Good Monday morning from your Hometown Lender. Here is your Monday market analysis.

Friday was a calm day, with minimal movement from bonds. Rates are at least as good as Friday, maybe a bit better, as bonds recovered from early losses and shrugged off headlines about the US blockade of Iranian ports in the Strait of Hormuz. Reprice risk on the day is moderate, but we’re not expecting trouble. Over the weekend, President Trump announced the US would blockade Iranian ports in the Strait of Hormuz after negotiations fell apart. The ceasefire still seems to be holding though, at least for now, and although oil prices pushed higher bonds didn’t seem to care. There is no economic data today, and nothing else happening that we need to watch. Only the activity in the Middle East is likely to have any effect on bonds and rate sheets today.

Market Analysis – From a higher and better view:

Market Analysis – Quick Snapshot

- Today is an oil-and-geopolitics day more than a pure data day. The U.S. blockade of ships leaving Iranian ports went into effect Monday after weekend talks broke down. By Reuters’ Monday market update, Brent was at $100.07, WTI at $101.39, and the 10-year Treasury yield was 4.319%. U.S. stocks were soft to mixed, with the Dow down 0.54%, the S&P 500 down 0.10%, and the Nasdaq roughly flat.

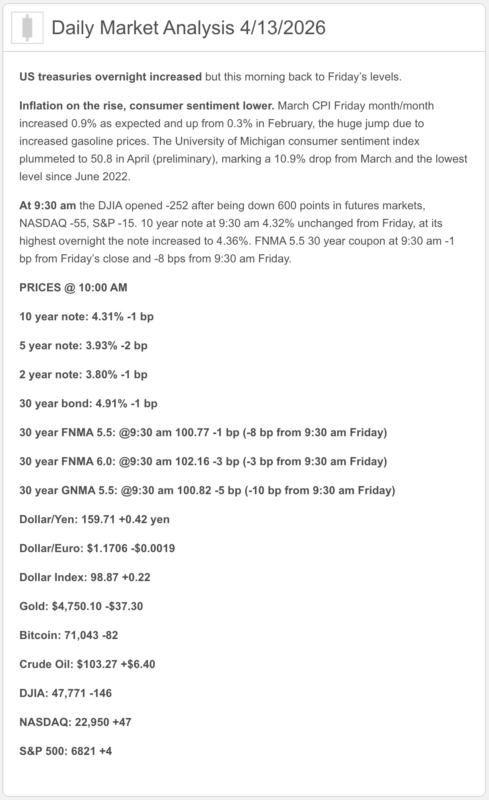

- Inflation is still the ghost at the feast. Friday’s March CPI showed headline inflation up 0.9% month over month and 3.3% year over year, while core CPI rose 0.2% monthly and 2.6% annually. BLS said the jump was led by gasoline, and Reuters reported March was the biggest monthly CPI increase in nearly four years.

- Consumers are not feeling festive. The University of Michigan’s preliminary April sentiment reading fell to a record low 47.6, down from 53.3 in March.

- The Fed is still on hold at 3.50% to 3.75%. The March FOMC statement kept policy unchanged, and the March 17–18 minutes said a cut was not fully priced until December while the probability of rate hikes through early next year rose to about 30%.

- Mortgage rates are a little better than last week, but not exactly relaxed. Freddie Mac’s latest weekly survey shows the 30-year fixed at 6.37% and the 15-year fixed at 5.74%. MBA’s more current survey had the 30-year contract rate at 6.51%, with refis down 2.8% and purchase apps up only 1% week over week, still 7% below last year.

- Housing gave us a fresh reality check this morning. NAR reported March existing-home sales fell 3.6% to a 3.98 million annual pace, inventory rose to 1.36 million, supply increased to 4.1 months, and the median price climbed to $408,800.

1) Market Analysis – What Hit This Morning

There was no major 8:30 a.m. blockbuster on the U.S. calendar today, so the market’s marching orders came from three places: Friday’s hot CPI, today’s Hormuz/blockade escalation, and this morning’s softer March home-sales report. That is a messy combo for rates because housing softness leans bond-friendly, but $100-plus oil and renewed shipping risk lean the other way.

Today’s fresh housing data were a little underwhelming. NAR said March sales fell 3.6% month over month and 1.0% year over year, while inventory improved and affordability slipped from February’s level. Translation: the market is not frozen, but it is still asking buyers to bring a stronger stomach and a bigger calculator.

On the energy side, OPEC cut its second-quarter 2026 global oil demand forecast by 500,000 barrels per day, calling out the Iran war’s effect, while keeping its full-year demand-growth forecast unchanged. That matters because it tells you the market is no longer treating this as a short, tidy headline event.

Narrative you can use:

“Today’s setup is a classic tug-of-war: housing data softened, which normally helps rates, but the fresh Hormuz blockade and oil back above $100 keep inflation nerves alive. For mortgage pricing, energy is still shouting louder than housing.”

2) Market Analysis – Fed Watch

Officially, the Fed is still saying the economy is expanding at a solid pace, inflation remains somewhat elevated, uncertainty is elevated, and policy stays in a 3.50% to 3.75% target range. One notable wrinkle from the March meeting: Stephen Miran dissented in favor of a quarter-point cut, but the Committee held steady.

