Good morning on this best day of the week, Wednesday from your Hometown Lender. Here’s your market analysis!

Yesterday saw bonds drift a bit lower through the early afternoon before rallying strong to end the day at the best levels.

Rate sheets today should be a bit better than yesterday, with mortgage bonds drifting a bit better on the day already. There’s no economic data to worry about, no new headlines about the peace talks with Iran, and nothing to cause any real concerns on the day. Rates aren’t likely to move much lower today, but could continue to slowly creep towards more improvement.

Market Analysis – From a higher and better view:

Market Analysis – Quick Snapshot

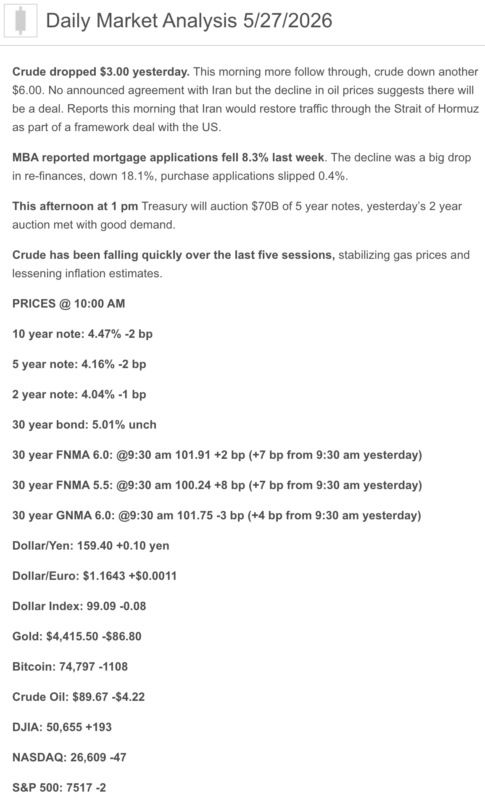

- Bonds: The 10-year Treasury is catching a little relief this morning, moving near 4.47%, its lowest level in roughly two weeks, as oil prices dropped and markets reacted to reports of progress toward a possible U.S.–Iran deal to reopen the Strait of Hormuz.

- Mortgage Rates: Freddie Mac’s latest weekly survey showed the 30-year fixed at 6.51% and the 15-year fixed at 5.85% as of May 21. More current daily readings are still elevated, with Bankrate/WSJ showing the 30-year around 6.62% today.

- Mortgage Demand: MBA data showed mortgage applications fell 8.5% for the week ending May 22, with refi activity hit especially hard as rates pushed higher. That is the market saying, “I love real estate, but can we talk about the payment first?”

- Inflation: April CPI rose 3.8% year over year, with energy up 17.9% and gasoline up 28.4% over the past 12 months. Core CPI rose 2.8% year over year, and shelter remained sticky.

- Housing: Existing-home sales rose 0.2% in April to a 4.02 million annualized pace. Inventory improved to 1.47 million homes, equal to 4.4 months of supply, while the median existing-home price rose 0.9% year over year to $417,700.

1) Market Analysis – What Hit This Morning

Today’s market theme is relief rally, but not a victory lap.

Oil prices dropped sharply after reports that Iran and the U.S. may be moving toward a draft agreement that could eventually reopen the Strait of Hormuz. Reuters reported Brent crude down to about $95.59 and WTI near $88.91, both at roughly one-month lows. Lower oil helps the inflation narrative, which helps bonds, which can eventually help mortgage pricing.

But the word eventually matters. Markets are still waiting on key U.S. data due tomorrow, including PCE inflation, GDP, and jobless claims. Today’s bond improvement is encouraging, but one softer oil headline does not erase sticky CPI, high energy costs, or Fed caution.

Narrative you can use:

Rates are getting a little help today because oil is lower and geopolitical risk may be cooling. But the Fed still needs actual inflation improvement before the market can believe in a sustainable rate move lower. In other words: good day for bonds, not yet a parade.

2) Fed Watch

The Fed’s current target range remains 3.50% to 3.75%. In its April statement, the Fed said economic activity was expanding at a solid pace, inflation remained elevated, and uncertainty around the Middle East was contributing to economic risk.

