Good morning on this fantastic Thursday from your Hometown Lender. Here is today’s wild market analysis!

Yesterday bonds were choppy on news that President Trump said the ceasefire with Iran was over and military strikes would resume. Mortgage bonds have lost about -50bps since Monday, with rates moving up .125 or even .250 for some programs. Even worse when you look at where they are at from the end of June.

Rates this morning are similar to yesterday, as oil prices remain barely below $80 a barrel. Markets are much less concerned about military action than ships moving through the Strait of Hormuz, which for now has seen a reduction in traffic but isn’t at a standstill like it was previously. If reports increase that Iran is able to stop traffic, and oil prices rise, expect rates to do the same. However, if anything happens that helps oil prices fall, we would see the improvements on rate sheets.

While it’s ok to cautiously float to start the day, reprice risk is moderate and many loans will want to lock at the first sign of trouble or by day’s end.

Market Analysis – From a higher and better view:

Market Analysis – Quick Snapshot

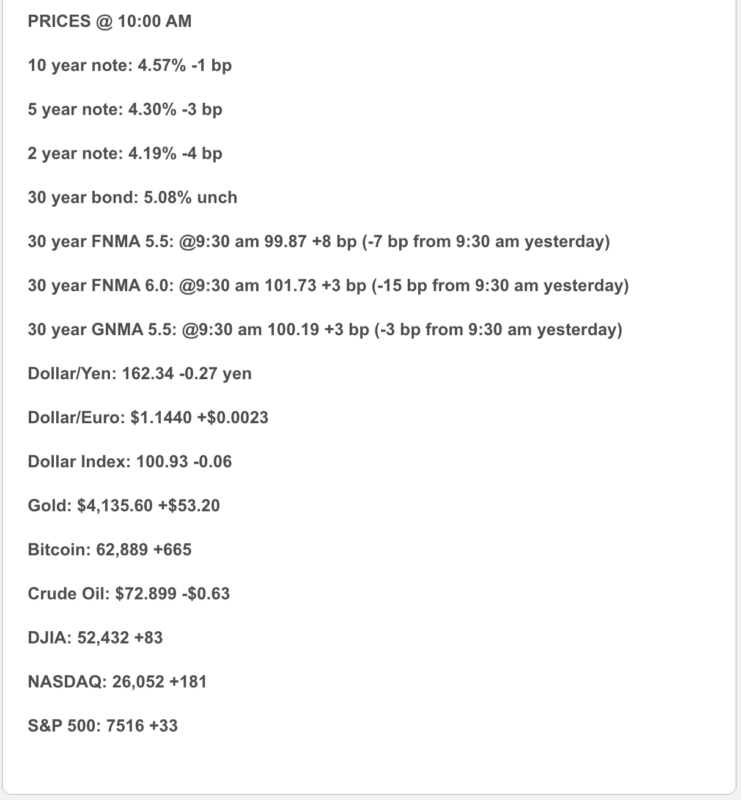

- Bonds: The 10-year Treasury is near 4.56%, slightly lower on the day but still elevated as markets balance stable labor data, renewed Middle East tension, oil volatility, and hawkish Fed minutes. Bonds are calmer — but still sleeping with one eye open.

- Mortgage Rates: Daily tracking shows the 30-year fixed around 6.56% and the 15-year fixed around 5.83%. Freddie Mac’s latest weekly survey shows the 30-year fixed at 6.49% and the 15-year fixed at 5.82%.

- Labor: Initial jobless claims fell to 215,000, while continuing claims rose slightly to 1.814 million. Translation: layoffs remain low, but hiring is still slow and selective.

- Fed Watch: The June Fed minutes showed growing inflation concern. A few officials saw a case for hiking at the June meeting, and 9 of 18 policymakers now see rates higher by year-end.

- Oil / Geopolitics: Oil remains volatile after fresh U.S.–Iran strikes and Iranian attacks on U.S. infrastructure in Qatar, Kuwait, and Bahrain. Brent moved near $77–$79 intraday, keeping inflation risk front and center.

- Housing: Existing-home sales fell 2.4% in June to a 4.09 million annualized pace, while the median price hit a record $440,600. Buyers are still active, but affordability is clearly calling the shots.

Market Analysis – What It Means

Today’s tone is cautious but not panicked. Labor remains stable, but inflation and oil risk are keeping the Fed hawkish and mortgage rates elevated.

In plain English: the market is functioning, but it is still making buyers do math before breakfast.

Housing & Mortgage Strategy

This remains a structure-the-payment market.

The best conversations right now are about:

Seller credits, temporary buydowns, permanent buydowns, builder incentives, ARM options where appropriate, and a realistic refinance plan if rates improve later.

Buyers are still active, but they are doing math. Sellers and builders who help solve the monthly payment problem have the best chance of turning interest into contracts.

Lock vs. Float

- Lock bias: If closing within 30 days, the borrower is payment-sensitive, or the file is tight, locking remains the cleaner recommendation.

- Float bias: Floating may make sense only with time, flexibility, and a clear trigger. Oil headlines, inflation data, and Fed commentary can still move bonds quickly.

Market Analysis – Today’s guidance:

Bias toward locking short-term closings. For longer timelines, cautious floating may be reasonable only with a clear risk ceiling and daily monitoring.

Stay safe and make today great!