Happy Cinco de Mayo from your Hometown Lender. Let’s get into today’s market analysis.

Yesterday was bad for bonds on heightened concerns the ceasefire was cracking. It is amazing that we can allow for some aggression by Iran without it violating the ceasefire. Rates are a bit better than the worst pricing we saw yesterday as bonds recover.

Most of the gains can be attributed to the relative calm returning to the Persian Gulf. The Pentagon said that even though Iran fired on commercial vessels and seized two ships, the actions don’t rise to the level of restarting the bombing and military action. As long as the skirmishes stay small enough that negotiations can continue, markets should calm down a bit. However, market analysis tells us not to expect rates to improve that much until a deal is struck and the Strait of Hormuz is fully open.

Market Analysis – From a higher and better view:

Market Analysis –Quick Snapshot

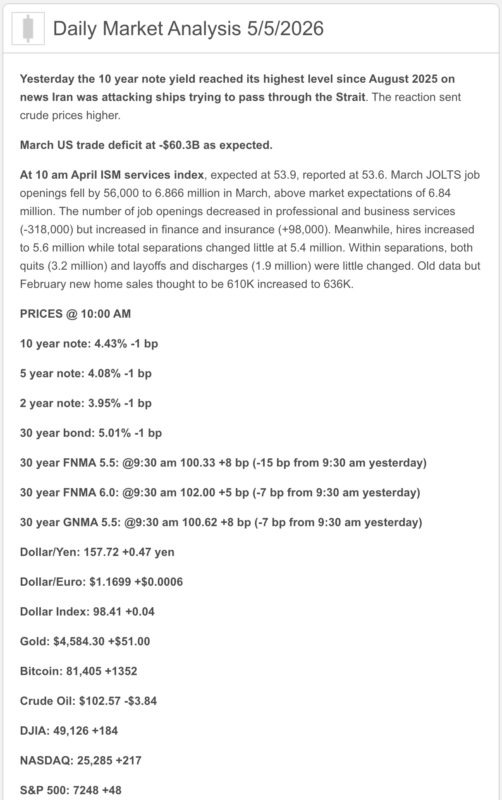

- Services are still expanding, but momentum cooled. ISM services slipped to 53.6 in April from 54.0, while new orders fell sharply to 53.5 from 60.6 and the prices-paid index stayed at 70.7, its highest since late 2022.

- The labor market still looks stable, not soft. March job openings dipped to 6.866 million, but hires jumped to 5.554 million and layoffs rose modestly to 1.867 million.

- Trade remains a GDP headwind. The U.S. trade deficit widened to $60.3 billion in March, and Reuters said trade subtracted 1.3 percentage points from Q1 GDP growth.

- Housing gave a mixed but usable signal. New home sales rose 7.4% in March to 682,000, supply eased to 8.5 months, and the median new-home price fell 6.2% year over year to $387,400.

- Markets are trying to look past the Middle East, but oil is still the chaperone. At 10:01 a.m. ET, the Dow was up 0.51%, the S&P 500 up 0.67%, and the Nasdaq up 0.83%. Oil was down on the day, but Brent remained above $110, with Hormuz disruption still hanging over inflation and rates.

- The Fed is still on hold at 3.50% to 3.75%. In its April 29 statement, the Fed said inflation is elevated and Middle East developments are contributing to a high level of uncertainty. Freddie Mac’s latest survey shows the 30-year fixed at 6.30% and the 15-year fixed at 5.64% as of April 30.

1) Market Analysis -What Hit This Morning

Today’s data told a familiar story: the economy is still moving, but not in a way that gives rates much breathing room. Services growth cooled, new orders lost some steam, and hiring improved in JOLTS, which keeps the labor backdrop from looking weak. At the same time, service-sector price pressure stayed hot, so the market got a little growth cooling without the gift of cleaner inflation.

Narrative you can use:

“Today’s reports showed the economy is still functioning, but inflation pressure has not backed off enough to make the Fed comfortable. That is why mortgage rates are getting some support from decent housing demand, but not the kind of relief borrowers would love.”

2) Market Analysis -Fed Watch

The Fed is still in wait-and-see mode, and the official language remains cautious. It held the target range at 3.50% to 3.75%, said inflation is elevated, and flagged Middle East uncertainty as a risk to the outlook.

The market is drifting more hawkish, not less. Barclays became the latest major firm to forecast no Fed cuts in 2026, pushing its first expected cut into March 2027. That does not mean cuts are impossible, but it does mean the “later for longer” crowd keeps stealing the microphone.

3) Market Analysis -Where Mortgage Rates Actually Are

Freddie Mac’s latest weekly read shows the 30-year fixed at 6.30% and the 15-year fixed at 5.64%. Freddie Mac also said purchase applications are running more than 20% above a year ago, which tells you buyers are still in the game even with rates in the mid-6s.

The big picture has not changed: mortgage pricing is still being pushed around more by oil, inflation expectations, and Treasury sentiment than by dreams of quick Fed cuts. Today’s rebound in stocks is nice, but Brent still sitting north of $110 is the part bond traders keep circling in red ink.

4) Market Analysis -Housing Market Check

Housing is still giving a mixed but workable signal. New home sales improved in March, supply came down a bit, and prices eased year over year, which helps affordability on the margin. That is constructive, even if it is not exactly confetti-cannon constructive.

The main caution is that the outlook still depends heavily on rates and energy. Reuters noted the spring housing market could struggle to hold momentum if war-driven mortgage-rate pressure returns. So yes, demand is there, but it still has trust issues.

5) Political Backdrop & Fed Independence

The political and macro story is still the Gulf. Reuters reported fresh attacks rattled the fragile truce, including a strike that set a fire at Fujairah, a critical UAE oil-export hub outside Hormuz. Even with oil lower today, the broader disruption story is still very much alive.

On the Fed side, Kevin Warsh has already cleared committee, and Reuters says a full Senate confirmation vote is expected the week of May 11, with Powell’s chair term ending May 15. So markets are not just pricing today’s Fed. They are also pricing the next one.

6) Market Analysis -What This All Means for Rates Going Forward

Base case: rates stay choppy but sticky, because services are still expanding, the labor market is still stable, and geopolitical inflation risk has not gone away.

Better case: oil backs off further, supply through Hormuz improves, and this week’s labor data soften enough to calm the bond market. Reuters’ week-ahead coverage says the next key focus is still the labor calendar, especially Friday’s jobs report.

Worse case: oil turns back up, Friday’s jobs report comes in firm, and markets push the first cut even farther out. That is how mid-6s mortgage rates stick around like an unwanted houseguest.

7) Practical Takeaways

For buyers, this is still a market where structure beats hope. The weekly mortgage survey is not bad, new-home supply is workable, and builders still have product to move. But payment sensitivity remains the whole movie, not just the trailer.

For agents and partners, today’s message is balanced: services cooled a bit, job openings edged lower, but hiring jumped and the housing market still has a pulse. Opportunity is there; it just still needs a calculator and a plan.

8) Lock vs Float

0–15 days: lean lock.

15–30 days: case by case.

30+ days: cautious float, but only if the borrower can handle headline-driven swings. Oil is still the loudest voice in the room.