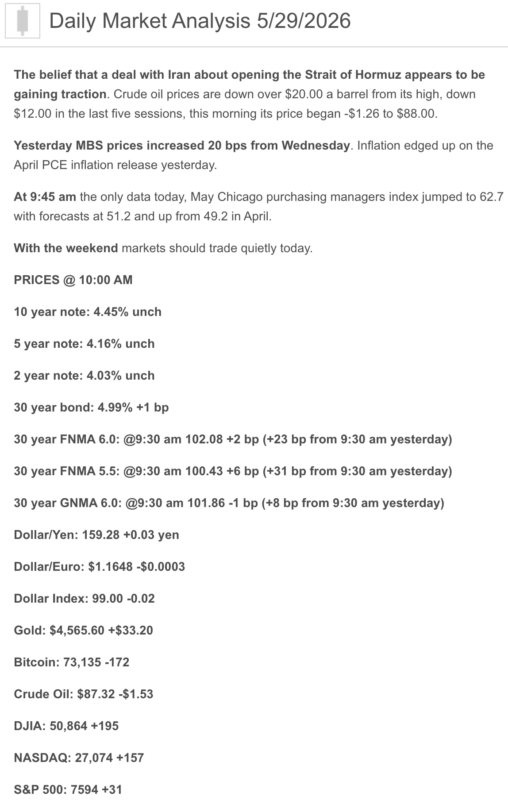

Good Friday morning from your Hometown Lender… let’s get today’s market analysis going!

Yesterday saw mortgage bonds start the day losing a bit of ground, but rallied to improve through the day after news was leaked that the US and Iran had reached a preliminary deal to extend the ceasefire by 60 days, and more importantly to open up the Strait of Hormuz and remove all mines within 30 days. One important point was the the deal was not yet approved by President Trump, although markets didn’t seem too worried about that just yet.

Rates today are better than yesterday morning. There is no economic data on the calendar for the day, and although Fed members are out speaking that won’t affect bonds at all today. We could see bonds improve if news breaks that Trump has signed off on the deal, but it would have to be a significant rally for bonds for most lenders to reprice better on a Friday.

Market Analysis – From a higher and better view:

Bonds: The 10-year Treasury is near 4.45%, roughly flat from late Thursday, as markets balance lower oil prices and U.S.–Iran ceasefire hopes against still-hot inflation. Translation: bonds got a little oxygen, but they are not exactly running wind sprints yet.

Mortgage Rates: Freddie Mac’s latest weekly survey shows the 30-year fixed at 6.53% and the 15-year fixed at 5.87% as of May 28. That is up slightly from 6.51% and 5.85% the prior week.

Inflation: April PCE inflation — the Fed’s preferred gauge — rose 3.8% year over year, with core PCE up 3.3%. The monthly PCE increase was 0.4%, and core rose 0.2%. Inflation is still too warm for the Fed to comfortably pivot lower.

Growth: Q1 GDP was revised down to a 1.6% annualized pace, from the prior 2.0% estimate. Slower growth plus sticky inflation is not the Fed’s favorite smoothie.

Consumer: The personal saving rate fell to 2.6% in April, down from 3.2% in March and 4.3% in January. Consumers are still spending, but they are increasingly dipping into savings to do it.

Housing: New-home sales fell 6.2% in April to a 622,000 annualized pace, while new-home inventory rose to 489,000 units, equal to 9.4 months of supply. Higher rates are clearly weighing on affordability and builder traffic.

1) Market Analysis -What Hit This Morning

Today’s market theme is relief, but not resolution.

Markets are responding positively to hopes that the U.S. and Iran may extend a ceasefire and move toward reopening the Strait of Hormuz. Oil prices eased today, with Brent crude around $92.18 and U.S. crude near $88.09, helping reduce some inflation pressure at the margin. That matters because high oil prices have been one of the key forces pushing inflation expectations, Treasury yields, and mortgage rates higher.

But the inflation problem did not disappear overnight. April PCE came in at 3.8% year over year, the fastest pace in roughly three years, while core PCE rose 3.3%. That keeps the Fed in a cautious posture even if oil is finally giving markets a little breathing room.

Narrative you can use:

Markets are getting relief from lower oil and better geopolitical headlines, but inflation is still too high for the Fed to declare victory. This is a better setup than last week’s panic, but not yet a clean rate-rally trend. In mortgage terms: constructive, not conclusive.

2) Fed Watch

The Fed’s target range remains 3.50% to 3.75%, and the next FOMC meeting is scheduled for June 16–17. The Fed’s latest statement kept policy unchanged and emphasized incoming data, the evolving outlook, and the balance of risks.

