Good Morning on this best day of the week Wednesday from your Hometown Lender! Let’s dig into today’s market analysis, shall we?

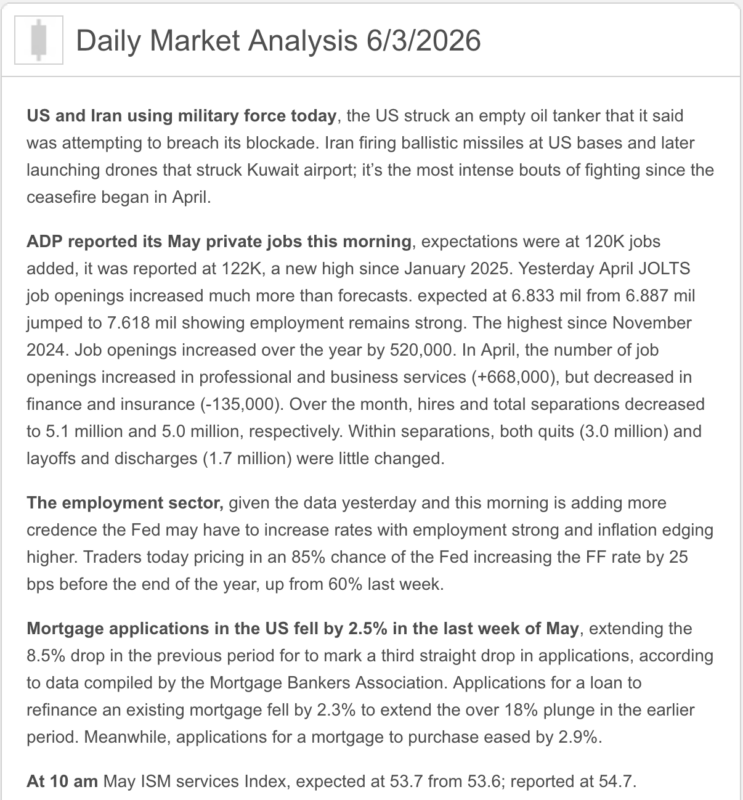

With no new headlines or action in the Middle East, yesterday was a calm day for bonds. Neither mortgage bonds nor the 10yr moved much through the day at all. Bonds off to a weak start this morning, first in overnight trading in foreign markets and then continued to lose ground here in domestic markets as oil prices rose on concerns on yet more military skirmishes with Iran despite the ceasefire. This one though is considered more serious and was one of the most intense bouts of fighting yet, with Kuwait and Bahrain caught in the crossfire and a drone attack closing a Kuwait airport. According to the media, it was started when the U.S. struck an empty oil tanker it said was trying to get through the blockade. Despite the military action though, U.S. Central Command said the ceasefire was still “ongoing.”

Market Analysis – From a higher and better view:

Market Analysis – Quick Snapshot

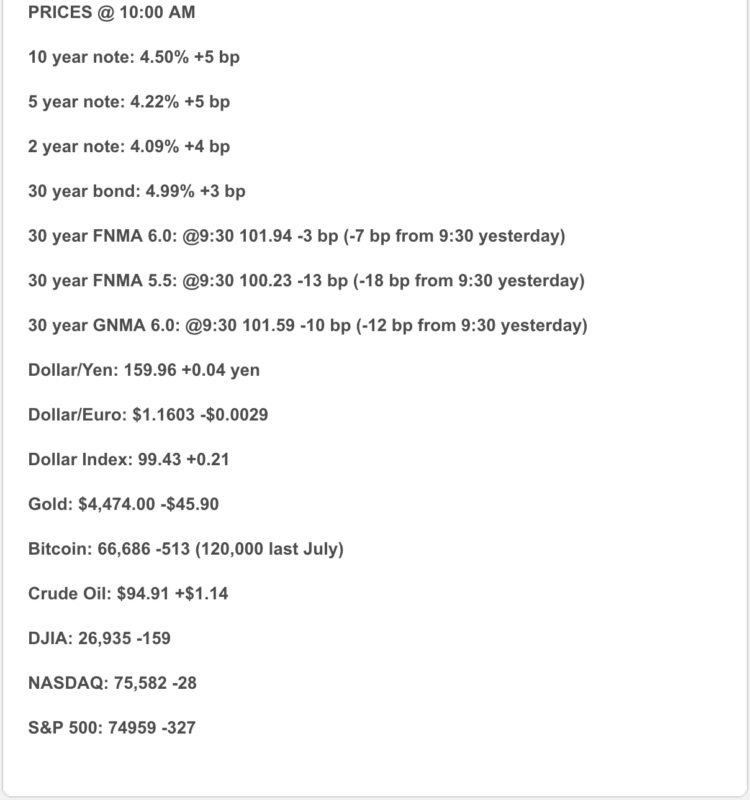

Bonds: The 10-year Treasury is back near 4.49%–4.50%, moving higher after stronger ADP labor data and renewed Middle East/oil concerns. Translation: bonds wanted a quiet Wednesday and got handed a triple espresso.

Mortgage Rates: Daily Bankrate/WSJ tracking shows the 30-year fixed around 6.52% and the 15-year fixed around 5.91% today. Freddie Mac’s latest weekly survey, released May 28, showed the 30-year fixed at 6.53% and the 15-year fixed at 5.87%.

Labor: ADP reported private employers added 122,000 jobs in May, above expectations and up from a revised 105,000 in April. Labor is not roaring, but it is still firm enough to keep the Fed cautious.

