Good Thursday am from your Hometown Lender! Let’s dive into today’s market analysis.

Yesterday saw bonds improve through the morning but then drift lower through the afternoon as concerns increased that there would be continued military strikes in the Middle East. It wasn’t a sharp sell off, but it was enough to feel some pain.

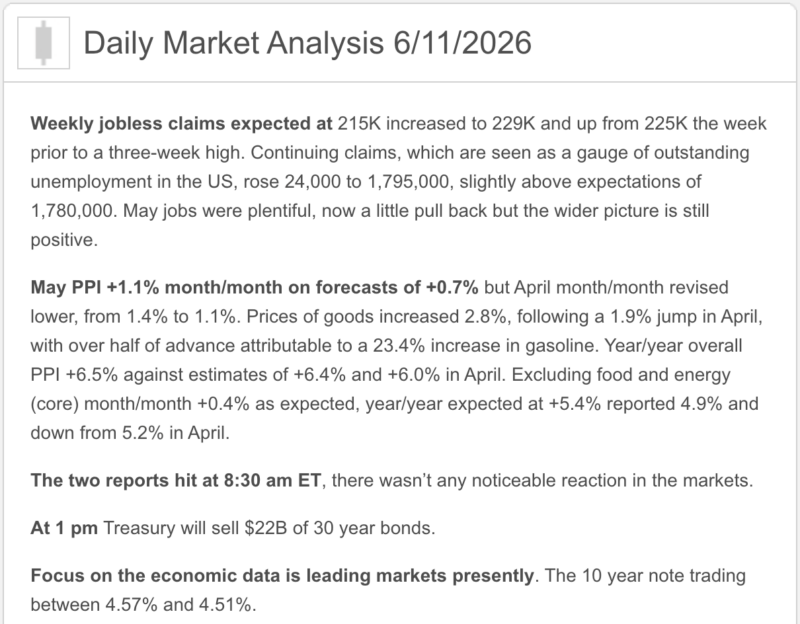

Rates today likely to be slightly worse than yesterday, despite bonds being up a few basis points at the moment. Mortgage bonds lost ground when the PPI wholesale inflation data came out, mainly due to the headline reading increasing 6.5% from a year earlier, with that being the most since November 2022.

Although the producer price index doesn’t have the same sway over markets as the consumer price index, eventually wholesale inflation will become consumer inflation if it is high enough. However, the good news is that mortgage bonds recovered in the 30 minutes after the data came out, and are sitting back at the same levels they were at before the data… up a few basis points but still worse than when pricing came out yesterday.

Other headlines to watch, although not yet seeming to play much of a role in mortgage bonds, is that the European Central Bank (ECB) hiked its policy rate today, the first central bank to do so since the Iran conflict. They are trying to stay ahead of inflation that is being caused by energy prices. This is just an interesting tidbit, but has no real effect on our bonds. What does though is the headlines coming out of the Middle East.

President Trump is threatening to continue strikes on Iran, effectively nullifying the cease fire if followed through on and is also threatening to take control of Kharg Island, Iran’s main oil export hub. Oil is up a couple bucks a barrel, but markets don’t yet seem panicked about this whole thing. But… if we DO see military action increase, it will likely pressure bonds further, as oil prices rise. Right now though, markets don’t seem convinced that it will happen, as oil stays near recent lows and bonds improve to start the day.

Market Analysis – From a higher and better view:

Market Analysis – Quick Snapshot

Bonds: The 10-year Treasury is still hovering in the mid-4.5% range as markets digest hot wholesale inflation, slightly softer jobless claims, and ongoing U.S.–Iran oil risk. Bonds are trying to stay calm, but the inflation data keeps tapping them on the shoulder.

Mortgage Rates: Freddie Mac’s latest weekly survey shows the 30-year fixed at 6.52% and the 15-year fixed at 5.84%. Daily tracking shows the 30-year fixed around 6.55% and the 15-year fixed around 5.92%.

Inflation: May PPI rose 1.1% month over month and 6.5% year over year, driven heavily by energy. Final demand goods jumped 2.8%, the largest monthly increase since the series began in 2009, with gasoline up 23.4%.

Labor: Initial jobless claims rose to 229,000, suggesting the labor market may be cooling at the edges — but not enough to offset the inflation concern.

Fed Watch: The Fed is still expected to hold rates steady at next week’s meeting, but sticky inflation and strong recent jobs data keep the “higher for longer” conversation very much alive.

Politics / Geopolitics: Oil remains a major market driver as investors weigh U.S.–Iran escalation risk and possible Strait of Hormuz disruptions. In 2026, apparently every mortgage rate sheet now needs a foreign policy minor.

Market Analysis – What It Means

Today’s data reinforces the same theme: inflation is still too hot for the Fed to comfortably cut, while the labor market is softening only modestly. That combination keeps Treasury yields elevated and mortgage rates choppy in the mid-6% range.

In plain English: the market is not broken, but it is not handing out easy payments either.

Market Analysis – Housing & Mortgage Strategy

Buyers are still active, but they are payment-sensitive. This remains a structure-the-payment market.

The best conversations right now are about:

Seller credits, temporary buydowns, permanent buydowns, ARM options where appropriate, and a realistic refinance plan if rates improve later.

Sellers and builders who help solve the monthly payment problem have the best chance of turning interest into contracts.

Lock vs. Float

Lock bias: If closing within 30 days, the borrower is payment-sensitive, or the file is tight, locking is still the cleaner recommendation.

Float bias: Floating only makes sense with time, flexibility, and a clear trigger. With hot PPI, oil risk, and the Fed still cautious, floating without a plan is not strategy

Stay safe and make today great!