The more important takeaway was in the minutes. The Fed’s own March 17–18 minutes said the market had pushed out the first fully priced cut to December, and options implied the probability of rate hikes through early next year increased to about 30%. That is not the kind of sentence bond bulls frame and hang over the fireplace.

San Francisco Fed President Mary Daly added last week that the oil shock means getting inflation back to 2% “takes longer,” though she still said policy is in a “good place.” So the Fed is not waving a rate-hike flag today, but it also is not acting like rate cuts are waiting just around the corner with balloons.

3) Market Analysis – Where Mortgage Rates Actually Are

Freddie Mac’s latest consumer benchmark has the 30-year fixed at 6.37% and the 15-year fixed at 5.74%, both a touch better than the prior week. That is the good news.

The more market-sensitive MBA read was 6.51% for the week ended April 3. Refinance applications fell 2.8%, purchase applications rose about 1%, and purchase demand remained 7% lower than a year ago. In other words, the spring market still has a pulse, but it is not exactly sprinting stadium stairs.

The bigger point is that mortgage pricing is still being driven more by Treasury yields, oil, inflation expectations, and geopolitical risk than by abstract conversations about future Fed cuts. With the 10-year back around 4.319% and oil back above $100, the market is not exactly handing out discount points like party favors.

4) Market Analysis – Housing Market Check

NAR’s March report gave us the newest housing snapshot: 3.98 million in existing-home sales annualized, 1.36 million homes on the market, 4.1 months’ supply, and a $408,800 median price. Prices were up 1.4% year over year, marking the 33rd consecutive month of annual price gains.

Affordability dipped slightly in March to 113.7 from 117.5 in February, though it remained well above 104.2 from a year earlier. First-time buyers accounted for 32% of transactions, down from 34% in February. That tells you housing is still accessible for some buyers, but not without friction.

For Western-market conversations, the regional data are useful: the West saw sales fall 1.3% month over month to 770,000, but they were up 1.3% year over year, while the median price was $613,400, down 1.3% from March 2025. NAR also trimmed its 2026 forecast and now expects existing-home sales to rise 4% this year, with new-home sales now expected to be flat.

5) Market Analysis – Political Backdrop & Fed Independence

The biggest political and macro story remains the renewed escalation around the Strait of Hormuz. Reuters reported Monday that the U.S. military blockade of ships leaving Iranian ports had begun, Tehran threatened retaliation against Gulf neighbors’ ports, and about one-fifth of the world’s oil normally moves through the strait. That is not a side story for rates. That is the story.

Reuters also reported Trump acknowledged on Sunday that oil and gasoline prices may remain high into the midterm elections in November, which is an unusually direct political admission that the energy shock could linger. When the White House is effectively saying “yes, this may sting for a while,” the bond market tends to believe the bruise may last longer too.

There is also a second-order political/economic issue here: if energy stays high while sentiment stays weak, Washington’s room for error gets smaller. That does not mean the Fed loses independence. It does mean the Fed’s inflation fight is now happening with a geopolitical backpack full of bricks. That is an inference based on the Fed’s own concern about inflation expectations and international developments, plus Daly’s warning that the oil shock extends the timeline back to 2%.

6) Market Analysis – What This All Means for Rates Going Forward

Base case:

Mortgage rates stay choppy to slightly elevated near term. Housing softened, yes, but oil back above $100, a 10-year around 4.319%, and a Fed that is still worried about inflation expectations do not create a clean recipe for lower mortgage pricing this week.

Better case for rates:

The better path is that the blockade proves temporary, shipping risk eases, oil comes back down, and the market decides March CPI was mostly an energy punch rather than a broad re-acceleration. That view has some support from the softer 0.2% monthly core CPI reading and Daly’s point that the oil shock delays progress rather than automatically requiring fresh hikes.

Worse case for rates:

If Hormuz stays snarled, oil remains above $100, and higher energy costs bleed further into inflation expectations and consumer behavior, the Fed can stay sidelined longer and mortgage rates can remain stubborn in the mid-6s. The Fed minutes already showed a more hawkish market path, and consumer sentiment already fell to a record low.

7) Practical Takeaways

For buyers, this is still a market where structure beats hope. A slightly better survey rate is nice, but it does not offset what higher oil and bond yields can do to daily pricing. Buydowns, concessions, and product choice still matter a lot.

For agents, today’s housing report is useful because it gives you both sides of the argument: inventory is improving, but demand is still rate- and confidence-sensitive. That means realistic pricing and strong financing strategy matter more than motivational speeches and a ring light.

For refi and move-up conversations, the honest message is still not “rates are about to tumble.” The better message is that opportunities still exist, but the window depends on the borrower’s timeline, payment sensitivity, and willingness to act when pricing improves rather than waiting for perfection. That inference is supported by the Fed’s hold stance, the still-elevated mortgage backdrop, and today’s risk-off oil move.

8) Lock vs Float

0–15 days from closing:

I would lean lock. Today’s renewed oil shock and shipping-risk headlines are not the kind of backdrop I would want to gamble against with a near-term closing.

15–30 days:

This is still case by case. If the borrower is tight on DTI or highly payment-sensitive, I would favor protection. If they have room and can handle volatility, there is at least a reasoned case for cautious patience, but not casual optimism.

30+ days:

A cautious float can still make sense, but only with discipline. This market can pivot on one energy headline, one Fed speech, or one inflation-expectation move. Not exactly a hammock-and-lemonade setup.

Stay safe and make today great!