Good Tuesday morning from your Hometown Lender. Here’s your daily market analysis!

Yesterday was a great day for bonds, with mortgage bonds ending the day quite a bit better through the afternoon. The blockade didn’t lead to any escalation in Iran, and markets have hope that negotiations will continue and a resolution to the conflict will come soon.

Rates will be better than yesterday, as mortgage bonds build on yesterday’s gains. It is very slow progress but nonetheless, improving. It should be a calm day unless something unexpected happens in the Middle East. It’s even possible bonds improve some more through the day.

PPI was released today and while it was the highest in a long time (4+% annually), it was still much below expectations so markets largely ignored it.

Market Analysis – From a higher and better view:

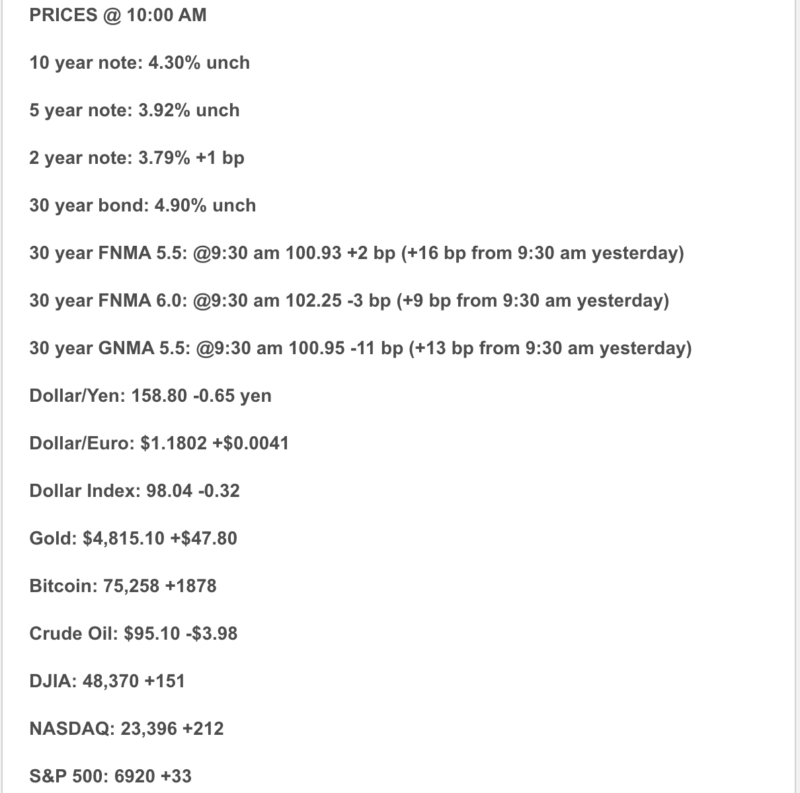

Market Analysis – Quick Snapshot

- Today’s headline is producer inflation, not consumer inflation. March PPI rose 0.5% month over month and 4.0% year over year, the biggest annual increase since February 2023. The cleaner core measure excluding foods, energy, and trade services rose 0.2% for the month and 3.6% year over year.

- Markets are having a better hair day. By late morning, the Dow was up 0.47%, the S&P 500 up 0.58%, and the Nasdaq up 0.98% as hopes for renewed U.S.-Iran talks pushed Brent down to $95.02 and WTI down to $92.60. The 10-year Treasury eased to 4.281%.

- The Fed is still at 3.50% to 3.75%, but today’s Fed chatter was not exactly friendly to quick cuts. Chicago Fed President Austan Goolsbee said cuts could slip into 2027 if high oil prices keep inflation sticky, while Treasury Secretary Scott Bessent said the Fed is “doing the right thing” by waiting and watching.

- Mortgage rates remain a little better than last week, but still not cozy. Freddie Mac’s latest survey has the 30-year fixed at 6.37% and the 15-year fixed at 5.74%.

- Housing and small business both flashed a caution light. March existing-home sales fell to a 3.98 million annual pace, while the NFIB small-business optimism index dropped to 95.8, its lowest level since April 2025.

1) Market Analysis – What Hit This Morning

The main economic release this morning was PPI, and it landed in that awkward middle ground the bond market hates: hot enough to keep inflation concerns alive, but not hot enough to force a full panic. Headline producer prices rose 0.5% in March, while the underlying measure excluding foods, energy, and trade services rose 0.2%. Goods prices did the heavy lifting, rising 1.6%, with energy up 8.5%.

The encouraging part, if you are looking for one with a flashlight, is that services were unchanged in March. Reuters noted that some economists took that as a sign tariff pass-through may be easing a bit. So the report was not soft, but it also was not a full “inflation is back and brought friends” moment.

We also got a second read on business mood, and it was not exactly sparkling. The NFIB Small Business Optimism Index fell 3.0 points to 95.8, below its long-run average of 98.0, while the uncertainty index jumped to 92. That tells you the real economy is still functioning, but confidence is getting pushed around by oil and geopolitics.

Narrative you can use:

“Today’s inflation report showed price pressure is still alive, especially in energy, but the internals were not as ugly as the headline sounds. Markets are trying to balance slightly better inflation texture against the reality that oil and geopolitics can still wreck the party.”

2) Fed Watch

Officially, nothing changed: the Fed’s target range remains 3.50% to 3.75%, and the March FOMC statement said the Committee will keep assessing incoming data, the evolving outlook, and the balance of risks.

