Good Monday Morning from your Hometown Lender,

This is the week after (the Fed cut) and markets are still guessing on what comes next.

We have two more Fed meetings before the end of the year and predictions from the Fed are all over the place. Some members are predicting no more cuts and at least one is predicting two more 50bos cuts. The dot plot graph, which sets expectations for the future, seems a bit more erratic in the short term. As a result, markets are taking a twostep approach. Investors have decided that the Fed will be much more dovish than it says. And the effect is to push down the cost of short-term borrowing as traders anticipate lower rates, while pushing up the cost of longer-term borrowing as investors prepare for the resulting stronger economy to pressure inflation. That last piece is the kernel on why mortgage rates have not improved. We do have some data this week, the Fed’s favorite inflation gauge (PCE) late there week, and we do hear from the conductor, Chairman Powell as well. For now, rates are range bound but we may not see them fall until there is a clear expectation on the Fed’s next moves.

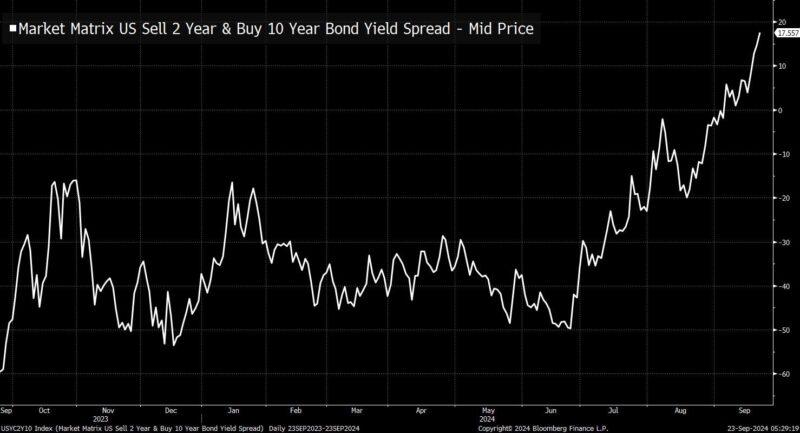

Bloomberg shared the 2-10 spread continues to steepen. Here’s a chart of the 2-10 spread.

The 10-year yield has gone up a touch since the Fed decision last week,

And what’s important to remember is that this is perfectly consistent with Fed easing. Some people get confused by this. They think the Fed easing and lower rates are synonymous. But to some extent this is a misconception. The simplest thing to think about it is that if we had some kind of massive shock tomorrow, harming the economy, you’d almost certainly expect the 10-year yield to collapse. Or think about the 2010s, after the Great Financial Crisis. Inflation was very mild. Employment growth was mediocre, and rates fell through most of the decade. Just going on the economic targets alone, the implication is that for many of those years, the Fed was too tight. And that’s why yields at the long end of the curve kept falling.

Anyway, it’ll be a decent week for economic data.

Nothing too massive. But today we get the S&P Services and Manufacturing PMIs. Tomorrow, we get Philly Fed Non-Manufacturing, Richmond Fed, and the Conference Board confidence data. Later this week we’ll also get Initial Jobless Claims, the latest reading of Q2 GDP, and then also Core PCE, which we know matters a lot to the Fed. Should be another interesting week.

Stay safe and first make today great!