis – What This All Means for Rates Going Forward

| Scenario | What Needs to Happen | Likely Rate Impact |

| Best Case | Oil cools, inflation improves, labor softens gently, Fed rhetoric calms | Mortgage rates drift lower |

| Base Case | Labor stays resilient, inflation remains sticky, Fed stays patient | Rates remain choppy in the mid-to-upper 6s |

| Risk Case | Jobs stay strong, oil rises again, inflation expectations climb, Fed sounds hawkish | Rates push higher and reprice risk increases |

My read: base case remains choppy, not catastrophic. Today’s jobs report was good for economic resilience, but it was not friendly to rate-cut hopes. Bonds need softer inflation and less geopolitical pressure before mortgage rates can make a clean move lower.

7) Market Analysis – Practical Takeaways

For buyers:

Do not wait for the perfect rate. Perfect rates are like perfect inspection reports — beautiful, rare, and usually followed by fine print. Focus on payment, seller credits, buydowns, program fit, and long-term flexibility.

For homeowners:

Refinance decisions remain case-by-case. Cash-out, debt consolidation, HELOC alternatives, ARM reset planning, and future refinance strategy should all be reviewed individually.

For agents:

This is a payment strategy market. The strongest agents are not just saying, “rates are high.” They are showing buyers how credits, buydowns, price negotiation, and loan structure change the monthly payment.

8) Lock vs. Float

- Lock bias: If closing within 30 days, the borrower is payment-sensitive, or the file is tight on ratios, locking remains the cleaner recommendation.

- Float bias: Floating can make sense only with more time, stronger borrower flexibility, and a defined trigger. After today’s strong jobs report, floating blindly is not strategy — it is cardio with disclosures.

Today’s guidance:

Bias toward locking short-term closings. For longer timelines, cautious floating may be reasonable only if the borrower understands the risk and has a clear ceiling for pain.

Stay safe, make today great, and have a fantastic weekend!