Good Friday (and Good Friday) morning from your Hometown Lender. Here’s your Friday market analysis

Please pray for the view of the F15 shot down in Iran today. The first time Iran has shot down a US plane during the war. Clearly, we don’t own all the airspace over Iran as we have been told. I suspect this was a Russian missile, but I am often a conspiracy theorist. Regardless, it is heartbreaking.

On to markets, yesterday saw bonds start the day with big losses after President Trump’s address to the nation, but a strong recovery to end the day in positive territory. Mortgage bonds improved from about 9 am till 12 pm and held the gains through close.

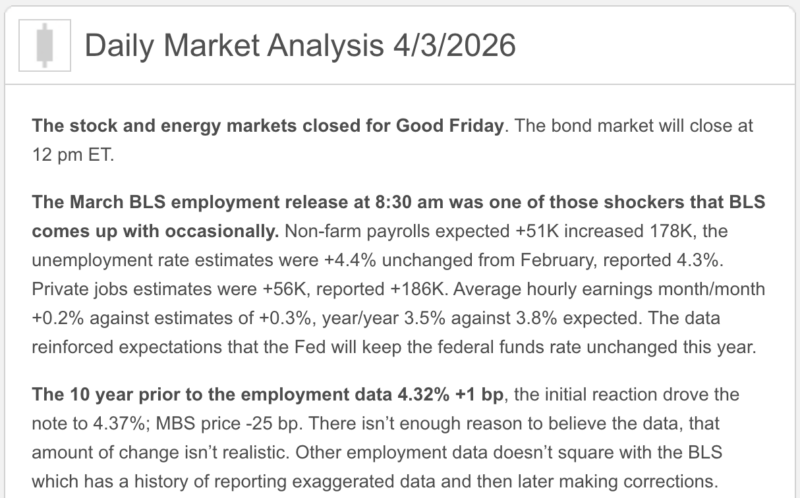

Rates are slightly better than this morning, despite the Jobs report showing 178,000 jobs created and unemployment falling to 4.3%. There are, of course, backward-looking revisions, but this report is not credible (why traders took it with a grain of salt for the most part). The decline in the unemployment rate came with an asterisk: The labor force shrank by nearly 400,000 people, meaning fewer people were counted as unemployed. The share of Americans working or looking for work slipped to 61.9%, its lowest level since the fall of 2021. That means the “real” unemployment would be higher.

Although the initial reaction was bad, bonds quickly started to recover, which we have seen happen before as traders dig past the strong headline numbers to see that the labor market is not nearly as strong as the headlines would make it appear. Today will bring reduced trading volume, it’s Good Friday and the bond market closes at 2pm ET, and will be closed Sunday for Easter.

Market Analysis – From a higher and better view:

Market Analysis – Quick Snapshot

- The big headline this morning was jobs, and it came in stronger than expected: nonfarm payrolls rose 178,000 in March, unemployment held at 4.3%, and average hourly earnings rose 0.2% month over month and 3.5% year over year. In plain English: the labor market still has more pulse than the bond market wanted to see.

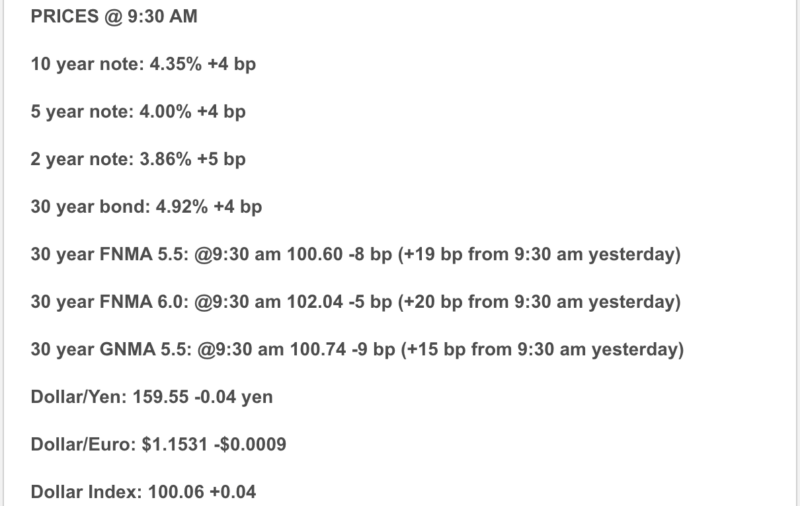

- The 10-year Treasury was around 4.35% after the report, while U.S. stock markets are closed today for Good Friday. Translation: thinner holiday conditions, but rates still took the payroll number seriously.

- The Fed’s target range remains 3.50% to 3.75%. At its March meeting, the Fed held steady, said inflation remains somewhat elevated, and its median year-end fed funds projection was 3.4%, which still implies roughly one 25 bp cut this year.

- The latest inflation data we actually have are still a mixed bag: February CPI was 0.3% monthly and 2.4% yearly; core CPI was 0.2% monthly and 2.5% yearly. January PCE was 0.3% monthly and 2.8% yearly; core PCE was 0.4% monthly and 3.1% yearly.

- Freddie Mac’s weekly survey shows the 30-year fixed at 6.46% and the 15-year fixed at 5.77% as of April 2. Existing-home sales rose in February to 4.09 million, with 1.29 million homes for sale, 3.8 months of supply, and a $398,000 median price.

1) Market Analysis – What Hit This Morning

- The March jobs report was the main event, and it was firmer than consensus. Payrolls rose 178,000, February was revised down to -133,000, and January was revised up to 160,000. Health care added 76,000 jobs, construction added 26,000, and federal employment fell another 18,000.

