Good Tuesday AM from your Hometown Lender. Let’s get into today’s market analysis!

Yesterday saw bonds start the day basically flat, then around 9am ET started selling off hard as news broke that Iran was pulling out of negotiations and vowed to completely block the Strait of Hormuz because of continued fighting between Israel and Hezbollah in Lebanon.

After bottoming out, bonds started to recover late morning when oil prices started to fall. Markets seemed to ease up after President Trump posted on Truth Social, “Talks are continuing, at a rapid pace, with the Islamic Republic of Iran.” He also said he “had a very productive call” with Israeli Prime Minister Netanyahu about ceasing attacks on Lebanon and Hezbollah. Bonds continued to rebound through the afternoon.

Rates today will be better than yesterday morning. Although we are at risk of seeing some pricing volatility, rates are pretty stable and shouldn’t move much today.

Market Analysis – From a higher and better view:

Market Analysis –Quick Snapshot

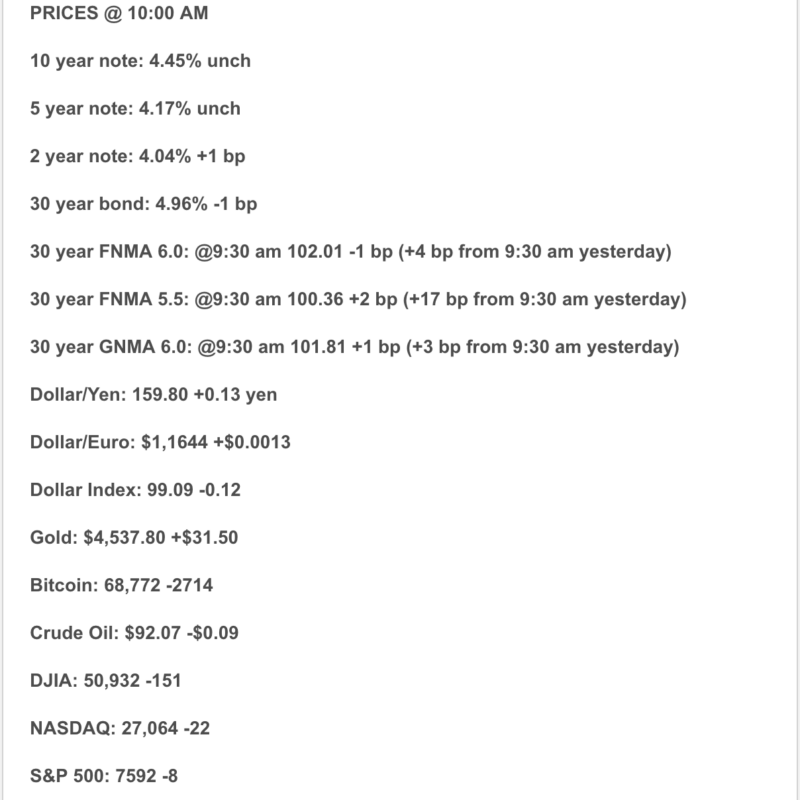

Bonds: The 10-year Treasury is hovering around the mid-4.4% range, with intraday reports showing it near 4.43%–4.45% as markets balance softer oil headlines, Middle East uncertainty, and hawkish Fed commentary. In other words, bonds are trying to relax, but they are still checking the exits.

Mortgage Rates: Daily Bankrate/WSJ tracking shows the 30-year fixed around 6.54% and the 15-year fixed around 5.90% today. Freddie Mac’s latest weekly survey, released May 28, showed the 30-year fixed at 6.53% and the 15-year fixed at 5.87%.

Labor: April JOLTS job openings jumped by 731,000 to 7.618 million, the highest level since May 2024. The catch: hiring fell by 419,000 to 5.116 million, so employers are posting jobs, but they are still moving cautiously.

Inflation: April PCE inflation remains the core problem: headline PCE was 3.8% year over year, core PCE was 3.3%, and the personal saving rate fell to 2.6%. That is not exactly a “Fed, please cut now” starter kit.

Housing: Pending home sales rose 1.4% in April and were up 3.2% year over year, while existing-home sales came in at 4.02 million, with a median price around $417,800 and 4.4 months of inventory. Demand is still there — it is just very payment-sensitive.

1) Market Analysis -What Hit This Morning

Today’s big economic release was the JOLTS report, and it gave the market a mixed but important message. Job openings surged to 7.618 million, well above expectations, which suggests labor demand is not falling apart. But hiring declined to 5.116 million, which means employers may be interested in workers, but still hesitant to actually pull the trigger. It is the labor market version of browsing Zillow at midnight — lots of interest, not always a contract.

Markets are also still watching oil and the Middle East. Reuters reported Brent crude around $95.15 and WTI around $92.21 as investors digest conflicting signals over U.S.–Iran talks and the possible reopening of the Strait of Hormuz. Energy prices remain central to the inflation story, which means they remain central to the mortgage-rate story.

