Good Thursday morning from your Hometown Lender. Here’s is your market analysis for Thursday!

Lots to unpack. Rates improved yesterday early on and then gave back most of the improvement. The trend this week has been a slow grind to better rates. As the adage goes, rates take the elevator up and the stairs down. Trades are being pushed one way or another by the next headline. Last night President Trump spoke for about 20 minutes. I thought he did a good job (regardless your position on the war). He identified the objective and did not over promise on the timing. Foreign markets were rattled by the speech.

When the US markets opened, things were calmer. Since the speech, Iran is pumping out messages on both sides of their mouth. Willingness to have a resolution in the Strait of Hormuz and threats of what will happen if we attack (which is different than threatening to attack). This seems to be a big change and to me, makes me think they are gasping for air, and this is likely over soon. The outcome is Iran likely gets to keep whatever regime is in place now, has no military to speak of, and gets paid to let ships through the Strait allowing them to pay to rebuild their military and terrorist cells.

Markets will cheer and rates will normalize but, we may have just kicked the can down the road for a bit. The ideology hasn’t changed. Tomorrow is a big data day with the jobs report. It is never a good idea to float into it.

Market Analysis – From a higher and better view:

Thursday, April 2, 2026 | Low layoffs, wider trade gap, hotter oil, and rates still wearing their stress face

🚀 Market Analysis – Quick Snapshot

- Fed: The Fed’s target range is still 3.50% to 3.75% after the March 18 meeting. The official statement said growth is still solid, job gains have remained low, and inflation remains somewhat elevated. Powell then said the Fed can “wait and see” how the war-driven energy shock affects inflation, and New York Fed President John Williams said policy is well positioned for these unusual circumstances.

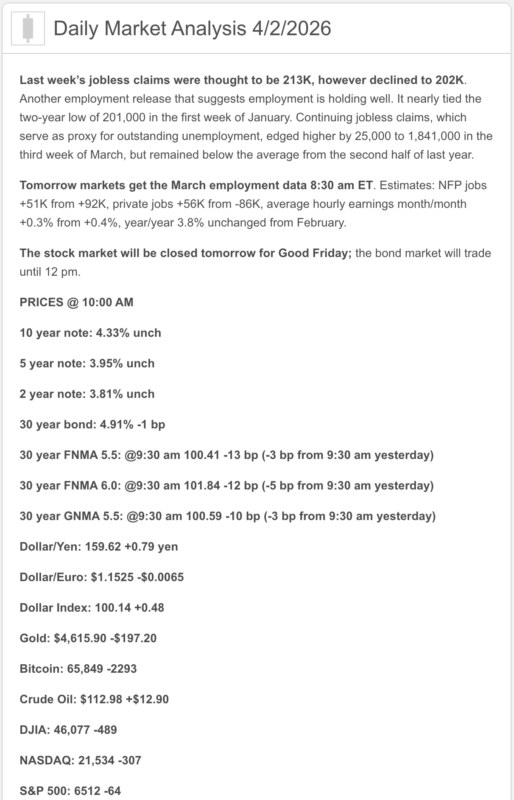

- Labor: Weekly jobless claims fell to 202,000, below expectations, but continuing claims rose to 1.841 million. JOLTS earlier this week showed February job openings at 6.882 million and hiring down to 4.8 million, which keeps the “low hire, low fire” story very much alive.

- Mortgage rates: The latest official Freddie Mac survey still shows 6.38% for the 30-year fixed and 5.75% for the 15-year fixed as of March 26. The more real-time MBA survey yesterday showed the average 30-year contract rate up to 6.57%, the highest since August.

- Housing: Existing home sales were running at a 4.09 million annual pace in February, pending sales rose 1.8%, but new home sales fell to 587,000 in January. Builder sentiment is still subdued at 38, with 37% of builders cutting prices and 64% using incentives in March.

- Big drivers today: lower claims, a wider trade deficit, rising yields, a fresh oil spike, and a Fed that still sounds patient rather than eager to cut.

The big takeaway:

Today’s setup is not screaming recession, but it is also not giving mortgage bonds much relief. Layoffs still look low, but hiring is weak, trade looks like a Q1 GDP drag, oil just shot back above $109, and markets are again pricing a more stubborn inflation backdrop. That is not exactly a spa day for rates.

🎯 Market Analysis –What Hit This Morning?

The hard data this morning was mostly labor and trade. Initial jobless claims fell to 202,000 for the week ended March 28, the four-week average fell to 207,750, and continuing claims rose to 1.841 million. That says layoffs remain low, but hiring is not exactly bursting with enthusiasm either.

At the same time, the U.S. trade deficit widened 4.9% in February to $57.3 billion. Imports rose to $372.1 billion and exports rose to a record $314.8 billion. The real goods deficit also widened to $83.5 billion, which Reuters noted could keep trade on track to subtract from first-quarter GDP.

Markets cared at least as much about geopolitics as they did about the data. Reuters’ market wrap showed Brent jumping above $109, WTI around $109–$113, and the 10-year Treasury yield up around 4.376% after Trump said attacks on Iran would continue for another two to three weeks.

