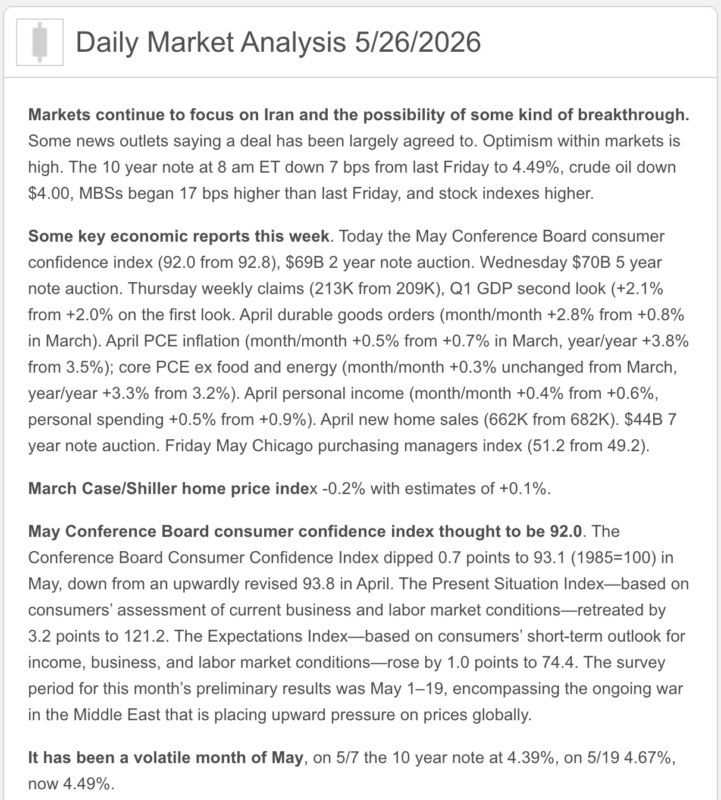

Good Tuesday AM from your Hometown Lender. Here is the latest market analysis!

Friday was a calm day for bonds, with the bond market closing at 2pm and remaining closed Monday in observance of Memorial Day. Mortgage bonds closed right around the same levels as they started.

Today, despite headlines of military attacks yesterday, the ceasefire remains in effect with Iran and negotiations continue, and bonds starting the week off with more gains. That means rate sheets this morning will continue to improve, although it’s still small increments at a time. Reprice risk on the day is moderate, the potential for volatility remains constant with the threat of a breakdown in negotiations with Iran hanging over our heads.

Rates will continue to follow the headlines and track oil prices, with Brent crude currently still below $100 a barrel. As long as negotiations continue and the ceasefire remains in effect, we don’t have to worry about locking today.

Market Analysis – From a higher and better view:

Market Analysis – Quick Snapshot

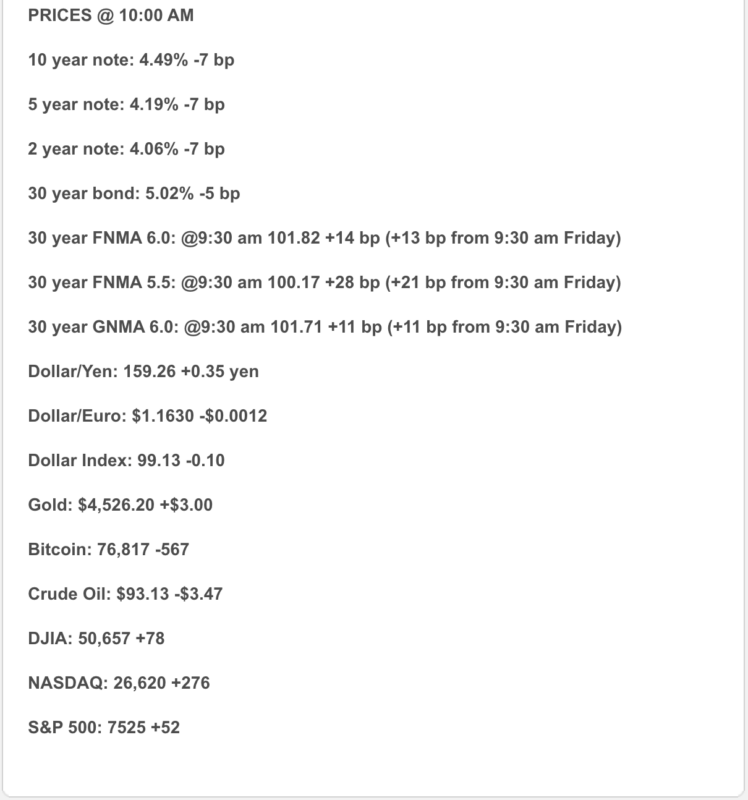

Bonds: The 10-year Treasury is catching a little relief today, trading around 4.48% after recent pressure pushed yields higher. The move lower is tied to hopes that U.S.–Iran tensions may ease and oil-flow concerns may calm down. Bond traders apparently do have feelings — they just express them in basis points.

Mortgage Rates: Freddie Mac’s latest weekly survey showed the 30-year fixed at 6.51% and the 15-year fixed at 5.85% as of May 21, both higher than the prior week. Daily rate trackers are showing even more pressure, with Bankrate’s national average 30-year fixed around 6.70% today.

Inflation: April CPI rose 0.6% month over month and 3.8% year over year, while core CPI rose 0.4% monthly and 2.8% annually. Energy remains the villain in the movie, with energy prices up 17.9% year over year and gasoline up 28.4%.

Consumer Mood: The Conference Board Consumer Confidence Index slipped to 93.1 in May from 93.8 in April, as high gas prices and inflation continued to pressure households. AP reported the national average gas price around $4.49 per gallon, which explains why consumers are not exactly skipping into Costco.