Narrative you can use:

Today’s data says the labor market is resilient, but not roaring. Inflation is still too high, oil remains volatile, and the Fed does not yet have a clean reason to cut. That keeps mortgage rates choppy and keeps financing strategy more important than headline rate shopping.

2) Fed Watch

The Fed’s current target range remains 3.50% to 3.75%, and the April FOMC statement said the Committee will continue assessing incoming data, the evolving outlook, and the balance of risks.

Cleveland Fed President Beth Hammack added a hawkish note today, saying rates may need to rise if inflation pressures do not abate. Her comments helped push Treasury yields higher intraday and reinforced that the Fed discussion has shifted closer to hold vs. hike, not hold vs. cut.

Bottom line:

The Fed is still in “prove it” mode. Stronger job openings plus sticky inflation do not make rate cuts easier. Buyers may want lower rates, agents may want lower rates, lenders may want lower rates — but the Fed wants evidence. Very rude of them, but consistent.

3) Market Analysis -Where Mortgage Rates Actually Are

Freddie Mac’s latest weekly PMMS showed the 30-year fixed at 6.53%, up slightly from 6.51% the prior week. The 15-year fixed averaged 5.87%, up from 5.85%. Freddie Mac’s survey is released weekly and reflects an average of offered rates from the prior Thursday through Wednesday, so daily pricing can move faster.

Daily market tracking from Bankrate/WSJ shows the 30-year fixed around 6.54% today and the 15-year fixed around 5.90%, slightly lower than recent late-May highs but still elevated.

Practical read:

Rates are workable, but not forgiving. The right conversation is not just:

“What is the rate?”

It is:

What is the payment? What credits are available? Is a buydown smart? Does an ARM make sense? What is the refinance path if the market improves?

That is where deals are getting built right now.

4) Market Analysis -Housing Market Check

Housing remains mixed but far from dead. April pending home sales rose 1.4% month over month and 3.2% year over year, showing that buyer demand still exists when price, inventory, and payment line up.

Existing-home sales were running at 4.02 million in April, with a median sales price of about $417,800 and 4.4 months of inventory. More inventory helps buyers breathe, but higher rates continue to make payment the real gatekeeper.

What this means:

This is a market where buyers can find opportunity, but they need structure. Sellers and builders who help solve the payment problem — through credits, buydowns, incentives, or realistic pricing — are more likely to convert showings into contracts.

5) Political Backdrop & Fed Independence

The political and geopolitical backdrop remains a major rate driver. Reuters reported that oil prices remain around the mid-$90s as the market waits for clarity on U.S.–Iran negotiations, with the Strait of Hormuz still central because of its importance to global oil and LNG flows.

Markets are also reacting to Fed credibility and policy messaging. Hammack’s comments that policy may need to tighten if inflation does not cool are important because they show the Fed is still worried about inflation becoming more persistent. That matters for mortgage rates because long-term yields respond not just to today’s inflation, but to whether investors believe the Fed will control it.

Translation:

Mortgage rates are not just following housing data. They are following inflation, oil, labor, Fed credibility, Treasury demand, and geopolitical risk. Apparently, today’s rate sheet needs a passport and a caffeine budget.

6) Market Analysis -What This All Means for Rates Going Forward

| Scenario | What Needs to Happen | Likely Rate Impact |

| Best Case | Oil prices ease, PCE cools, Friday’s jobs report softens gently, Fed rhetoric calms | Mortgage rates drift lower |

| Base Case | Inflation stays sticky, labor remains stable, Fed stays cautious | Rates remain choppy in the mid-to-upper 6s |

| Risk Case | Oil spikes again, inflation expectations rise, labor stays firm, Fed turns more hawkish | Rates push higher and reprice risk increases |

My read: base case remains choppy, not catastrophic. The bond market is getting occasional relief, but sticky inflation and firm labor data are preventing a clean rate rally.

7) Market Analysis -Practical Takeaways

For buyers:

Do not wait for the perfect rate. Perfect rates are like perfect inspection reports — beautiful, rare, and usually followed by fine print. Focus on payment, seller credits, buydowns, program fit, and long-term flexibility.

For homeowners:

Refinance decisions remain case-by-case. Cash-out, debt consolidation, HELOC alternatives, ARM reset planning, and future refinance strategy should all be reviewed individually.

For agents:

This is a payment strategy market. The strongest agents are not just saying, “rates are high.” They are showing buyers how credits, buydowns, price negotiation, and loan structure change the monthly payment.

8) Lock vs Float

- Lock bias: If closing within 30 days, the borrower is payment-sensitive, or the file is tight on ratios, locking remains the cleaner recommendation.

- Float bias: Floating can make sense only with more time, stronger borrower flexibility, and a defined trigger. With Friday’s jobs report ahead and Fed speakers still leaning cautious, floating blindly is not strategy — it is cardio with disclosures.

Today’s guidance:

Bias toward locking short-term closings. For longer timelines, cautious floating may be reasonable only if the borrower understands the risk and has a clear ceiling for pain.

Stay safe and make today great!