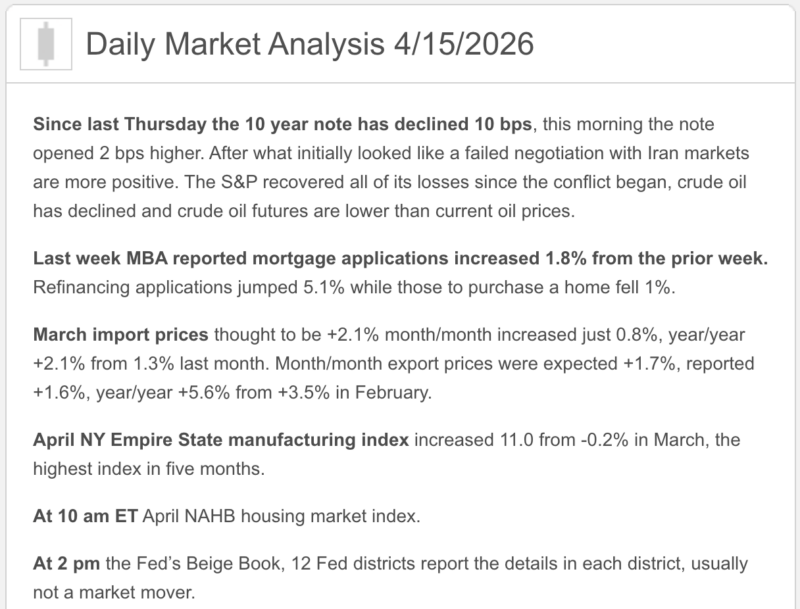

Good Wednesday morning (I am not sure I can say best day of the week on tax day), from your Hometown Lender. Let’s get into today’s market analysis.

Yesterday saw bonds continue to improve through the day on whispers of more ceasefire talks. Bonds are under a little pressure as it is never a straight line down (we have seen it can be a straight line up); however, most rate sheets should be seeing the best pricing we’ve seen in a month or so, with little risk of repricing worse today.

Stocks have rallied and sit near all-time highs once again, as traders remain optimistic that a deal with Iran will soon bring a resolution to the conflict. Both stocks and bonds are increasingly pricing out much of the risk premium that has built up since the conflict started in late February as the US and Iran talk of a second round of negotiations.

President Trump has said that the war is “close to over”. Oil remains below $100 a barrel, which is the lever, and markets are looking ahead to what comes next. It is likely we see bonds improve a bit through the day, wiping out some small early losses.

Market Analysis – From a higher and better view:

Market Analysis – Quick Snapshot

- No retail-sales bomb this morning. The March retail-sales release was pushed back to April 21, so markets had less fresh consumer-demand data than usual to chew on today.

- The main data point was import prices. U.S. import prices rose 0.8% in March after a revised 0.9% gain in February, and were up 2.1% year over year, the biggest annual increase since December 2024. Imported fuel prices rose 2.9%, and import prices excluding food and energy rose 0.6%.

- Stocks are acting pretty calm for a market that has been living on espresso and geopolitics. At 9:57 a.m. ET, the Dow was down 0.22%, the S&P 500 up 0.11%, and the Nasdaq up 0.42% as earnings and renewed U.S.-Iran talk hopes offset some Middle East nerves.

- Oil is lower than the panic highs, but still not exactly cheap. Reuters reported Brent at $95.10 and WTI at $91.91 as talk of renewed negotiations helped, even while U.S. forces continued halting Iran’s sea trade.

- The Fed is still parked at 3.50% to 3.75%, and today’s tone stayed patient. Cleveland Fed President Beth Hammack said rates are likely on hold “for a good while,” while emphasizing the Fed needs to wait and see how the energy shock flows through the economy.

- Mortgage rates remain better than the early-April spike, but still elevated. Freddie Mac’s latest survey shows the 30-year fixed at 6.37% and the 15-year fixed at 5.74%. MBA’s last weekly read had the 30-year contract rate at 6.51%.

- Housing is giving off cautious vibes, not champagne vibes. Builder sentiment fell to 34 in April, a seven-month low, while March existing-home sales were 3.98 million, with 1.36 million homes for sale, 4.1 months’ supply, and a $408,800 median price.

1) Market Analysis – What Hit This Morning

Today’s actual data story was import prices, and it was a little sticky without being a full-blown horror movie. Import prices rose 0.8% in March, below the 2.0% increase economists expected, but the annual rate still climbed to 2.1%, and the core import measure excluding food and energy rose 0.6%. That tells you inflation pressure from abroad is still very much alive, even if today’s number was not as bad as feared.

The other important thing that hit this morning was actually what didn’t hit: retail sales. That release got bumped to April 21, so today’s market had less direct evidence on consumer spending and had to lean more heavily on prices, energy, earnings, and geopolitics. In bond-market terms, that is like trying to judge a football game with only the scoreboard and no game film.

Narrative you can use:

“Today’s inflation signal was still warm, especially on imported goods and fuel, but it was not quite as ugly as feared. The bigger issue is that markets still do not have enough evidence yet to declare the consumer weak enough or inflation cool enough to push mortgage rates meaningfully lower.”

2) Fed Watch

Officially, nothing changed: the Fed’s target range remains 3.50% to 3.75%, and the March statement said the Committee will assess incoming data, the evolving outlook, and the balance of risks. Inflation is still above target, and the Fed is still not in a hurry to act cute.

