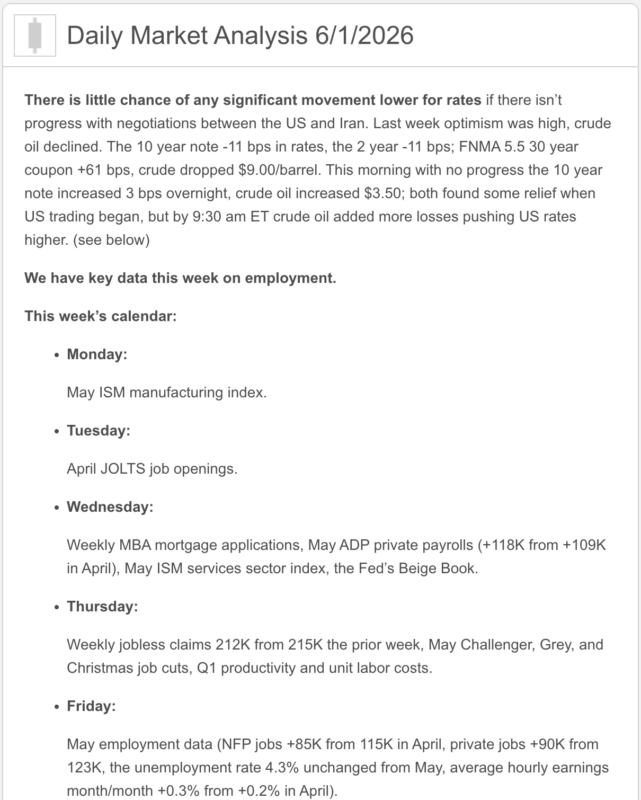

Good Monday am from your Hometown Lender. Let’s dive into today’s market analysis!

Friday saw bonds improve a bit on the day. There was a bit of a head fake that a deal with Iran was done when news broke that President Trump had called a Situation Room meeting and had promised a “final determination”, but after two hours the meeting broke without any announcements. Bonds seemed to be waiting for the real news, so we didn’t see a big rally that fell apart. Today, rates are worse than Friday after bonds sold off hard on headlines that Iran was pulling out of negotiations and vowed to ‘completely’ block the Strait of Hormuz.

Market Analysis – From a higher and better view;

Market Analysis – Quick Snapshot

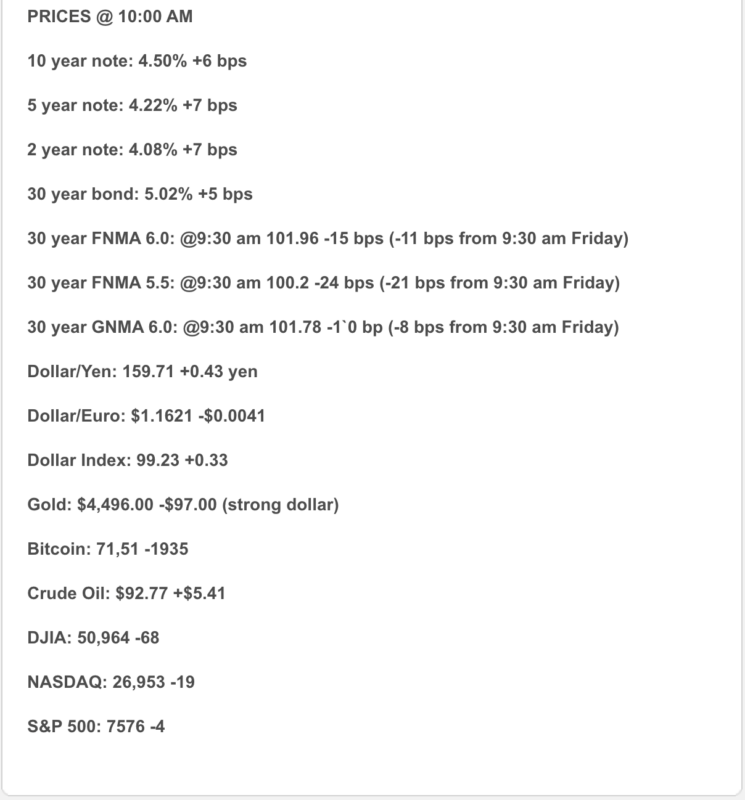

Bonds: The 10-year Treasury is back around the mid-4.4% to low-4.5% range, with fresh pressure from rising oil prices and renewed uncertainty around Middle East peace talks. Translation: bonds got the weekend memo and did not love it.

Mortgage Rates: Freddie Mac’s latest weekly survey showed the 30-year fixed at 6.53% and the 15-year fixed at 5.87% as of May 28. Daily tracking from WSJ/Bankrate showed the 30-year fixed around 6.56% today.

Manufacturing: ISM Manufacturing jumped to 54.0 in May, the strongest reading since May 2022 and the fifth straight month of expansion. Good for growth, but not great for rate-cut hopes because stronger activity can keep inflation pressure alive.

Construction: April construction spending rose 0.4%, better than expectations, with residential construction up 0.8% and new single-family construction up 1.4%.

Inflation: April PCE inflation rose 3.8% year over year, while core PCE rose 3.3%. That is still too hot for the Fed to get comfortable cutting.

Housing: Pending home sales rose 1.4% in April and were up 3.2% year over year, while existing-home sales came in at 4.02 million, with 4.4 months of inventory.

1) Market Analysis – What Hit This Morning

Today’s market theme is stronger manufacturing, sticky inflation, and fragile geopolitics.

