Good Thursday morning from your Hometown Lender. Let’s get today’s market analysis started!

Yesterday bonds started the day a bit weak and ended the day the same way. There was minimal movement. Rates today are roughly the same as yesterday. There is a calm over markets as the war posture has shifted from attacking and defending to choking off revenue. Surprisingly, it’s an effective strategy thus far and markets clearly like it a lot better. Not only are we avoiding missiles, but Iran is being crippled economically, which even if it ended today, would take them months if not years to rebound from.

Additionally, the US is getting the win at home as oil international oil and gas exports are skyrocketing. As long as traders remain optimistic that a resolution is coming with Iran, it is unlikely we will see rates jump.

However, and this is important to note, while we could see some pricing improvement, there isn’t a lot of room for rates to move much lower yet. For that to happen we need to see ship traffic resume normal levels in the Strait of Hormuz and for oil to fall back to February levels.

Market Analysis – From a higher and better view:

Market Analysis – Quick Snapshot

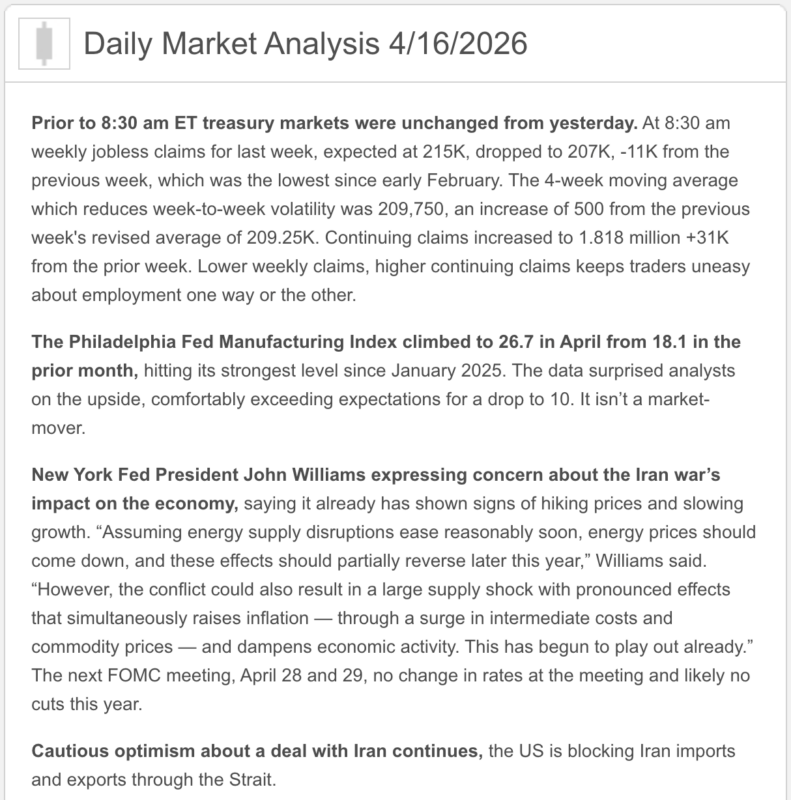

- This morning’s labor read stayed firm. Weekly jobless claims fell to 207,000 from a revised 218,000, while continuing claims rose to 1.818 million. Translation: layoffs still are not breaking higher in a meaningful way, even if hiring is not exactly doing cartwheels.

- Industrial production was soft. Total industrial production fell 0.5% in March, manufacturing dipped 0.1%, and capacity utilization slipped to 75.7%. That is a mild growth caution flag, especially with mining down 1.2% and utilities down 2.3%.

- Regional manufacturing was stronger, but pricier. The Philly Fed’s April general activity index rose to 26.7 from 18.1, new orders jumped to 33.0, but the employment index fell to -5.1 and prices paid climbed to 59.3. In plain English: activity looked better, hiring looked weaker, and inflation still refused to be polite.