- There was some softness under the hood. The labor force participation rate was 61.9%, the employment-population ratio was 59.2%, and Reuters noted that about 396,000 people exited the labor force in March. That means the lower unemployment rate was not purely a “growth is booming” story.

- Yesterday’s jobless claims also reinforced the idea that layoffs remain low: initial claims fell to 202,000. So the labor market is not falling apart. It is more like a plane still flying, just with more turbulence lights on.

Narrative you can use:

“Today’s jobs report told the market the economy still has some muscle. That is good news for Main Street, but it is not an instant gift for mortgage rates, because stronger hiring plus oil-driven inflation pressure gives the Fed more reason to stay patient.”

2) Fed Watch

Officially, the Fed is still in wait-and-see mode. The March 18 statement said the economy has been expanding at a solid pace, job gains had remained low, and inflation remains somewhat elevated. The current policy range is still 3.50% to 3.75%.

Today’s jobs number makes an April hold look even more entrenched. The Fed’s own March projections still showed a 3.4% median fed funds rate for year-end 2026, which implies one cut, but a hotter labor print and renewed energy pressure make the path to that cut bumpier. Barron’s, citing CME FedWatch, reported markets still overwhelmingly expect no April change.

3) Market Analysis – Where Mortgage Rates Actually Are

Freddie Mac’s survey average for the week ending April 2 moved up to 6.46% on the 30-year fixed from 6.38% the prior week, while the 15-year fixed rose to 5.77% from 5.75%. That is a reminder that mortgage rates care a lot more about the bond market, inflation expectations, and risk premium than about some future fairy-tale Fed cut.

So yes, the Fed held steady. But the market heard stronger jobs, higher oil, and ongoing geopolitical stress, and basically said: “Cool story, still not cutting you a discount.”

4) Market Analysis – Housing Market Check

- Housing is hanging in there, but it is still a market that rewards realistic pricing and prepared buyers. Existing-home sales increased 1.7% in February to a 4.09 million annual pace, inventory rose to 1.29 million units, and supply stayed at 3.8 months. The median existing-home price was $398,000, up 0.3% year over year.

- One encouraging piece: NAR said its Housing Affordability Index improved for the eighth straight month to 117.6, the highest since March 2022. That is real improvement, even if it still does not feel like a buyer’s-market parade.

- For the West, sales were actually stronger month to month, up 8.2%, while the median price in the region was down 1.9% year over year. That is a useful reminder that national housing data are one thing, but local markets still have their own personality disorders.

5) Political Backdrop & Fed Independence

- The biggest political-macro issue right now is still the Iran/Hormuz conflict. Reuters reported the war has intensified worries about inflation, supply chains, and global growth, and oil prices surged sharply this week; Reuters said WTI briefly neared $114 and Brent approached $109 after the latest escalation rhetoric. AP also reported the national average gasoline price moved back above $4 per gallon.

- Trade policy is also still messy. After the Supreme Court struck down Trump’s broad tariff program in February, Reuters reported the administration shifted to a temporary global tariff approach and, on April 2, ordered 100% tariffs on certain branded pharmaceutical imports while also revising steel, aluminum, and copper duties. None of that screams “easy disinflation.”

- And this morning’s fiscal headline did not exactly calm bond nerves either: Reuters reported Trump’s proposed FY2027 budget would push defense spending to $1.5 trillion while cutting non-defense discretionary spending by 10%. Whether Congress follows that script or rewrites it in red ink, fiscal policy remains a market-moving variable.

6) Market Analysis – What This All Means for Rates Going Forward

- My base case: near-term mortgage pricing stays choppy to slightly worse unless oil cools off and upcoming inflation reports cooperate. Stronger jobs plus geopolitical inflation risk is not a friendly short-term combo for bonds.

- Better case for rates: next week’s February PCE on April 9 and March CPI on April 10 come in soft enough to calm inflation nerves, and the energy spike proves temporary. That could pull Treasury yields back down and improve mortgage pricing. This is an inference, but it is grounded in how the market is currently reacting to inflation and energy risk.

- Worse case for rates: oil stays elevated, tariffs widen, and inflation expectations drift up. In that world, the Fed gets even more cautious, the 10-year stays elevated or rises, and mortgage rates remain sticky in the mid-to-upper 6s. Also known as the bond market’s version of “we need to talk.”

7) Market Analysis – Practical Takeaways

- For buyers, the backdrop is still workable, but monthly payment sensitivity remains real. Affordability has improved from where it was, yet today’s rate environment still rewards strategy, seller concessions, buydowns, and smart structuring over wishful thinking.

- For agents, stronger labor data are helpful for buyer confidence and household stability, but higher financing costs and energy-driven inflation can still create hesitation. In other words: demand is alive, but it is picky.

- For refi and move-up conversations, this is not the market to assume improvement just because the Fed is eventually expected to cut. The timing still depends heavily on inflation and Treasury yields, not just the Fed funds headline.

8) Lock vs Float

- 0–15 days from closing: I would lean lock. A stronger jobs report, higher oil, and thin holiday trading are not the setup I would choose for bravery.

- 15–30 days: more of a case-by-case call. If the borrower is payment-sensitive, tight on DTI, or stress-prone, I would still lean protective. If they can tolerate volatility, next week’s PCE and CPI could matter.

- 30+ days: a cautious float can make sense if you are actively watching data. The next two major inflation checkpoints are April 9 for PCE and April 10 for CPI.

Stay safe and make today great!