The ISM Manufacturing Index rose to 54.0, beating expectations and reaching the highest level in four years. That is a clear sign the industrial side of the economy is still moving. The catch: part of the strength appears tied to businesses front-loading orders because of supply-chain disruptions and rising prices tied to the Iran conflict.

Construction spending also beat expectations, rising 0.4% in April. Residential spending rose 0.8%, and new single-family spending rose 1.4%, even as higher mortgage rates continue to weigh on housing demand.

Narrative you can use:

The economy is showing pockets of strength, but inflation is still sticky and geopolitical risk is still pushing oil and bond yields around. That keeps the Fed cautious and keeps mortgage rates volatile. In mortgage terms: opportunity exists, but the payment still needs a seatbelt.

2) Fed Watch

The Fed remains stuck between two uncomfortable facts: inflation is still too high, but parts of the economy are showing strain. Markets are increasingly focused on whether the Fed stays on hold or eventually has to consider another hike if energy-driven inflation persists. Reuters noted that markets are watching Friday’s jobs report closely, with economists expecting 85,000 jobs added and unemployment holding at 4.3%.

The Fed’s preferred inflation gauge, PCE, is still running well above target at 3.8%, with core PCE at 3.3%. That is not the setup that typically produces quick rate cuts.

Bottom line:

The Fed is still in “show me” mode. It needs cooler inflation, softer labor, or both. Right now, the data is not giving the Fed enough cover to ride in on a rate-cut horse wearing a cape.

3) Market Analysis – Where Mortgage Rates Actually Are

Freddie Mac’s latest PMMS showed the 30-year fixed at 6.53%, up from 6.51% the prior week, and the 15-year fixed at 5.87%, up from 5.85%. Freddie also notes that its weekly survey reflects rates offered during the prior Thursday-through-Wednesday period, so daily pricing can move faster than the survey.

Daily WSJ/Bankrate tracking showed the national average 30-year fixed around 6.56% today and the 15-year fixed around 5.92%.

Practical read:

Rates are workable, but not forgiving. This is not a market where “just find me the lowest rate” is the whole strategy. The real conversation is:

What is the payment? What credits are available? Is a buydown smart? Does an ARM make sense? Is there a realistic refinance path later?

That is where smart deals are getting built.

4) Market Analysis – Housing Market Check

Housing is giving us a mixed but useful message. Pending home sales rose 1.4% in April and were 3.2% higher year over year, which tells us demand still exists when inventory, price, and payment line up.

Existing-home sales were running at 4.02 million, with a median price around $417,800 and 4.4 months of inventory. That is more balanced than the frenzy years, but still not a fire-sale market.

Construction data added another layer today: residential construction spending rose 0.8%, and new single-family spending rose 1.4%, but Reuters noted higher mortgage rates, tariffs, land costs, and labor shortages are still creating headwinds for builders.

What this means:

Buyers have more options, but affordability is still the gatekeeper. Sellers and builders who help solve the payment problem — through credits, buydowns, incentives, or price strategy — have the best chance of turning traffic into contracts.

5) Market Analysis – Political Backdrop & Fed Independence

The political and geopolitical backdrop remains a major rate driver. Reuters reported that the dollar rose as markets evaluated fragile Middle East peace talks after the U.S. and Iran traded blows over the weekend, with the Strait of Hormuz closure continuing to worsen the inflation outlook.

AP also highlighted the bond market’s warning around U.S. debt, deficits, inflation, and affordability. The 10-year Treasury yield has risen from around 3.95% before the Iran conflict began to above 4.44%, with higher borrowing costs worsening pressure on housing, autos, and consumer finance.

Translation:

Mortgage rates are not just following housing data. They are following oil, inflation, war risk, Treasury supply, Fed credibility, budget deficits, and consumer resilience. Apparently, today’s rate sheet needs a passport, a political science minor, and maybe a helmet.

6) What This All Means for Rates Going Forward

| Scenario | What Needs to Happen | Likely Rate Impact |

| Best Case | Oil prices cool, PCE improves, labor softens gently, Fed rhetoric calms | Mortgage rates drift lower |

| Base Case | Inflation stays sticky, manufacturing holds up, Fed stays cautious | Rates remain choppy in the mid-to-upper 6s |

| Risk Case | Oil spikes again, inflation expectations rise, jobs stay firm, Fed sounds hawkish | Rates push higher and reprice risk increases |

My read: base case remains choppy, not catastrophic. Today’s stronger manufacturing data is good for economic confidence but not necessarily good for mortgage rates. Bonds need softer inflation and less geopolitical pressure before mortgage pricing can make a more meaningful move lower.

7) Market Analysis – Practical Takeaways

For buyers:

Do not wait for the perfect rate. Perfect rates are like perfect inspection reports — beautiful, rare, and usually followed by fine print. Focus on payment, credits, buydowns, program fit, and long-term flexibility.

For homeowners:

Refinance decisions remain case-by-case. Cash-out, debt consolidation, HELOC alternatives, ARM reset planning, and future refinance strategy should be reviewed individually.

For agents:

This is a payment strategy market. The strongest agents are not just saying, “rates are high.” They are showing buyers how credits, buydowns, price negotiation, and loan structure change the monthly payment.

8) Lock vs Float

- Lock bias: If closing within 30 days, the borrower is payment-sensitive, or the file is tight on ratios, locking remains the cleaner recommendation.

- Float bias: Floating can make sense only with more time, stronger borrower flexibility, and a defined trigger. With Friday’s jobs report ahead and geopolitical headlines still moving bonds, floating blindly is not strategy — it is cardio with disclosures.

Today’s guidance:

Bias toward locking short-term closings. For longer timelines, cautious floating may be reasonable only if the borrower understands the risk and has a clear ceiling for pain.

Stay safe and make today great!!!