Good Monday morning from your Hometown Lender. Let’s get right to today’s market analysis!

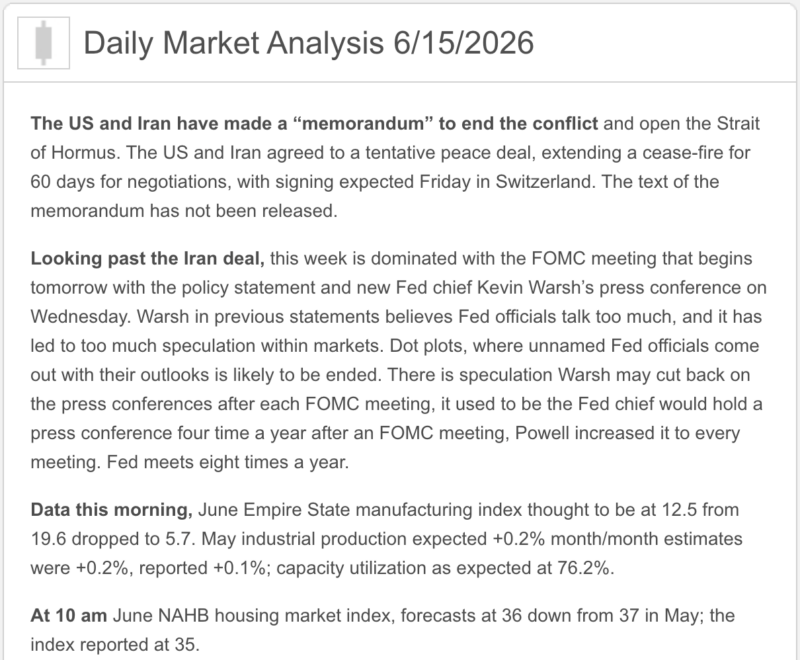

Friday saw bonds lose ground early but then recover as traders parked money over the weekend. All said and done, when the dust settled bonds were flat on the day. News now that the formal signing of the agreement between the U.S. and Iran will be on Friday, although Vice President JD Vance has said there has already been a digital signing of the agreement. The Strait of Hormuz will also open on Friday, giving Iran time to remove the mines that are in place. Oil prices have fallen, and bonds have improved, but not much yet, as traders wait to see it all play out as has been announced.

Rates today though will be better than Friday as bonds improve, and it should be some of the best pricing we’ve seen since early May. Reprice risk on the day is low, as long as something catastrophic doesn’t happen with the deal we shouldn’t have to worry about bonds selling off.

Market Analysis – From a higher and better view:

Market Analysis – Quick Snapshot

Bonds: The 10-year Treasury eased to around 4.44% as markets reacted positively to a preliminary U.S.–Iran peace framework and lower oil prices. Bonds finally got a little good news — not a vacation, but at least they found the exit row.

Mortgage Rates: Daily tracking shows the 30-year fixed around 6.57% and the 15-year fixed around 5.93%. Freddie Mac’s latest weekly survey showed the 30-year fixed at 6.52% and the 15-year fixed at 5.84%.

Fed Watch: The Fed begins its two-day meeting tomorrow, with markets expecting no change to the current 3.50%–3.75% target range. The big focus will be Chair Kevin Warsh’s first Fed press conference and whether he leans patient, hawkish, or more flexible.

Oil / Geopolitics: Oil fell sharply after the U.S. and Iran announced a preliminary framework to end hostilities and reopen the Strait of Hormuz. Lower oil helps the inflation narrative, but the deal still has details to settle.

Housing: Builder sentiment fell again in June, with higher mortgage rates, construction costs, and affordability keeping pressure on new-home demand. Builders are increasingly using price cuts and incentives to move buyers off the fence.

Market Analysis – What It Means

Today’s tone is better because oil is lower and Treasury yields eased.

But the bigger picture has not changed overnight: mortgage rates are still elevated, inflation is still above the Fed’s target, and this week’s Fed meeting is the main event.

In plain English: the market got a little relief, but buyers still need a payment plan.

Market Analysis – Housing & Mortgage Strategy

This remains a structure-the-payment market.

The best conversations right now are about:

Seller credits, temporary buydowns, permanent buydowns, builder incentives, ARM options where appropriate, and a realistic refinance plan if rates improve later.

Buyers are still active, but they are doing math. Sellers and builders who help solve the monthly payment problem have the best chance of turning interest into contracts.

Lock vs. Float

Lock bias: If closing within 30 days, the borrower is payment-sensitive, or the file is tight, locking is still the cleaner recommendation.

Float bias: Lower oil and lower Treasury yields are helpful, but this week’s Fed meeting can move the market quickly.

Today’s guidance:

Bias toward locking short-term closings. For longer timelines, cautious floating may be reasonable only with a clear risk ceiling and a plan before Wednesday’s Fed announcement.

Stay safe and make today great!