Good morning on this best day of the week, Wednesday from your Hometown lender. Here’s today’s market analysis!

Yesterday, rates were down, then up, then down, then flat. All while watching equities scream higher. Bonds prices and rates are vacillating between the inflationary prospects of higher oil and the economic slowdown of higher oil.

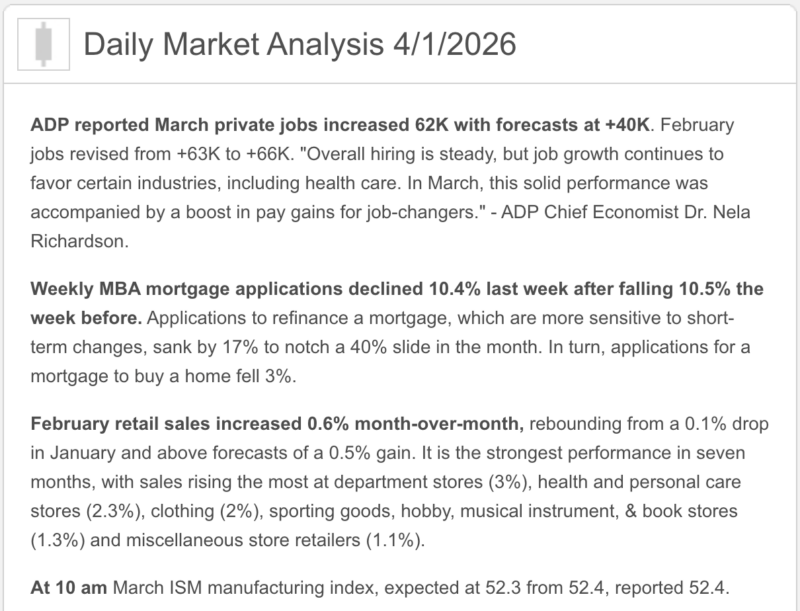

Early on in the war, inflation was the concern but now, it seems the pendulum is swinging and slower economic activity is more in focus. The market absorbed the stronger economic data released this am (ADP payrolls slightly higher, Retail sales slightly higher albeit from before the war) with no visible reaction.

Additionally, several gulf states are at least saying they will support the US militarily to open the Strait of Hormuz. I don’t think I remember another time that has ever happened, but I also don’t remember a time when Iran fired more drones and missiles at neighboring Middle Eastern countries than it has at Israel. The complexion of the Middle East is certainly changing.

This morning, bonds are having a good day. Mortgage bonds and rates are outperforming Treasuries for the moment. I would look at today as an opportunity to lock. There will be a lot more volatility this week as the data mounts tomorrow and Friday.

While markets where unphased by today’s data, I don’t have an expectation that will continue. If you float, be alert.

Market Analysis – From a higher and better view:

Manufacturing looks better, labor looks softer, and rates are still getting pushed around by oil.

🚀 Market Analysis – Quick Snapshot

- Fed: The Fed is still at 3.50% to 3.75% after the March 18 meeting, and Powell said this week the Fed can “wait and see” how the war-driven energy shock affects inflation and growth. Musalem said today policy is likely appropriate “for some time.”

- Inflation: The latest official CPI is 2.4% headline and 2.5% core year over year for February. The latest official PCE is 2.8% headline and 3.1% core for January. Cleveland Fed nowcasts updated today suggest headline inflation may be heating back up in April, largely from energy and supply-chain effects.

- Mortgage rates: The MBA said the average 30-year fixed jumped to 6.57% for the week ended March 27, the highest since August. Freddie Mac’s last weekly survey, released March 26, showed 6.38% for the 30-year fixed and 5.75% for the 15-year.

- Housing: Existing sales rose to a 4.09 million annual pace in February, pending sales rose 1.8%, but new home sales fell to 587,000 in January and builder sentiment is still weak at 38.

- Big drivers today: ADP payrolls, stronger ISM manufacturing, ugly price pressures inside ISM, rising mortgage rates, and ongoing Iran/oil headlines.

