Good Friday morning from your Hometown Lender! Let’s dive into today’s market analysis.

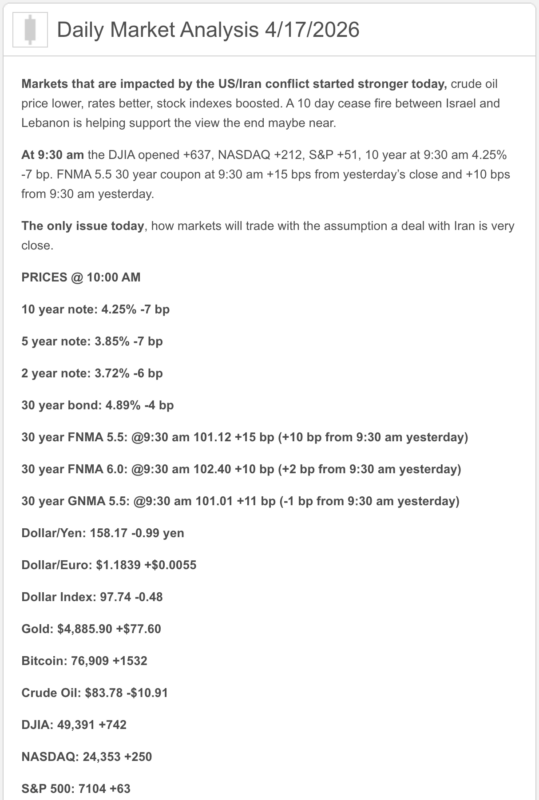

Yesterday bonds drifted a bit lower in price through the day which has the inverse effect on rates although it wasn’t enough to talk about it. Today though, rates are much better, reflecting the strong showing in mortgage bonds after it was announced this morning that the Strait of Hormuz would once again be fully open to commercial traffic. Oil prices fell, and stocks and bonds rallied. More peace talks are expected to take place this weekend, and the Israel-Lebanon cease fire that went into effect yesterday seems to be holding. What a way to end the week.

Market Analysis – From a higher and better view:

Market Analysis – Quick Snapshot

- Today’s market headline is not a U.S. data dump. It’s oil. Reuters reported that after Iran said the Strait of Hormuz is open during the ceasefire, Brent fell more than 11% to about $87.94 and WTI to about $83.33, while the S&P 500 rose 1.15% to a record 7,115.31, the Dow gained 1.95%, and the Nasdaq rose 1.15%.

- The Fed is still on hold at 3.50% to 3.75%. That target range remains in place from the March meeting, and Reuters said markets still expect the Fed to hold again on April 28–29.

- Mortgage rates actually improved this week. Freddie Mac’s latest weekly survey shows the 30-year fixed at 6.30% and the 15-year fixed at 5.65%, both down from the prior week.

- There was no fresh retail-sales or housing-starts release today. Census says the March retail-sales report was pushed to April 21, and the March new residential construction report was pushed to April 29.

- The freshest hard U.S. economic reads are still yesterday’s. Weekly jobless claims fell to 207,000, continuing claims rose to 1.818 million, and March industrial production fell 0.5% while manufacturing dipped 0.1%.

- Housing still looks rate-sensitive. Existing-home sales fell to a 3.98 million annual pace in March, inventory rose to 1.36 million, supply increased to 4.1 months, and median price rose to $408,800. Builder sentiment also dropped to 34 in April, a seven-month low.

1) Market Analysis – What Hit This Morning

There was no major scheduled U.S. economic release this morning, so markets took their cues from the thing that has been bossing rates around for weeks: energy and geopolitics. The reopening of the Strait of Hormuz during the ceasefire sent oil sharply lower, pushed stocks higher, and helped bonds. In plain English, the market woke up and decided maybe inflation does not need to keep doing CrossFit quite so aggressively.

The absence of fresh retail-sales and housing-starts data matters too. Because retail sales were delayed to April 21 and new residential construction to April 29, today’s market had less domestic macro data to react to and more room to obsess over oil, diplomacy, and the Fed path.

Narrative you can use:

“Today’s rate story is simpler than most of this month: lower oil is helping the bond market breathe. We did not get a big U.S. economic report this morning, so falling energy prices and easing Middle East stress are doing most of the heavy lifting for sentiment and mortgage pricing today.”

2) Fed Watch

Officially, the Fed is still parked at 3.50% to 3.75%. Reuters said the April 28–29 meeting is still expected to result in no change, even after today’s oil drop.

Where it gets interesting is the split in expectations. Reuters reported today that Deutsche Bank now expects no Fed cuts in 2026, joining JPMorgan and HSBC on the no-cut side, while Goldman Sachs, Morgan Stanley, and BofA still expect two cuts starting in September. The same Reuters report said LSEG pricing implied about a 69% probability the Fed does not cut by year-end. So the market is still not singing from one hymn book. More like a choir where half the room brought the wrong sheet music.