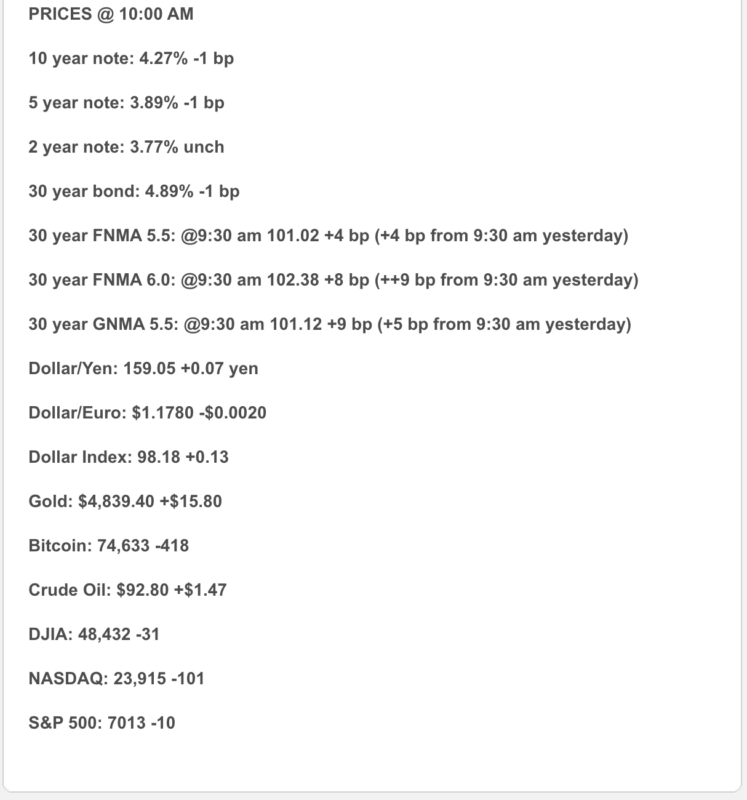

- Markets are a little wobbly after the recent record run. At 10:06 a.m. ET, the Dow was down 0.13%, the S&P 500 down 0.08%, and the Nasdaq down 0.28%. The rally is still alive, but today’s vibe is more “take a breath” than “confetti cannon.”

- Oil is still very much a rate story. Reuters reported Brent at $96.61 and WTI at $92.46 as traders questioned whether renewed U.S.-Iran talks will really fix the Hormuz mess.

- The Fed is still on hold at 3.50% to 3.75%, and officials are not sounding eager to cut. New York Fed President John Williams said the war is already adding to inflation pressure, while St. Louis Fed President Alberto Musalem said core inflation could stay near 3% this year and rates may need to stay unchanged for some time.

- Mortgage rates remain improved from the recent spike, but still elevated. The latest available Freddie Mac weekly survey has the 30-year fixed at 6.37% and the 15-year fixed at 5.74%. MBA’s last weekly survey showed 6.51% on the 30-year contract rate.

1) Market Analysis – What Hit This Morning

Today’s data came in with a very 2026 flavor: stable labor, softer production, and still-uncomfortable pricing pressure. Claims improved to 207,000, which says layoffs remain contained, but industrial production fell 0.5% in March and manufacturing slipped 0.1%, which says the growth engine is still running with a little less swagger.

The Philly Fed report added a twist. Business activity, new orders, and shipments all improved, but employment turned negative and prices paid jumped sharply. That is the kind of report that makes the bond market squint: growth is not collapsing, but inflation pressure is still lurking in the machinery.

Narrative you can use:

“Today’s data were mixed in a way the Fed does not love; layoffs still look low, manufacturing activity improved regionally, but national production softened and price pressure stayed hot. That keeps the economy out of immediate danger, but it also keeps mortgage-rate relief from arriving in any dramatic fashion.”

2) Fed Watch

Officially, nothing changed: the Fed’s target range remains 3.50% to 3.75%. But today’s Fed tone leaned patient-to-hawkish, not dovish. Williams said the war is already lifting inflation pressures and projected inflation of roughly 2.75% to 3.0% this year before returning to target in 2027. He also said growth could run 2.0% to 2.5% and unemployment 4.25% to 4.5%.

Musalem was even more direct. He said high oil prices could keep core inflation near 3% for the rest of 2026, making it more likely that rates stay unchanged for some time, with hikes still possible if inflation expectations become unanchored. That is not exactly the Fed equivalent of “rate cuts coming soon, everyone relax.”

3) Market Analysis – Where Mortgage Rates Actually Are

The latest available Freddie Mac weekly survey still shows the 30-year fixed at 6.37% and the 15-year fixed at 5.74% for the week ending April 9. That was an improvement from the prior week, but we are still very much living in the mid-6s, not the promised land.