The big takeaway:

Today’s market story is not “the economy is crashing” and it is not “everything is fine.” It is more like: growth data is hanging in there, labor is softening underneath, inflation risk is still sticky, and mortgage rates are feeling the inflation/oil side of that tug-of-war more than the soft-labor side.

🎯 Market Analysis – What Happened Today?

This morning gave us two useful reads. First, ADP private payrolls rose 62,000 in March, better than the 40,000 expected, but still not exactly a chest-thumping labor print. Second, ISM manufacturing rose to 52.7, the highest since August 2022, which says manufacturing is still expanding.

The catch is that the ISM internals were much less friendly for rates. Supplier deliveries slowed, and the prices paid index jumped to 78.3, the highest since June 2022, which is a flashing yellow light that inflation pressures are still alive, especially with supply chains and shipping routes getting knocked around by the Middle East conflict.

Translation:

The headline growth number was decent. The inflation smell coming off it was not. Mortgage bonds noticed.

🏦 Fed Watch

The official stance is still unchanged: the Fed held rates at 3.50% to 3.75% in March and said uncertainty remains elevated because of developments in the Middle East. Powell said on March 30 that policy is in a good place to wait and see, because the Fed is balancing downside labor-market risk against upside inflation risk.

Today’s Fed speakers kept that same tone. Barkin said there is no major shift yet in spending or inflation expectations, but he also said a hike case could emerge if inflation expectations move higher. Musalem said policy is likely appropriate for some time, warned against too casually looking through the energy shock, and said both a cut case and a hike case could eventually develop depending on inflation and labor-market data.

One important nuance: Reuters’ March 26 economist poll still showed most economists expecting the Fed to stay on hold until at least September, even though markets had been whipsawing between no cuts and even a small chance of a hike.

Plain English:

The Fed is not trying to save borrowers right now. It is trying not to get caught easing into another inflation mess.

📈 Market Analysis – Where Mortgage Rates Actually Are

The real-world rate picture got worse again this week. The MBA said the average 30-year fixed rose to 6.57%, up 14 basis points on the week and up 48 basis points since February 28. Refinance applications fell 17.3% and purchase applications fell 2.6%.

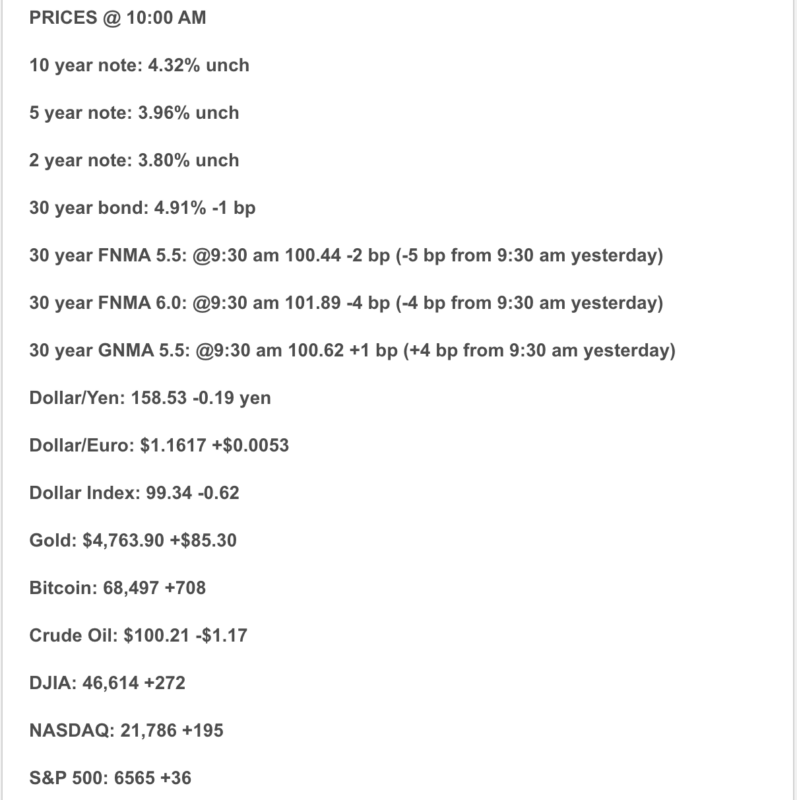

Freddie Mac’s broader weekly benchmark, which is a little less real-time but good for client-facing context, still showed 6.38% for the 30-year fixed and 5.75% for the 15-year as of March 26. Reuters also noted the 10-year Treasury yield was still around 4.32% late Tuesday, even after easing a bit on de-escalation hopes.