The April meeting minutes showed the Fed is not united around easy cuts. Stephen Miran preferred a 0.25% cut, while Beth Hammack, Neel Kashkari, and Lorie Logan supported holding rates steady but did not support keeping an easing bias in the statement. The next Fed meeting is scheduled for June 16–17, 2026.

Minneapolis Fed President Neel Kashkari also emphasized today that inflation risk remains the main focus and said it is too early to predict the timing of the next rate move.

Bottom line:

The Fed is not saying “cuts are coming.” The Fed is saying “show us the data.” Bonds like hope, but the Fed wants receipts.

3) Market Analysis – Where Mortgage Rates Actually Are

Freddie Mac’s weekly survey showed the 30-year fixed at 6.51%, up from 6.36% the prior week. The 15-year fixed moved to 5.85%, up from 5.71%. Freddie Mac’s PMMS is a weekly average, so it can lag daily rate movements when the bond market moves quickly.

Daily rate readings are still showing pressure in the mid-to-upper 6% range. WSJ/Bankrate showed the average 30-year fixed around 6.62% today, down slightly but still elevated.

Practical read:

Rates are not friendly, but they are workable. The goal is not to wait for a perfect rate. The goal is to structure the file intelligently: seller credits, temporary buydowns, permanent buydowns, ARM options where appropriate, and a clear refinance strategy if the market gives us that window later.

4) Market Analysis – Housing Market Check

April existing-home sales increased 0.2% month over month to a 4.02 million annualized pace. Inventory rose 5.8% from March to 1.47 million homes, equal to 4.4 months of supply. The median existing-home price rose 0.9% year over year to $417,700, marking the 34th consecutive month of year-over-year price gains.

What this means:

Buyers have more choices than they had during the frenzy, but affordability is still the speed bump. Sellers are not giving homes away, but more inventory gives buyers more room to negotiate. This is where payment strategy, credits, and structure can turn a “maybe” into a closed escrow.

5) Political Backdrop & Fed Independence

The political and geopolitical backdrop remains directly tied to mortgage rates. Markets are reacting to potential progress on a U.S.–Iran agreement, but Reuters noted the situation remains fragile, with continued questions around whether any deal is final and how quickly oil flows normalize.

The key connection is simple: lower oil can reduce inflation pressure; lower inflation pressure can help Treasuries; lower Treasury yields can improve mortgage pricing. But if the truce breaks down or oil jumps again, bonds can give back gains quickly. Tiny violin for bond traders, big payment impact for buyers.

Translation:

Mortgage rates are not only following housing data right now. They are following inflation, oil, global conflict, Fed credibility, and Treasury demand.

6) Market Analysis – What This All Means for Rates Going Forward

| Scenario | What Needs to Happen | Likely Rate Impact |

| Best Case | Oil continues lower, PCE improves, labor softens gently, Fed rhetoric cools | Mortgage rates drift lower |

| Base Case | Inflation stays sticky, oil remains volatile, Fed waits for more data | Rates stay choppy in the mid-to-upper 6s |

| Risk Case | Oil spikes again, inflation expectations rise, Fed turns more hawkish | Rates push higher and reprice risk increases |

My read: today is constructive, but not conclusive. Bonds are getting relief, but mortgage pricing needs sustained improvement in inflation and Treasury yields before we can call this a real trend.

7) Market Analysis – Practical Takeaways

For buyers:

Do not wait for the perfect rate. Perfect rates are like perfect inspection reports — beautiful, rare, and usually followed by fine print. Focus on payment, seller credits, buydowns, program choice, and long-term flexibility.

For homeowners:

Refinance decisions remain case-by-case. Cash-out, debt consolidation, HELOC alternatives, ARM reset planning, and future refi strategy should all be evaluated individually.

For agents:

This is a payment strategy market. The best agents are not just saying, “rates are high.” They are showing buyers how credits, buydowns, and price negotiation actually change the monthly payment.

8) Lock vs Float

- Lock bias: If closing within 30 days, the borrower is payment-sensitive, or the file is tight on ratios, locking remains the safer play.

- Float bias: Floating can make sense for longer timelines if the borrower has flexibility, understands the risk, and has a defined trigger.

Today’s guidance:

Bias toward locking short-term closings. For longer timelines, today’s bond improvement may justify cautious floating, but only with a plan. Floating without a plan is not strategy

Stay safe and make today great!