Good Monday AM from your Hometown Lender. Let’s dig into today’s market analysis!

Friday was a pretty good day for rates, with mortgage bonds having a pretty calm day. The outlook heading into the weekend was cloudy though, with the main dominating force continuing to be the peace talks with Iran and the opening of the Strait of Hormuz. Rate sheets today will lose some ground, basically giving back Friday’s gains. The day has started off with a lot of early volatility for mortgage bonds, but I expect to see that settle out. The early trades are due to what happened over the weekend, more specifically the fact that President Trump quickly rejected Iran’s counteroffer to a US peace proposal.

As optimism of a deal swings back and forth, so do bonds, and we can expect more of the back-and-forth until a deal is done. Trying to keep a pulse on how the talks are going is pointless though, as both sides play their cards close to the vest and it always sounds like talks are two steps away from falling apart. Although both sides try to sound like they can do this forever, the reality is that there is pain on both sides, causing both sides to want to get a deal done. Tomorrow morning brings CPI inflation data, before rate sheets come out, and if anything that isn’t the conflict with Iran has a chance to move rate sheets a bit it’s that.

Market Analysis – From a higher and better view:

Market Analysis – Quick Snapshot

- Today’s market is mostly an oil story. U.S.-Iran talks stalled again, Wall Street paused after its recent run, and rising crude is putting fresh pressure on yields and inflation expectations. Reuters reported the S&P 500 and Nasdaq were still near records, while oil rose nearly 3% and stocks traded more cautiously Monday morning.

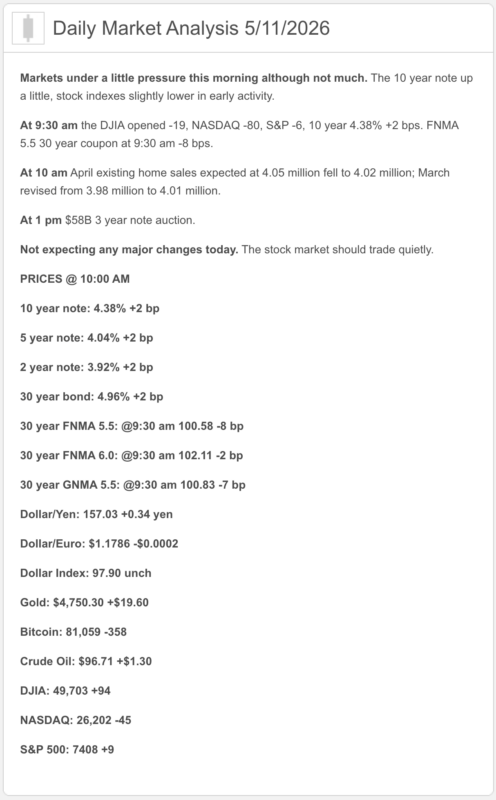

- The 10-year Treasury is back near 4.39%. WSJ reported the 10-year yield rose to 4.386% as the market reacted to the geopolitical setback and renewed inflation worries.

- Mortgage rates are still in the mid-6s. Freddie Mac’s latest weekly survey shows the 30-year fixed at 6.37% and the 15-year fixed at 5.72% as of May 7.

- Housing is still moving, but slowly. Reuters reported existing-home sales rose just 0.2% in April to a 4.02 million annual pace, below expectations, while the median price rose 0.9% to $417,700 and inventory increased to 1.47 million homes.

- The Fed-cut timeline keeps getting pushed back. Reuters reported today that Bank of America now expects no Fed cuts in 2026, while Goldman Sachs pushed its first expected cut to December 2026 after stronger jobs data and persistent inflation risk.

- Tomorrow matters. The BLS schedule shows the April CPI report is due Tuesday, May 12 at 8:30 a.m. ET, which is the next big macro checkpoint for bonds and mortgage pricing.

1) Market Analysis – What Hit This Morning

There was no giant domestic data bomb this morning. The fresh U.S. read was existing-home sales, and it basically said the spring market is still inching forward, not sprinting. Higher mortgage rates and still-tight affordability kept the gain modest, even though inventory improved.

Narrative you can use:

“Today’s market is being driven more by oil and geopolitics than by domestic data. Housing is still moving, but slowly, and as long as crude stays elevated, mortgage-rate relief is going to stay on a short leash.”

2) Fed Watch

The Fed is still in hold mode, but the Street is sounding more “later for longer” every day. Reuters reported today that BofA now expects no cuts this year, and Goldman pushed its expected first cut from September to December. That is not the market getting ready for easy money. That is the market slowly putting the rate-cut party on next year’s calendar.

3) Market Analysis – Where Mortgage Rates Actually Are

Freddie Mac’s latest weekly benchmark is 6.37% on the 30-year fixed and 5.72% on the 15-year fixed. That is up from the prior week and keeps mortgage pricing firmly in the “better than the worst, but still not comfortable” zone.

The bigger issue is that mortgage pricing is still reacting more to oil, yields, and inflation expectations than to hopeful chatter about future Fed cuts. Today’s higher crude and firmer Treasury yields are a reminder that the market still bruises easily.

4) Market Analysis – Housing Market Check

April existing-home sales were 4.02 million annualized, up just 0.2% month over month. Inventory rose 5.8% to 1.47 million, the median price climbed to $417,700, and homes took about 32 days to sell. First-time buyers slipped to 33% of purchases.

Translation: inventory is improving a bit, but affordability is still doing plenty of damage. The market is alive. It is just still walking with a noticeable limp.

5) Political Backdrop & Fed Independence

The macro story is still the Strait of Hormuz. Reuters reported Trump called Iran’s latest response to the U.S. peace proposal “totally unacceptable,” which pushed oil higher and kept the ceasefire on what Reuters described as “life support.”

That matters because roughly one-fifth of global oil normally moves through Hormuz, and Reuters reported tanker traffic remains drastically reduced. In other words, this is not just foreign-policy wallpaper. It is directly tied to inflation, yields, and mortgage pricing.

6) Market Analysis – What This All Means for Rates Going Forward

Base case: mortgage rates stay choppy and a little vulnerable. Higher oil, firmer yields, and a Fed that is getting less dovish give bonds very little room to celebrate.

Better case: diplomacy revives, crude cools off, and tomorrow’s CPI does not confirm a new inflation flare-up.

Worse case: talks stay stuck, oil keeps climbing, and CPI comes in hot enough to push the first cut even farther out. That is how mid-6s mortgage rates stick around like an unwanted houseguest.

7) Practical Takeaways of Market Analysis

For buyers, this is still a market where structure beats hope. Rates are not disastrous, but they are high enough that payment strategy still matters a lot.

For agents and partners, today’s message is simple: housing is still moving, but it is not getting much help from the macro backdrop. Oil and inflation are still the loudest voices in the room.

8) Lock vs Float

0–15 days: lean lock.

15–30 days: case by case.

30+ days: cautious float, but only if the borrower can handle headline-driven swings. Tues CPI is a real volatility point.

Stay safe and make today great!!!