Translation:

The labor market is still standing, but the inflation and oil side of the equation is louder today than the “cooling economy” side. Mortgage pricing hears that first.

🏦 Fed Watch

The Fed has not changed policy since March 18, and the official message is still essentially: growth okay, labor softer, inflation still too warm. Powell said this week the Fed can wait and see how the war affects inflation, and Williams said policy is well positioned for the unusual mix of geopolitical shock and energy-driven inflation risk.

That matters because the market backdrop has become much less friendly for near-term cuts. Rising oil, firmer yields, and higher inflation expectations have pushed investors back toward a higher-for-longer mindset, even though some economists still expect the first cut later this year rather than sooner.

Plain English:

The Fed is not looking for an excuse to help rates right now. It is looking for a reason not to make an inflation mistake.

📈 Where Mortgage Rates Actually Are

The latest official Freddie Mac weekly survey, which is still the cleanest benchmark for client conversations, shows the 30-year fixed at 6.38% and the 15-year fixed at 5.75% as of March 26.

The more real-time read from MBA is less friendly: 6.57% on the average 30-year fixed for the week ended March 27, up 14 basis points on the week and up 48 basis points since February 28. Refi applications fell 17.3% and purchase apps slipped 2.6%.

Real-world takeaway:

Rates had started to feel better earlier in March, then oil and Treasury yields walked back into the room and flipped the table.

🏠 Market Analysis –Housing Market Check

The good news:

- Existing home sales rose 1.7% in February to a 4.09 million annual pace.

- Pending home sales rose 1.8% in February, with gains in the South, West, and Midwest.

- Inventory has been improving enough that MBA’s chief economist said many markets are looking more like a buyer’s market than they have in some time.

The not-as-fun news:

- New home sales fell 17.6% in January to 587,000, near a three-and-a-half-year low.

- Builder sentiment was only 38 in March, still well below the neutral 50 line.

- Builders are still leaning hard on incentives: 37% cut prices and 64% used incentives in March.

What that means:

Housing is still functioning, but it is extremely payment-sensitive. More supply is helping, but higher rates are still the bouncer at the door checking everyone’s wallet.

🌍 Market Analysis –Political + Global Market Backdrop

The political backdrop is doing real market damage, not just making cable news louder. In his Wednesday night address, Trump said U.S. war goals in Iran were nearly complete, but gave no timeline for ending the war and said attacks would intensify over the next two to three weeks. Reuters reported that this erased hopes for a quick resolution and sent oil sharply higher again.

There is also still a trade-policy inflation layer underneath all this. Reuters reported today that the Supreme Court had struck down Trump’s earlier broad tariffs, after which Trump imposed a temporary global tariff for up to 150 days. Between tariffs, shipping restrictions, and higher energy costs, markets have plenty of reasons to stay suspicious about inflation.

Why that matters:

Mortgage rates do not need a fresh inflation report every day to move higher. Sometimes oil, war, tariffs, and one presidential speech do the job just fine.

🔮 What This Means for Rates Going Forward

Base Case

My base case is that rates stay choppy to slightly elevated near term. Low claims keep recession fear from taking over, while higher oil and higher yields keep inflation anxiety alive. That mix is not ideal for a clean mortgage rally. This is an inference based on today’s labor, trade, mortgage-rate, and market data.

Best Case

The friendlier path for rates would be a softer jobs report tomorrow, calmer oil, and fresh signs that the Iran situation is de-escalating. That would give the bond market room to breathe. This is an inference based on how yields and mortgage rates have been reacting to labor softness versus oil headlines.

Worst Case

The uglier path is straightforward: payrolls hold up, oil stays elevated, inflation expectations drift higher, and the Fed keeps sounding patient. In that setup, mortgage rates likely stay under pressure. This is an inference grounded in current market pricing and recent Fed commentary.

Bottom line:

This is still a market where one decent labor headline can help for an hour, and one oil spike can ruin everybody’s mood by lunch.

🧠 Market Analysis –Practical Takeaways

For buyers:

This is still a strategy market, not a perfection market. There are more choices in many areas than there were a year ago, but payment math matters more than headline optimism.

For agents:

The best conversations right now are about structure: seller concessions, buydowns, realistic price expectations, and monthly payment impact. The market is moving, but it is moving carefully.

For homeowners thinking about refinancing:

This week is another reminder that rate windows can shut fast when macro risk returns. The market rarely sends a courtesy text first.

🔒 Lock vs Float

Lock if:

- closing is within 30 days

- the borrower is payment-sensitive

- the file is tight on qualifying

- the deal does not have room for rate surprises

That case got stronger with the MBA rate jumping to 6.57% and the 10-year back near 4.38%.

Float cautiously if:

- the borrower has more time

- the file is strong

- everyone understands the risk

- the borrower can tolerate short-term swings

That is a measured-risk call, not a “let’s just vibe and hope” call. Today’s oil and geopolitical setup still argues for caution.

Simple rule:

If a worse rate creates a real problem, lock. If the borrower has time and flexibility, a cautious float can still make sense.

Stay safe and make today great!