Housing: Existing-home sales rose 0.2% in April to a 4.02 million annualized pace, inventory improved to 1.47 million homes, and supply increased to 4.4 months. Prices are still positive year over year, but buyers are more cautious and payment-sensitive.

1) Market Analysis – What Hit This Morning

Today’s market theme is relief, but not victory.

Treasury yields are lower today because markets are reacting positively to the possibility of progress toward a U.S.–Iran peace deal and a reopening of key oil routes. That matters because the recent oil spike has been feeding directly into inflation fears, Treasury yields, and mortgage rates.

Consumer confidence also came in slightly weaker, with the index falling to 93.1. The decline was not dramatic, but the message is clear: consumers are still feeling inflation, gas prices, and affordability pressure. Two-thirds of respondents in the Conference Board survey said they are cutting back spending because of rising prices.

Narrative you can use:

Markets are getting a little relief today because geopolitical risk may be cooling, but inflation is still too hot for the Fed to relax. In mortgage terms: better day for bonds, but not yet a “rates are fixed” day. We are not popping champagne; maybe just opening a Diet Coke.

2) Fed Watch

The Fed’s current target range remains 3.50% to 3.75%, and the next FOMC meeting is scheduled for June 16–17, 2026.

The latest Fed minutes showed a divided but cautious Committee. Several participants said cuts could be appropriate if disinflation gets firmly back on track or the labor market weakens, but a majority said additional policy firming could become appropriate if inflation remains persistently above 2%.

Bottom line:

The Fed is not in cut mode. It is in “prove it” mode. Inflation needs to cool, energy needs to settle, and labor needs to soften before the Fed gets comfortable moving lower.

3) Market Analysis – Where Mortgage Rates Actually Are

The latest Freddie Mac weekly survey has the 30-year fixed at 6.51%, up from 6.36% the prior week. The 15-year fixed moved to 5.85%, up from 5.71%. Freddie’s survey is weekly, so it smooths the data a bit; daily pricing can move faster when Treasuries and MBS react sharply.

Daily market readings are showing pressure closer to the upper-6% range, with Bankrate’s national average 30-year fixed near 6.70% today. Real borrower pricing will still depend on credit score, loan size, occupancy, property type, points, lock period, and program fit.

Practical read:

Rates are not friendly, but they are workable. The strategy is not “wait and hope.” The strategy is structure: seller credits, buydowns, ARM options where appropriate, permanent rate reductions, and a clear refinance plan if/when the market allows.

4) Market Analysis – Housing Market Check

April existing-home sales increased 0.2% to a 4.02 million annualized pace. Inventory rose 5.8% from March to 1.47 million homes, equal to 4.4 months of supply, while the median existing-home price rose 0.9% year over year to $417,700.

Today’s FHFA data also showed U.S. single-family home prices rose 0.1% in March and 1.7% year over year. That is slower appreciation, but still positive nationally, with limited starter-home inventory continuing to support prices.

What this means:

Buyers have more options than they did during the frenzy, but affordability is still the choke point. Sellers are not giving homes away, but the days of “list it, blink, and get 12 offers” are not exactly back either.

5) Political Backdrop & Fed Independence

The political and geopolitical backdrop is directly tied to rates right now. Treasury Secretary Scott Bessent said last week that elevated bond yields and headline inflation may prove “transient” if the Iran conflict ends and energy prices normalize. At the same time, he acknowledged that central bankers are focused on inflation risk, especially while oil prices remain elevated.

Markets are reacting today to hopes that the U.S. and Iran may be closer to a deal, which could ease oil prices and reduce some inflation pressure. But the situation remains fragile, and the Fed is not going to base policy on one good headline.

Translation:

Lower oil helps bonds. Lower bonds help mortgage pricing. But until inflation data actually improves, the Fed will keep its hand near the brake pedal.

6) Market Analysis – What This All Means for Rates Going Forward

| Scenario | What Needs to Happen | Likely Rate Impact |

| Best Case | Iran tensions cool, oil prices drop, inflation data improves, labor softens gently | Mortgage rates drift lower |

| Base Case | Inflation stays sticky, Fed waits, oil remains volatile | Rates stay choppy in the mid-to-upper 6s |

| Risk Case | Energy prices re-accelerate, inflation expectations rise, Fed turns more hawkish | Rates push higher and reprice risk increases |

My read: today is constructive, but not conclusive. A bond rally helps, but the market needs several cleaner inflation readings before mortgage rates can build a meaningful downward trend.

7) Market Analysis – Practical Takeaways

For buyers:

Do not wait for the perfect rate. Perfect rates are like perfect inspection reports — wonderful, rare, and usually followed by fine print. Focus on payment, credits, structure, and long-term flexibility.

For homeowners:

Refinance decisions remain case-by-case. Cash-out, debt consolidation, HELOC alternatives, ARM reset planning, and future refi strategy should all be evaluated individually.

For agents:

This is a payment strategy market. The best conversations right now are not “rates are high.” They are “here is how we can use credits, buydowns, price negotiation, and loan structure to make the payment work.”

8) Lock vs Float

Lock bias: If closing within 30 days, the borrower is payment-sensitive, or the file is tight on ratios, locking remains the safer play.

Float bias: Floating can make sense only if the borrower has time, flexibility, and a clear trigger. Today’s bond improvement is helpful, but geopolitical headlines can reverse quickly.

Today’s guidance:

Bias toward locking short-term closings and carefully floating longer timelines only with a defined ceiling for risk. In this market, floating without a plan is not strategy

Stay safe and make today great!