Good morning on this best day of the week Wednesday from your Hometown Lender! Let’s dive into today’s market analysis.

Yesterday was another brutal day for bonds, with rates hitting the highest levels since last July. Bonds were all over the place through the day, dipping to the worst levels in the late morning before fighting to recover through the early afternoon, only to have it all apart again and end the day.

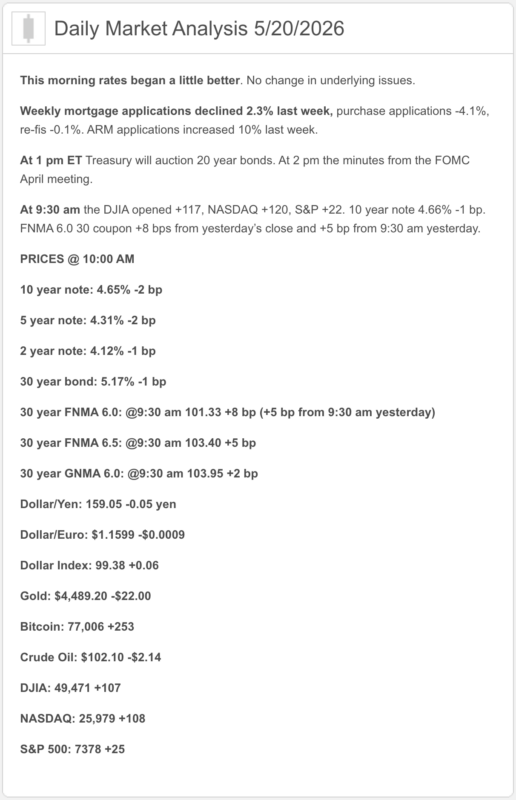

Rates are improving today on news that a deal in the middle east is close. Oil is below 100/barrel. We will take this small win. The minutes from last month’s Fed meeting come out at 11am. I don’t anticipate they will have much effect on bonds, but it is something to be cautious about.

Market Analysis – From a higher and better view:

Market Analysis – Quick Snapshot

- No major U.S. economic release is driving the bus this morning. The market is trading oil, bond yields, Nvidia earnings tonight, and Fed minutes later today more than fresh macro data. At 9:51 a.m. ET, the Dow was up 0.07%, the S&P 500 up 0.25%, and the Nasdaq up 0.43%.

- Treasury yields backed off a bit, but they are still elevated. Reuters said the 10-year yield eased to 4.651% on Wednesday after touching a 16-month high of 4.687% on Tuesday, while a separate Reuters market report noted investors still see a 48.6% chance of a Fed hike in December.

- Oil finally took a breather. Brent fell to about $106.52 and WTI to about $99.93 after Trump said U.S.-Iran negotiations are in the “final stages,” though Reuters noted flows through Hormuz remain far below normal and ADNOC expects it could take at least four months to restore 80% of pre-conflict flows.

- Mortgage rates moved the wrong way. MBA reported the average 30-year fixed mortgage rate rose to 6.56% for the week ended May 15, the highest in seven weeks, while mortgage applications fell 2.3% and adjustable-rate loans approached 10% of applications. Freddie Mac’s latest weekly survey still shows the broader benchmark at 6.36% for the 30-year fixed and 5.71% for the 15-year as of May 14.

- Housing still looks muted. Lowe’s said the U.S. housing market remains subdued, flagged higher transportation and input costs tied to elevated oil prices, and maintained its annual outlook while describing a more cautious lower-income consumer.

- The Fed backdrop is still hawkish and messy. The federal funds target range remains 3.50% to 3.75%, and Reuters says the April 28–29 Fed minutes due later today are expected to highlight the sharp internal divisions from the Fed’s most split decision in decades.

1) Market Analysis – What Hit This Morning

Today’s real market message is less about fresh domestic data and more about relief versus reality. Relief: oil is down sharply on renewed talk of a U.S.-Iran deal. Reality: yields are still high, mortgage rates just jumped in the MBA survey, and supply disruption in Hormuz is still far from resolved. Basically, the market got a better headline but not a full clean-up crew.

Narrative you can use:

“Today’s rate backdrop is a little friendlier because oil pulled back, but not friendly enough to declare victory. Mortgage rates are still reacting more to inflation and geopolitical risk than to any clear sign of easier policy.”

2) Fed Watch

The Fed is still officially on hold at 3.50% to 3.75%. Today’s focus is the April meeting minutes, which Reuters says are expected to show the sharp policy split that ended Powell’s final full meeting as chair, including four dissenting votes, the most since 1992.

The market is no longer asking, “When do cuts start?” It is asking whether the next move could actually be up if oil-driven inflation sticks. Reuters noted traders now see about a 48.6% chance of a December hike. That is not exactly the Fed fan club handing out gift cards.

3) Market Analysis – Where Mortgage Rates Actually Are

The latest Freddie Mac benchmark is 6.36% on the 30-year fixed and 5.71% on the 15-year fixed. That is only slightly better than last week and still leaves borrowers living in the mid-6s.

The more current MBA read is less cheerful: 6.56% on the average 30-year fixed, applications down 2.3%, and almost 10% of borrowers opting for ARMs because they were about 80 bps cheaper. Translation: affordability is still tight enough that borrowers are shopping for workarounds, not champagne.

4) Market Analysis – Housing Market Check

There was no major fresh housing data release today, but the housing tone is still clear. Lowe’s joined Home Depot in saying the U.S. housing market remains muted, even as Pro demand held up better than DIY activity.

Lowe’s also said higher oil is feeding transportation and material costs, which is a very mortgage-market sentence if there ever was one.

That lines up with the recent spring picture: the housing market is still functioning, but it is rate-sensitive, cost-sensitive, and confidence-sensitive.

Alive, yes. Limber, not exactly.

5) Market Analysis – Political Backdrop & Fed Independence

The macro story is still the Iran war and the Strait of Hormuz. Trump said negotiations are in the “final stages,” which helped oil today, but also warned that the alternative could get “a little bit nasty.” Reuters noted only three supertankers were crossing Hormuz Wednesday and that traffic remains far below the roughly 130 ships a day seen before the war.

The Fed-independence story is still live, too. Reuters reported central bankers abroad are uneasy about Kevin Warsh’s comments suggesting Fed independence may not fully extend to broader crisis-fighting operations beyond rate setting. Markets are now pricing not just the inflation problem, but what kind of Fed will be dealing with it.

6) What This All Means for Rates Going Forward

Base case: mortgage rates stay choppy and somewhat elevated. Oil easing helps, but high yields and rising mortgage rates say the bond market is not ready to relax.

Better case: a real deal with Iran gains traction, more ships move through Hormuz, oil keeps falling, and the Fed minutes do not add fresh hawkish fuel.

Worse case: talks stall again, supply stays constrained, oil snaps back up, and the market leans harder into the idea that the next Fed move is a hike, not a cut. That is how mid-6s mortgage rates keep hanging around like an unwanted houseguest.

7) Practical Takeaways

For buyers, this is still a market where structure beats hope. The rate backdrop is not catastrophic, but it is jumpy enough that strategy matters more than trying to time the perfect headline.

For agents and partners, today’s message is straightforward: lower oil helps, but the bigger rate story is still inflation risk, elevated Treasury yields, and a housing market that remains cautious underneath the surface.

8) Lock vs Float

- 30+ days: cautious float, but only if the borrower can handle headline-driven swings. Oil is quieter today, but it is still the loudest person at the table.

- 0–15 days: lean lock.

- 15–30 days: case by case.

Stay safe and make today great!