At the same time, Reuters also reported that the collapse in oil prices could reopen the door to a December cut if the ceasefire holds and energy stays lower. That does not mean cuts are back on the menu with breadsticks, but it does mean the immediate pressure for more hawkish thinking has eased.

3) Market Analysis – Where Mortgage Rates Actually Are

Freddie Mac’s newest weekly survey shows the 30-year fixed at 6.30% and the 15-year fixed at 5.65% as of April 16, down from 6.37% and 5.74% the week before. That is real improvement, not dramatic improvement, but in this market we take wins where we can find them. Even if they arrive wearing a hard hat and carrying oil barrels.

The bigger driver today is that falling oil is helping calm inflation fears and Treasury pressure. Reuters said U.S. Treasury yields declined as oil sank and investors rotated back into bonds. That is exactly the kind of background move that can help mortgage pricing at the margin, even without a fresh “good” domestic data surprise.

4) Market Analysis – Housing Market Check

The freshest existing-home data still say the housing market is moving, but not gliding. Reuters reported that March existing-home sales fell 3.6% to 3.98 million, a nine-month low, while inventory rose to 1.36 million and median price climbed to $408,800. NAR also cut its 2026 existing-home sales growth forecast from 14% to 4%.

New construction is not exactly sending valentines either. Reuters reported builder sentiment fell to 34 in April, the lowest since September 2025, with higher rates, fuel costs, tariffs, and uncertainty all weighing on confidence. That matters because even with resale inventory improving, the new-home side is still telling us affordability and cost pressure are doing plenty of damage.

Also worth noting: we did not get fresh housing starts today because Census pushed the March construction release to April 29. So for now, builder sentiment is our freshest pulse check on the new-home market.

5) Political Backdrop & Fed Independence

The political and macro backdrop is still overwhelmingly about the Middle East and Hormuz. Reuters reported Iran said the Strait of Hormuz would remain open to commercial shipping during the ceasefire, which is why oil fell so sharply and markets rallied. But Reuters also noted the U.S. blockade of Iran remains in place and traders are still watching whether the ceasefire actually sticks.

The Fed angle is still politically live too. Reuters highlighted that next week’s confirmation hearing for Kevin Warsh, Trump’s pick for Fed chair, is a major market focus, especially because he faces pressure to favor easier policy despite inflation risk. That is not directly changing today’s mortgage rate quote, but it absolutely matters for the broader rates conversation and Fed-independence narrative.

6) Market Analysis – What This All Means for Rates Going Forward

Base case:

Mortgage rates stay choppy but a little friendlier if oil stays lower. Falling crude removes some inflation pressure, helps bonds, and gives the market room to talk about cuts again later in the year instead of only “higher for longer.”

Better case for rates:

The better path is that the ceasefire holds, Hormuz stays open, and lower energy prices start flowing through to inflation expectations and consumer costs. If that happens, mortgage pricing could improve a bit more and the December-cut conversation gets louder. This is an inference, but it is grounded in Reuters’ reporting on falling oil, declining Treasury yields, and revived cut expectations.

Worse case for rates:

If the ceasefire cracks, oil snaps back up, and the market decides today was just a temporary sugar rush, rates can back up again quickly. Housing is still fragile enough that this would matter fast, and the Fed is still not fully convinced inflation has behaved itself.

7) Market Analysis – Practical Takeaways

For buyers, this is still a market where structure beats hope. The drop in mortgage rates this week is helpful, but not enough to make payment sensitivity disappear. Buydowns, concessions, and smart product choice still matter a lot.

For agents, today’s message is constructive: lower oil and lower mortgage rates are a better backdrop than what we had a week ago, but existing-home sales and builder sentiment still say confidence is fragile. The market is moving, just not exactly with jazz hands.

For refi and move-up conversations, the honest message is that some relief is showing up, but it is being driven more by geopolitical de-escalation and oil than by a big shift in the Fed. That means the window can improve, but it can also shut faster than people expect.

8) Lock vs Float

0–15 days from closing:

I would still lean lock. Today is better, but this market is still one headline away from changing its mood, and near-term closings do not need extra drama.

15–30 days:

This is more case by case. If the borrower is tight on DTI or very payment-sensitive, I would still favor protection. If they have room, today’s oil move gives a real case for cautious patience.

30+ days:

A cautious float can make sense, but only with discipline. Right now the market is trading ceasefire credibility, oil, and Fed timing all at once. That is not exactly a hammock-and-lemonade setup.

Stay safe, enjoy the weekend, and make today great!