Unofficially, today’s tone stayed hawkish by delay. Goolsbee said that before the Iran war he thought multiple cuts in 2026 were plausible, but if inflation does not resume falling, that timeline could get pushed out of this year and potentially into 2027. That is not a formal Fed forecast, but it is a pretty loud reminder that the bar for cuts is still high.

The political wrinkle is interesting too. Treasury Secretary Bessent said the Fed is “doing the right thing by sitting and watching” while the conflict plays out. That is notable because it reinforces a wait-and-see policy stance at the same moment markets are still debating whether oil weakness today is real relief or just a temporary exhale.

3) Market Analysis – Where Mortgage Rates Actually Are

Freddie Mac’s latest weekly survey still shows the 30-year fixed at 6.37% and the 15-year fixed at 5.74%, both slightly improved from the prior week. That is the good news. The less-fun news is that we are still talking mid-6s, not some magical return to borrower nirvana.

For rate watchers, the bigger market signal today is that the 10-year Treasury slipped to 4.281% as oil cooled and equities bounced. That helps at the margin, but yields remain much higher than they were before the late-February war shock because markets still see inflation risk hanging around. Mortgage pricing still cares a lot more about bond yields, oil, and inflation expectations than about optimistic daydreams of near-term Fed cuts.

4) Market Analysis – Housing Market Check

Yesterday’s NAR report is still the best fresh housing read on the board. Existing-home sales fell 3.6% in March to a seasonally adjusted annual rate of 3.98 million, inventory rose to 1.36 million homes, and supply increased to 4.1 months. The median existing-home price rose 1.4% year over year to $408,800, marking 33 straight months of annual price gains.

Affordability slipped from February but is still better than a year ago. NAR’s Housing Affordability Index fell to 113.7 in March from 117.5 in February, but it remained above 104.2 from March 2025. Translation: housing is still expensive, but it is not quite as punishing as last year’s version of the obstacle course.

For Western-market conversations, the regional data are useful. The West saw sales fall 1.3% month over month to 770,000, while the median price was $613,400, down 1.3% from a year earlier. That keeps the conversation nuanced: national prices are still rising, but some Western markets are softer around the edges.

5) Market Analysis – Political Backdrop & Fed Independence

The biggest macro-political driver today is that markets are betting there may still be an off-ramp in the U.S.-Iran conflict. Reuters reported negotiating teams from the U.S. and Iran could return to Islamabad this week, and that hope helped send oil sharply lower even though the port blockade remains in place. That is why stocks are up and crude is down today. Hope is tradable, even when certainty is still on vacation.

That said, the broader risk picture has not disappeared. Reuters reported oil prices had jumped more than 35% since the war began before today’s pullback, and the IMF cut its 2026 global growth forecast to 3.1% from 3.3%, warning that a worse conflict path could drag growth to 2.0%, which it described as recession territory.

Financial firms are feeling the same split-screen. Big banks reported strong trading results from all the volatility, but executives still warned about mounting economic and geopolitical risk. Jamie Dimon said the U.S. economy has remained resilient, but also flagged a more complex risk environment. That is a pretty good summary of the whole market right now: resilient, but definitely not relaxed.

6) Market Analysis – What This All Means for Rates Going Forward

Base case:

Mortgage rates stay choppy but a touch better if oil keeps easing. Today’s PPI was firm, but not disastrous, and lower oil plus a slightly lower 10-year give bonds at least a fighting chance. Still, the Fed is nowhere near comfortable enough to hint at fast cuts.

Better case for rates:

The better path is that U.S.-Iran talks resume, crude keeps falling, and future inflation data confirm that March’s inflation pop was mostly an energy shock rather than a broad re-acceleration. That is an inference, but it is grounded in today’s oil selloff, unchanged services PPI, and the softer underlying producer-price reading.

Worse case for rates:

If today’s diplomacy hopes fade, oil rebounds, and producer inflation feeds through more fully into consumer prices and expectations, the Fed can stay on hold longer and mortgage rates can remain stubbornly in the mid-6s. Goolsbee’s comment that cuts could be pushed into 2027 is the clearest version of that risk.

7) Practical Takeaways

For buyers, this is still a market where strategy matters more than slogans. Slightly lower mortgage rates are helpful, but daily pricing can still get pushed around by oil, bond yields, and headlines. Buydowns, concessions, and smart structure still matter a lot.

For agents, today’s message is balanced: housing is slow, inventory is improving, and affordability is better than a year ago, but sentiment remains fragile. That means realistic pricing, strong pre-approval, and calm client coaching are still doing more work than motivational Instagram captions.

For refi and move-up conversations, the honest message is still not “rates are about to fall fast.” The better message is that windows can open, but they may open because markets get temporary relief on oil and headlines, not because the Fed suddenly turns into a coupon dispenser.

8) Lock vs Float

0–15 days from closing:

I would still lean lock. Today is better, but this market is still one geopolitical headline away from mood swings.

15–30 days:

This is still case by case. If the borrower is tight on DTI or very payment-sensitive, I would favor protection. If they have some room, today’s oil pullback gives a reasonable case for cautious patience.

30+ days:

A cautious float can make sense, but only with discipline. The market is trading hope right now, and hope is not a rate lock.

Stay safe and make today great!