MBA’s more market-sensitive survey last showed the average 30-year contract rate at 6.51%, with refinance applications down 2.8% and purchase applications up about 1% week over week but still 7% below last year. So yes, buyers are still shopping, but not exactly like they just found free guacamole.

The bigger point remains the same: mortgage pricing is still being driven more by oil, inflation expectations, and Treasury-market psychology than by wishful talk about future Fed cuts. Today’s data did not do much to change that story.

4) Market Analysis – Housing Market Check

The freshest hard housing data still come from Monday’s March existing-home sales report. Sales fell 3.6% to a seasonally adjusted annual pace of 3.98 million, inventory rose to 1.36 million, supply climbed to 4.1 months, and the median existing-home price rose to $408,800, up 1.4% from a year earlier.

Affordability slipped a bit in March to 113.7 from 117.5 in February, though it remained better than a year ago. In the West, sales fell 1.3% month over month to 770,000, while the median price was $613,400, down 1.3% from March 2025.

Builder sentiment did not exactly send flowers either. NAHB’s Housing Market Index fell to 34 in April, the lowest since September 2025, with current sales conditions at 37, future sales expectations at 42, and buyer traffic at 22. That tells you new construction is still feeling the squeeze from rates, uncertainty, and cost pressure.

5) Market Analysis – Political Backdrop & Fed Independence

The biggest macro-political backdrop is still the Iran war and the choke point around Hormuz. Reuters reported that roughly 20% of global oil and LNG flow has been disrupted, and even with more talk of negotiations, traders remain unconvinced that diplomacy will quickly normalize supply. That is why oil is still elevated enough to matter for inflation and mortgage pricing.

There is also a domestic political layer that matters more than usual right now. Reuters reported Trump is doing an economic reset push in Nevada and Arizona while Republicans worry that high gas prices and affordability pressure are hurting the party’s economic message ahead of the midterms. That does not directly set mortgage rates, but it does raise the odds that fiscal and Fed politics stay loud.

And then there is the Powell situation. Reuters reported Trump has threatened to fire Jerome Powell from the Fed Board if he does not leave after his chair term ends on May 15, while Kevin Warsh’s confirmation remains uncertain ahead of his April 21 hearing. Markets do not generally love it when central-bank independence becomes a reality show plotline.

6) Market Analysis – What This All Means for Rates Going Forward

Base case:

Mortgage rates stay choppy and relatively elevated. Claims are still low, regional factory activity improved, oil is still high enough to keep inflation pressure alive, and Fed officials are still talking like patience is mandatory.

Better case for rates:

The better path is that U.S.-Iran talks actually turn into something real, oil eases further, and the softer national production data start to matter more than the inflation fears. In that setup, bond yields can calm down and mortgage pricing can improve a little more. That is an inference, but it is grounded in the market’s recent sensitivity to oil and diplomatic headlines.

Worse case for rates:

If oil stays sticky, supply disruptions linger, and the price pressure showing up in surveys starts bleeding further into headline and core inflation, the Fed likely stays sidelined longer and mortgage rates remain stuck in the mid-6s. Musalem’s and Williams’s comments are basically flashing that risk in bold.

7) Market Analysis – Practical Takeaways

For buyers, this is still a market where structure beats hope. A good strategy with concessions, buydowns, and product choice still matters more than waiting for some magical macro headline to save the monthly payment.

For agents, today’s setup says the market is still active, but confidence is fragile. Existing-home sales are softer, builder sentiment is weak, and rates remain high enough that affordability is still the main character.

For refi and move-up conversations, the honest message is still not “rates are about to tumble.” The better message is that windows can open, but they are likely to open because oil calms down and bond markets exhale, not because the Fed suddenly starts handing out gifts.

8) Lock vs Float

0–15 days from closing:

I would still lean lock. Too many moving parts are still active, and today’s data were not clean enough to justify bravery for the sake of bravery.

15–30 days:

This is still case by case. If the borrower is tight on DTI or very payment-sensitive, I would still favor protection. If they have room, there is at least a reasoned case for cautious patience if oil continues to cool.

30+ days:

A cautious float can make sense, but only with discipline. This market is still trading geopolitics, inflation, and Fed credibility at the same time, which is not exactly a hammock-and-lemonade environment.

Stay safe and make today great!