Today’s live Fed tone stayed patient. Hammack said rates are likely on hold for “a good while” and stressed that the central bank needs to see how long higher energy prices last and how much they bleed into inflation and spending. She also said cuts or hikes remain possible depending on the data, which is central-bank language for “nobody touch anything until we know more.”

There is also a political split-screen around the Fed right now. Treasury Secretary Scott Bessent said the economy will likely grow more slowly this quarter because of the war but should rebound, while also saying current oil prices do not appear to be unanchoring inflation expectations. That is not a full all-clear, but it is a softer tone than the market had feared a week ago.

3) Market Analysis – Where Mortgage Rates Actually Are

Freddie Mac’s latest broad consumer benchmark still shows the 30-year fixed at 6.37% and the 15-year fixed at 5.74% as of April 9. That is down from the early-April spike, which is welcome, but we are still very much in “better than worse” territory, not “welcome back to 2021” territory.

MBA’s more market-sensitive weekly survey had the 30-year contract rate at 6.51% for the week ended April 3, with refinance applications down 2.8% and purchase applications up about 1% week over week but still 7% below a year earlier. So the spring market has a pulse, but it is not exactly sprinting stadium stairs.

The housing-market mood confirms that financing costs still matter. Reuters reported mortgage rates averaged 5.98% in late February, jumped to 6.46% in early April, and averaged 6.37% last week, which has been enough to drag builder confidence to a seven-month low. Mortgage rates are still being pushed around more by energy, inflation, and Treasury psychology than by happy talk about future Fed cuts.

4) Market Analysis – Housing Market Check

The freshest hard housing data still come from Monday’s March existing-home sales report: sales fell 3.6% to a 3.98 million annual pace, inventory rose to 1.36 million, supply increased to 4.1 months, and the median existing-home price rose 1.4% year over year to $408,800. Affordability slipped to 113.7 from 117.5 in February, though it remained better than a year ago.

Today added another housing wrinkle: homebuilder sentiment dropped to 34, a seven-month low and the 24th straight month below 50. Reuters said 62% of builders reported higher material costs and 70% said uncertainty made pricing homes harder. Translation: the resale market is still tight, the new-home market is still stressed, and nobody in housing is confusing this for easy mode.

5) Market Analysis – Political Backdrop & Fed Independence

The biggest macro-political story is still the Iran conflict, but the tone is slightly less panicked than earlier this week. Reuters reported the U.S. has completely halted Iran’s sea trade, yet oil has eased because markets are betting talks could resume and a broader deal may still be possible. That has helped risk appetite, but it has not erased the inflation damage already done.

The other political story that matters for rates is Fed independence. Reuters reported President Trump threatened to fire Jerome Powell from his Board seat if Powell does not leave entirely when his term as Fed chair ends on May 15, while Kevin Warsh’s confirmation hearing is set for April 21. Even if that does not change policy immediately, it adds noise around the central bank at exactly the moment markets are already hypersensitive to inflation and credibility.

6) Market Analysis – What This All Means for Rates Going Forward

Base case: mortgage rates stay choppy but range-bound near term. Import prices were sticky, housing sentiment weakened, oil is off the highs but still elevated, and Fed officials are still talking like patience is the only adult in the room.

Better case for rates: oil keeps drifting lower, U.S.-Iran talks actually resume, and the market decides the worst of the energy shock is behind us. In that setup, inflation fears ease a bit, Treasury yields can calm down, and mortgage pricing gets some breathing room. That is an inference, but it is grounded in the market’s positive reaction to lower oil and renewed diplomacy headlines.

Worse case for rates: talks fail, oil snaps back higher, imported inflation stays firm, and the Fed digs in for even longer. If that happens, mortgage rates likely stay sticky in the mid-6s and the “maybe next week” crowd gets another lesson in patience.

For the forward calendar, the next immediate scheduled data point is industrial production on April 16, while the postponed retail-sales report now lands on April 21. That means tomorrow still matters, but the next big consumer-demand read is later than usual.

7) Practical Takeaways

For buyers, today’s setup still says structure beats hope. Rates are a little off the recent highs, but the market is still one oil headline away from a mood swing. Concessions, buydowns, product choice, and realistic payment planning still matter more than trying to out-guess every macro headline.

For agents, the message is balanced: inventory has improved, but both existing-home sales and builder sentiment say affordability and confidence remain real constraints. The market is moving, just not gracefully. Think brisk walk, not victory lap.

For refi and move-up conversations, the honest message is still not “rates are about to drop fast.” The better message is that opportunities still exist, but they may come in windows tied to oil, Treasury calm, and market sentiment — not because the Fed suddenly starts throwing rate confetti.

8) Lock vs Float

- 0–15 days from closing: I would still lean lock. The market is steadier than earlier in the month, but inflation and geopolitical risk are still too alive for comfort.

- 15–30 days: this is still case by case. If the borrower is tight on DTI or highly payment-sensitive, I would favor protection. If they have room, today’s calmer oil backdrop gives you at least a reasonable case for cautious patience.

- 30+ days: a cautious float can make sense, but only with discipline. This market is trading peace headlines, earnings optimism, and inflation anxiety all at once, which is not exactly a hammock-and-lemonade setup.

Stay safe and make today great!