Services: ISM Services improved to 54.5 in May from 53.6, with new orders rising and input prices still elevated. Growth is holding up, but price pressure remains the problem child.

Oil / Geopolitics: Brent crude rose to about $97.41 and WTI to about $95.15 as Middle East hostilities flared and U.S.–Iran talks stalled. Higher oil keeps inflation pressure alive, and inflation pressure keeps mortgage rates from getting comfortable.

1) Market Analysis – What Hit This Morning

Today’s market theme is stronger labor, stronger services, higher oil, and a Fed that still does not have permission to cut.

ADP showed 122,000 private-sector jobs added in May, beating expectations, while ISM Services rose to 54.5, showing the service side of the economy continues to expand. That is good news for recession fears, but not great news for rate-cut hopes because resilient growth gives inflation more room to stick around.

The bigger headache is still energy. Oil moved higher as Middle East tensions escalated and negotiations stalled, which keeps markets worried about inflation feeding through transportation, goods, and consumer prices.

Narrative you can use:

The economy is still showing resilience, but inflation risk is not going away quietly. That keeps Treasury yields elevated, keeps the Fed cautious, and keeps mortgage rates choppy. In mortgage terms: buyers should not panic — but the payment still needs a plan.

2) Fed Watch

The Fed’s current target range remains 3.50% to 3.75%, and the April FOMC statement said the Committee will assess incoming data, the evolving outlook, and the balance of risks before making additional policy moves.

Fed officials are still emphasizing caution. Vice Chair Jefferson recently said policy is “well positioned” amid inflation risks, while other officials have warned that a prolonged energy shock could shift the policy outlook.

Bottom line:

The Fed is still in “show me” mode. Stronger jobs data, firmer services, and higher oil do not create a clean path to cuts. The market is still debating hold vs. hike risk, not celebrating lower rates.

3) Market Analysis – Where Mortgage Rates Actually Are

Freddie Mac’s latest weekly survey showed the 30-year fixed at 6.53% and the 15-year fixed at 5.87% as of May 28. Daily pricing is slightly better today, with Bankrate/WSJ showing the 30-year fixed around 6.52% and the 15-year fixed around 5.91%.

Practical read:

Rates are workable, but not forgiving. The right conversation is not simply, “What is the rate?” It is:

What is the payment? What credits are available? Is a buydown smart? Does an ARM make sense? What is the refinance path if the market improves?

That is where smart deals are getting built right now.

4) Market Analysis – Housing Market Check

The housing story remains simple: demand exists, but affordability is the gatekeeper. With rates still in the mid-6s and inflation keeping pressure on household budgets, buyers are more selective and payment-sensitive.

What this means:

Sellers and builders who help solve the monthly payment problem — through credits, buydowns, incentives, or realistic pricing — are more likely to convert interest into contracts. Buyers have opportunity, but they need structure.

5) Political Backdrop & Fed Independence

The political and geopolitical backdrop is still a direct rate driver. Middle East hostilities pushed oil higher today, and the OECD warned that a prolonged Iran conflict could materially weaken global growth while keeping energy and input costs elevated.

That puts the Fed in a tough spot: growth risks are real, but inflation risks are also real. If the Fed cuts too early and inflation expectations rise, long-term rates could stay stubbornly high anyway. If the Fed stays too tight, growth and housing feel the pain. Fun little policy pretzel.

Translation:

Mortgage rates are not just following housing data. They are following oil, inflation, labor, Treasury demand, Fed credibility, global conflict, and consumer resilience.

6) Market Analysis – What This All Means for Rates Going Forward

| Scenario | What Needs to Happen | Likely Rate Impact |

| Best Case | Oil cools, Friday jobs data softens gently, inflation expectations settle | Mortgage rates drift lower |

| Base Case | Labor stays stable, services expand, oil remains volatile | Rates stay choppy in the mid-to-upper 6s |

| Risk Case | Oil spikes, inflation expectations rise, Fed officials sound more hawkish | Rates push higher and reprice risk increases |

My read: base case remains choppy, not catastrophic. Today’s data does not scream recession, but it also does not give the Fed a clean reason to cut. Bonds need softer inflation and less oil pressure before mortgage rates can build a real downward trend.

7) Market Analysis – Practical Takeaways

For buyers:

Do not wait for the perfect rate. Perfect rates are like perfect inspection reports — beautiful, rare, and usually followed by fine print. Focus on payment, seller credits, buydowns, program fit, and long-term flexibility.

For homeowners:

Refinance decisions remain case-by-case. Cash-out, debt consolidation, HELOC alternatives, ARM reset planning, and future refinance strategy should all be reviewed individually.

For agents:

This is a payment strategy market. The strongest agents are not just saying, “rates are high.” They are showing buyers how credits, buydowns, price negotiation, and loan structure change the monthly payment.

8) Lock vs Float

- Lock bias: If closing within 30 days, the borrower is payment-sensitive, or the file is tight on ratios, locking remains the cleaner recommendation.

- Float bias: Floating can make sense only with more time, stronger borrower flexibility, and a defined trigger. With Friday’s jobs report ahead and oil headlines moving bonds, floating blindly is not strategy — it is cardio with disclosures.

Today’s guidance:

Bias toward locking short-term closings. For longer timelines, cautious floating may be reasonable only if the borrower understands the risk and has a clear ceiling for pain.

Stay safe and make today great!