Good morning on this fantastic Monday from your Hometown Lender. Let’s get right into today’s market analysis!

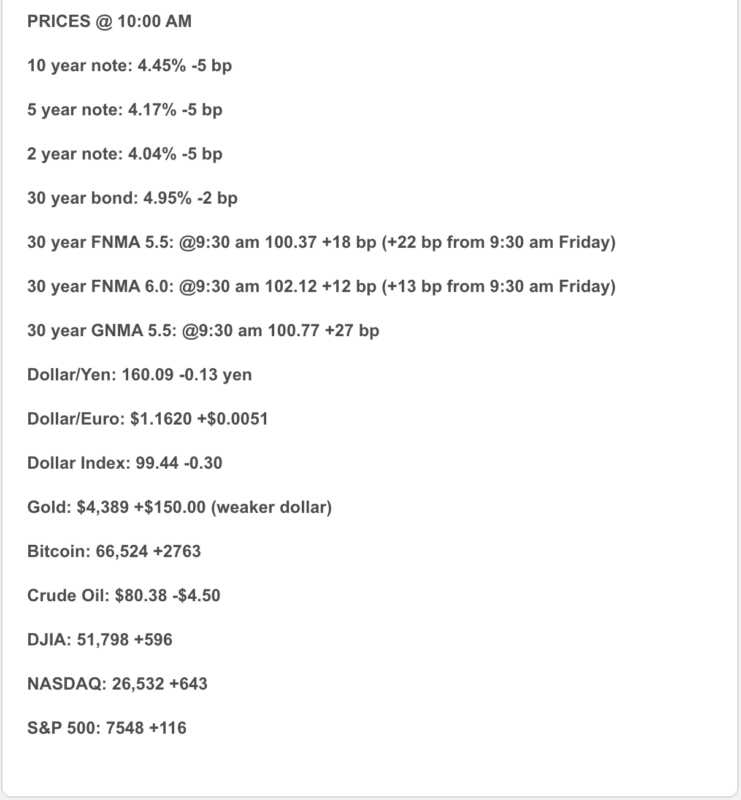

Looking back to Thursday, after a strong start that helped recover some of Wednesday’s losses after the Fed meeting, bonds drifted lower through the late afternoon on low trading volume. The bond market was closed on Friday in observance of Juneteenth. Rate sheets today will continue to slip, as bonds give back all of Thursday’s recovery, despite headlines about how peace talks with Iran continue. The Strait of Hormuz is open to traffic again, but it is projected that it could take months to see a return to the same volume of ships it was at before the conflict with Iran began. Oil prices are starting to level off after falling last week, but bond don’t care much and that means rate sheets don’t either. Instead, bonds are reacting to concerns that inflation could continue to be a problem, and Fed rate hike(s) coming to help fight it. Markets now pricing in the chance of a hike as soon as the next Fed meeting in July, currently about a 30% possibility.

There is a decoupling between oil and bonds for the moment. We will see how markets react over the next few days but clearly the hawkish statement from Chairman Warsh last week has changed the narrative back to a more normal trading strategy. Time to start watching inflation as a drive as well as oil (despite that oil is/will be the catalyst for the direction of inflation).

Market Analysis – From a higher and better view:

Bonds: The 10-year Treasury is back around the mid-4.5% range, as markets weigh lower oil prices against a more hawkish Fed. Bonds got oil relief, but the Fed is still holding the whistle.

Mortgage Rates: Daily tracking shows the 30-year fixed around 6.53% and the 15-year fixed around 5.90%. Freddie Mac’s latest weekly survey showed the 30-year fixed at 6.47% and the 15-year fixed at 5.81%.

Fed Watch: The Fed held rates steady last week, but the tone shifted more hawkish. Several major banks now expect rate hikes later this year, with Bank of America calling for three hikes and Deutsche Bank expecting two.

Oil / Politics: Oil fell as U.S.–Iran peace talks progressed and the U.S. issued a temporary 60-day license allowing certain Iranian oil sales. Lower oil helps the inflation story, but the market is not declaring victory yet.

Housing: May existing-home sales rose to a 4.17 million annualized pace, with a median price of $429,300 and 4.5 months of inventory. More inventory helps, but affordability is still the gatekeeper.

Market Analysis – What It Means

Today’s tone is mixed. Lower oil is helpful for inflation and bonds, but the Fed’s hawkish shift keeps pressure on rates. Markets are now watching Thursday’s PCE inflation report for the next major clue.

In plain English: the market got a little relief, but buyers still need a payment strategy.

Market Analysis – Housing & Mortgage Strategy

This remains a structure-the-payment market.

The best conversations right now are about:

Seller credits, temporary buydowns, permanent buydowns, builder incentives, ARM options where appropriate, and a realistic refinance plan if rates improve later.

Buyers are still active, but they are doing math. Sellers and builders who help solve the monthly payment problem have the best chance of turning interest into contracts.

Lock vs. Float

- Lock bias: If closing within 30 days, the borrower is payment-sensitive, or the file is tight, locking remains the cleaner recommendation.

- Float bias: Lower oil is helpful, but Fed hike risk and Thursday’s PCE report keep repricing risk alive.

Today’s guidance:

Oil prices eased and U.S.–Iran talks improved, but mortgage rates remain in the mid-6s as markets focus on Fed hike risk and Thursday’s PCE inflation report. Buyers should not panic — they should plan. In this market, structure matters. toward locking short-term closings. For longer timelines, cautious floating may be reasonable only with a clear risk ceiling and daily monitoring.

Stay safe and make today great!