Good Friday morning from your Hometown Lender. Here is Fri’s market analysis!

Yesterday saw bonds improved through the early afternoon, before giving back the gains by the day’s end. Overall though it wasn’t a bad day.

Rate outlook for today…

Things seem to be calming down in the Middle East, and oil prices are creeping lower. Rate sheets today will be similar to yesterday, which actually were better than expected. Reprice risk on the day is low, it’s a summer Friday which means trading desks will be empty. Not a bad idea to consider locking some loans for protection, but the outlook isn’t bad at the moment.

Market Analysis – From a higher and better view:

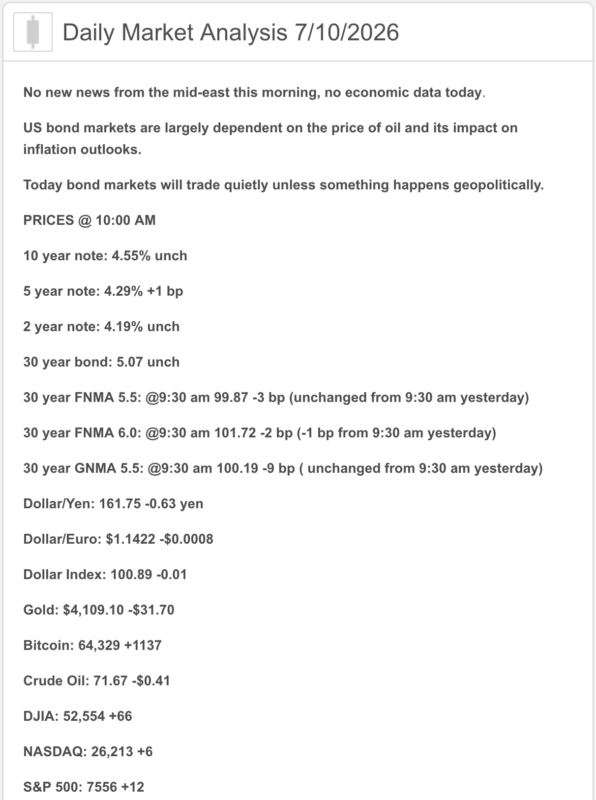

Market Analysis – Quick Snapshot

- Bonds: The 10-year Treasury is hovering around 4.60% after this week’s selloff, as renewed oil and inflation concerns keep pressure on longer-term yields. Bonds are not panicking — but they have definitely canceled casual Friday.

- Mortgage Rates: Daily tracking shows the 30-year fixed around 6.57% and the 15-year fixed around 5.92%. Freddie Mac’s latest weekly survey showed the 30-year fixed at 6.49% and the 15-year fixed at 5.82%.

- Fed Watch: Fed officials remain divided between holding rates steady and hiking again if inflation fails to cool. The next CPI report and Chair Kevin Warsh’s upcoming congressional testimony will be major market events.

- Housing: Existing-home sales fell 2.4% in June while prices reached a record high. Buyers are still present, but elevated rates and affordability are clearly limiting demand.

- Oil / Geopolitics: Renewed U.S.–Iran tensions are keeping oil prices volatile and inflation risk elevated. Apparently, mortgage pricing now requires equal parts economics, foreign policy, and caffeine.

- Politics: A major housing-affordability bill is set to become law without the president’s signature after a political dispute over voter-ID legislation. Housing policy is moving forward — just not quietly.

Market Analysis – What It Means

Today’s tone remains cautious. Higher Treasury yields, geopolitical risk, and persistent inflation concerns are keeping mortgage rates in the mid-6s.

In plain English: the market is functioning, but affordability still needs a strategy.

Market Analysis – Housing & Mortgage Strategy

This remains a structure-the-payment market.

The best conversations right now are about:

Seller credits, temporary buydowns, permanent buydowns, builder incentives, ARM options where appropriate, and a realistic refinance plan if rates improve later.

Buyers are not gone — they are doing math. Sellers and builders who help solve the monthly payment problem have the best chance of turning interest into contracts.

Lock vs. Float

- Lock bias: If closing within 30 days, the borrower is payment-sensitive, or the file is tight, locking remains the cleaner recommendation.

- Float bias: Floating may make sense only with time, flexibility, and a clear trigger. Oil headlines, CPI, and Fed commentary can still move bonds quickly.

Today’s guidance: Bias toward locking short-term closings. For longer timelines, cautious floating may be reasonable only with a defined risk ceiling and daily monitoring.

Stay safe and make today great!