Fed Vice Chair Michelle Bowman said today that an extended Middle East energy shock could shift the policy outlook, especially if higher energy prices broaden into more persistent inflation. That is important because even Fed officials who have leaned more dovish are now warning that inflation risk could force a policy rethink if the energy shock lasts.

Bottom line:

The Fed is not ready to cut. The debate has moved closer to hold vs. hike, not hold vs. cut. That is not the bedtime story buyers want, but it is the story the bond market is reading.

3) Market Analysis -Where Mortgage Rates Actually Are

Freddie Mac’s latest PMMS shows the 30-year fixed-rate mortgage averaged 6.53% as of May 28, up from 6.51% the prior week. The 15-year fixed averaged 5.87%, up from 5.85%. Freddie Mac also notes PMMS is released weekly on Thursdays and reflects average rates offered during the prior Thursday-through-Wednesday window.

Daily market readings are a little more responsive to current bond movement, and Bankrate/WSJ reported the national average 30-year fixed around 6.56% today, down modestly but still elevated.

Practical read:

Rates are workable, but not forgiving. The real conversation is not just, “What is the rate?” It is:

What is the payment? What credits are available? Is a buydown smart? Does an ARM make sense? What is the refinance path if the market improves?

That is where deals are made right now.

4) Market Analysis -Housing Market Check

New-home sales fell 6.2% in April to a 622,000 annualized pace and were down 11.3% year over year. Inventory rose to 489,000 homes, equal to 9.4 months of supply, while the median new-home price rose 2.2% year over year to $422,500.

Pending home sales were more encouraging earlier this month, rising 1.4% in April and 3.2% year over year, showing that demand still exists when buyers see better inventory, better negotiation, or temporary rate relief.

What this means:

Housing is not dead. It is picky, payment-sensitive, and allergic to bad structure. Buyers need options, sellers need flexibility, and agents need financing strategy at the front of the conversation — not three days before loan docs.

5) Market Analysis -Political Backdrop & Fed Independence

The political and geopolitical backdrop remains central to rates. Reuters reported that May was a wild month for global bonds as the Iran war pushed yields to multi-year highs, oil moved sharply, and investors wrestled with inflation, public debt, and Fed credibility. The 30-year Treasury yield even touched around 5.2% earlier in the month, its highest since 2007, before peace-talk hopes and softer data helped yields retreat.

Markets are also watching Fed independence under new Chair Kevin Warsh. Reuters noted that some investors are concerned about Fed credibility if policy were to ease despite elevated inflation, especially with fiscal dynamics already pressuring longer-term Treasury yields.

Translation:

Mortgage rates are not just following housing data. They are following oil, inflation, foreign policy, Treasury supply, Fed credibility, and whether consumers can keep spending without draining savings. Apparently, a rate sheet now needs a passport and a political science minor.

6) What This All Means for Rates Going Forward

| Scenario | What Needs to Happen | Likely Rate Impact |

| Best Case | Oil continues lower, Hormuz risk eases, PCE cools, labor softens gradually | Mortgage rates drift lower |

| Base Case | Inflation stays sticky, oil remains volatile, Fed holds steady | Rates stay choppy in the mid-to-upper 6s |

| Risk Case | Energy prices spike again, inflation expectations rise, Fed turns more hawkish | Rates push higher and reprice risk increases |

My read: today is constructive, but not a victory lap.The bond market likes lower oil and ceasefire progress, but mortgage rates need sustained improvement in inflation and Treasury demand before we can call this a real trend.

7) Market Analysis -Practical Takeaways

For buyers:

Do not wait for the perfect rate. Perfect rates are like perfect inspection reports — beautiful, rare, and usually followed by fine print. Focus on payment, seller credits, buydowns, program fit, and long-term flexibility.

For homeowners:

Refinance decisions remain case-by-case. Cash-out, debt consolidation, HELOC alternatives, ARM reset planning, and future refinance strategy should all be reviewed individually.

For agents:

This is a payment strategy market. The strongest agents are not just saying, “rates are high.” They are showing buyers how credits, buydowns, price negotiation, and loan structure change the monthly payment.

8) Lock vs Float

- Lock bias: If closing within 30 days, the borrower is payment-sensitive, or the file is tight on ratios, locking remains the cleaner recommendation.

- Float bias: Floating can make sense only with more time, stronger borrower flexibility, and a defined trigger. Today’s bond backdrop is better, but headline risk is still very real.

Today’s guidance:

Bias toward locking short-term closings. For longer timelines, cautious floating may be reasonable only if the borrower understands the risk and has a clear ceiling for pain. Floating without a plan is not strategy.

Stay safe and make today great!