Real-world takeaway:

Rates improved earlier in March, then oil, yields, and inflation nerves showed up with a folding chair.

🏠 Market Analysis – Housing Market Check

The good news:

- Existing home sales rose 1.7% in February to a 4.09 million pace.

- Pending home sales rose 1.8% to 72.1, with gains in the West, South, and Midwest.

- Inventory rose to 1.29 million homes, and even the MBA said many markets are looking more like a buyer’s market than they have in some time.

The not-as-fun news:

- New home sales fell to 587,000 in January, near a 3½-year low.

- At that pace, it would take 9.7 months to clear new-home supply.

- Builder sentiment is still only 38, below the 50 break-even line.

What that means:

Housing is still moving, but it is extremely payment-sensitive. More supply is helping, but higher rates are still the bouncer at the door.

🌍 Political + Global Market Backdrop

The macro backdrop is still being driven by the U.S.-Iran war and the oil shock tied to it. Reuters reported today that Rubio said the U.S. can see a “finish line” to the conflict, while Trump said attacks could end within two to three weeks and is scheduled to address the nation tonight. That has helped markets bounce, but the conflict has already raised oil prices and disrupted supply chains.

That matters because even if de-escalation hopes are improving risk sentiment, the inflation damage is already bleeding into the data. Cleveland Fed nowcasts show headline inflation re-accelerating, and Reuters’ earlier import-price report showed a broad-based 1.3% jump in February import prices, with core import prices up 3.0% year over year.

Why that matters:

Mortgage rates do not need a perfect disaster to stay elevated. They just need enough inflation risk to keep bond buyers suspicious, and right now there is still plenty of that going around.

🔮 Market Analysis – What This Means for Rates Going Forward

Base Case

My base case is that rates stay choppy and somewhat elevated near term. The labor market is clearly cooling, but today’s manufacturing and inflation signals were not soft enough to give bonds a clean rally.

Best Case

The best case is that de-escalation with Iran sticks, oil cools further, and Friday’s jobs report comes in soft enough to remind markets that labor weakness is real. That could help rates settle back down. This is an inference, but it follows directly from how markets have been reacting to oil and labor headlines.

Worst Case

The worst case is that energy prices stay elevated, inflation expectations push higher, and Friday’s jobs report is firm enough to keep the Fed parked even longer. In that setup, mortgage pricing stays under pressure. This is also an inference based on current Fed commentary and market pricing.

Bottom line:

This is still a market where one encouraging headline can help for a few hours, and one ugly inflation or oil headline can erase it before lunch.

🧠 Market Analysis – Practical Takeaways

For buyers:

This is still a strategy market, not a perfection market. More homes are available in many areas, but the payment matters more than ever.

For agents:

The message right now is not “panic.” It is “structure matters.” Concessions, buydowns, realistic seller expectations, and sharper monthly-payment conversations are doing more heavy lifting than generic optimism

For homeowners thinking about refinancing:

This week is another reminder that rate windows can close fast. The market does not send engraved invitations before it changes its mind.

🔒 Lock vs Float

Lock if:

- closing is within 30 days

- the borrower is payment-sensitive

- the file is tight on qualifying

- the deal cannot absorb more volatility

That case got stronger this week after the move to 6.57% in MBA data.

Float cautiously if:

- the borrower has more time

- the file is strong

- everyone understands the risk

- the borrower can tolerate short-term rate swings

That is a measured-risk call, not a “let’s see what happens and hope the market becomes nice” call. The current Fed and geopolitical backdrop still argues for caution.

Simple rule:

If a worse rate creates a real problem, lock. If the borrower has flexibility and time, a cautious float can still make sense.ill make sense.

Stay safe and make today great!