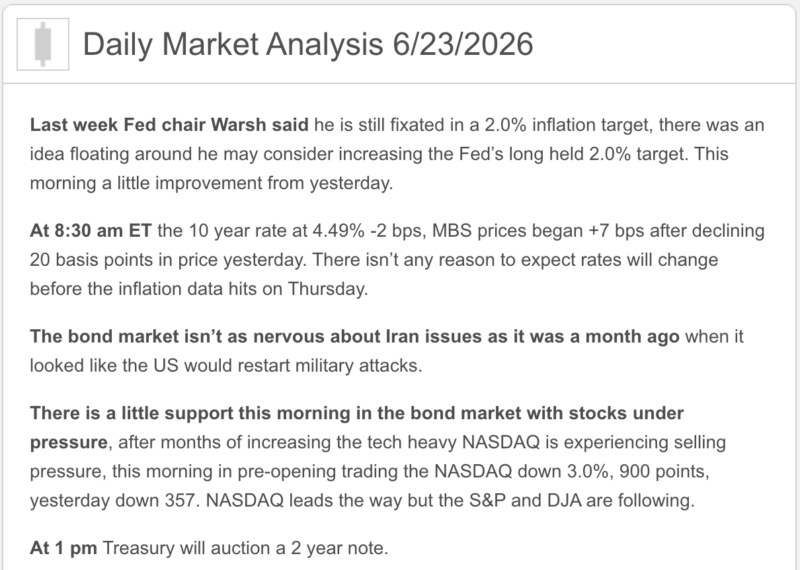

Good Tuesday am from your Hometown Lender. Let’s get into today’s market analysis!

Bonds started the day/week down quite a bit, giving back Thursday’s gains. From that point on though, bonds were basically unchanged through the day, ending about the same as when pricing came out.

Rate outlook for today…

Rate sheets today will be similar to a smidge better for some, and reprice risk on the day is low. There is a 2yr Treasury auction this afternoon, but don’t expect that to have any effect on bonds. Likely to see another calm day, reinforcing the idea that this is where rates will hang out for awhile.

Market Analysis – From a higher and better view:

Market Analysis – Quick Snapshot

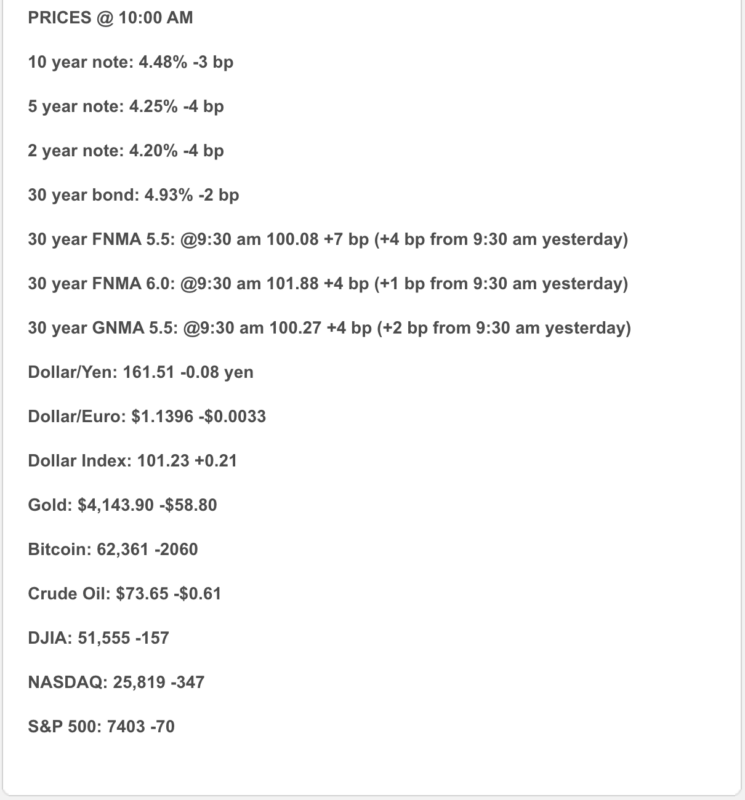

- Bonds: The 10-year Treasury is around 4.49%, slightly lower as oil prices ease and U.S.–Iran talks continue. Bonds got a little relief — not a spa day, but at least they found a parking spot.

- Mortgage Rates: Daily tracking shows the 30-year fixed around 6.61% and the 15-year fixed around 6.00%. Freddie Mac’s latest weekly survey showed the 30-year fixed at 6.47% and the 15-year fixed at 5.81%.

- Fed Watch: Fed hike expectations remain elevated after last week’s hawkish Fed meeting. Markets are now watching Thursday’s PCE inflation report for the next major clue.

- Economy: June business activity is still expanding, with manufacturing improving, but factory employment weakened. Translation: companies are still producing, but they are being cautious with hiring.

- Oil / Politics: Oil prices remain below recent highs as U.S.–Iran peace talks progress and temporary sanctions relief allows some Iranian oil sales. Lower oil helps inflation pressure, but the market is not declaring victory yet.

- Housing: May existing-home sales rose to a 4.17 million annualized pace. Inventory improved, but affordability remains the gatekeeper as mortgage rates stay elevated.

Market Analysis – What It Means

Today’s tone is mixed. Lower oil and slightly lower Treasury yields are helpful, but mortgage rates remain elevated because inflation and Fed hike risk are still very much alive.

In plain English: the market got a little breathing room, but buyers still need a payment strategy.

Market Analysis – Housing & Mortgage Strategy

This remains a structure-the-payment market.

The best conversations right now are about:

Seller credits, temporary buydowns, permanent buydowns, builder incentives, ARM options where appropriate, and a realistic refinance plan if rates improve later.

Buyers are still active, but they are doing math. Sellers and builders who help solve the monthly payment problem have the best chance of turning interest into contracts.

Lock vs. Float

Lock bias: If closing within 30 days, the borrower is payment-sensitive, or the file is tight, locking remains the cleaner recommendation.

Float bias: Lower oil is helpful, but Fed hike risk and Thursday’s PCE report keep repricing risk alive.

Today’s guidance:

Bias toward locking short-term closings. For longer timelines, cautious floating may be reasonable only with a clear risk ceiling and daily monitoring.

Stay safe and make today great!