And a good Friday morning from your Hometown Lender to you. Here is today’s market analysis.

Yesterday saw some volatility as bonds tracked cease fire headlines but ultimately ended the day much better than when pricing came out. Rate sheets today should be better, reflecting an improvement through the day for bonds yesterday and a good start to the day today (despite the hottest CPI inflation reading in two years). Reprice risk on the day is moderate, bonds will react to news on the cease fire, and if something happens to break it we will see a strong reaction.

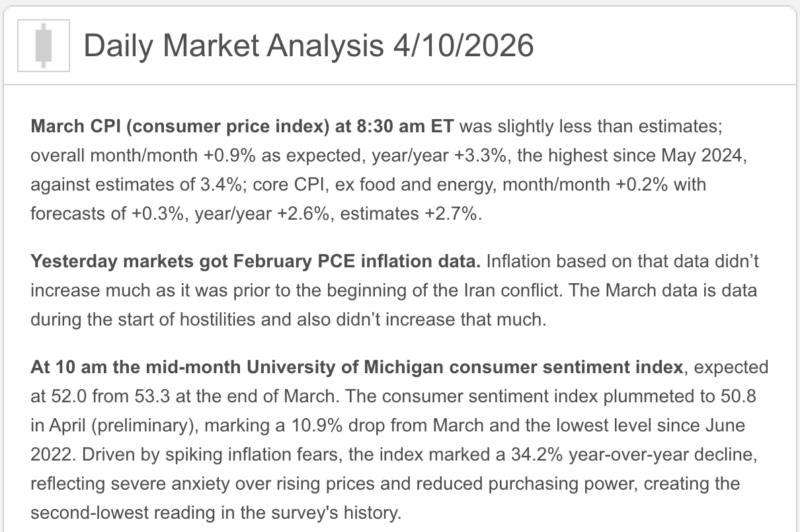

So that inflation data… unlike the PCE data this week, which was still a month behind, the CPI data reflects the first reaction to higher oil and gas prices from the Iran conflict. Bonds didn’t panic though, since it was already a given that we would see a jump in inflation due to the energy shock. The question is how long we expect to see inflation rise after the conflict is over, and if prices will come back down at all (like rates, prices rise quickly but are slow to fall).

Today should be a calm day but remember that we have an entire weekend for something to happen that could cause a strong reaction on Monday.

Market Analysis – From a higher and better view:

Market Analysis – Quick Snapshot

- Inflation came in hot on the headline, cooler on the core. March CPI rose 0.9% month over month and 3.3% year over year, while core CPI rose 0.2% month over month and 2.6% year over year. Gasoline did most of the damage: Reuters reported a 21.2% jump in gasoline accounted for nearly three quarters of the monthly CPI increase.

- Markets are not panicking, but they are not sending thank-you notes either. As of 10:15 a.m. ET, the Dow was down 0.23%, the S&P 500 was up 0.15%, and the Nasdaq was up 0.54% after the CPI report landed roughly in line with expectations.

- The Fed story got more hawkish by inertia, not by enthusiasm. The target range remains 3.50% to 3.75%, and traders on Friday continued to price the Fed on hold through the end of 2026, with only about a one-in-three chance of a cut by December.

- Consumers are feeling it. The University of Michigan’s preliminary April sentiment reading fell to a record low of 47.6 from 53.3 in March. One-year inflation expectations jumped to 4.8% from 3.8%, and five-year expectations rose to 3.4% from 3.2%.

- Mortgage rates improved a hair, but this is not exactly a parade. Freddie Mac’s latest survey shows the 30-year fixed at 6.37% and the 15-year fixed at 5.74%. Existing-home sales for February were 4.09 million, with 1.29 million homes for sale, 3.8 months of supply, and a $398,000 median price.

1) Market Analysis – What Hit This Morning

Today’s main event was clearly the March CPI report, and the headline looked ugly at first glance. A 0.9% monthly gain is the biggest monthly jump since mid-2022, and the yearly rate moved up to 3.3% from 2.4% in February. But under the hood, the report was less broadly inflationary than the headline makes it sound: core CPI rose just 0.2%, and Reuters noted that March likely captured only the initial hit from the oil shock rather than the full secondary effects.

The big villain wore a gas pump costume. Reuters reported gasoline prices surged 21.2% in March and accounted for nearly three quarters of the CPI increase. Food prices were unchanged in March, which helps explain why the core and broader internals looked less disastrous than the headline. BLS data also show the annual picture is still very energy-heavy: energy up 12.5% year over year, gasoline up 18.9%, while all items less food and energy were up 2.6%.

Then came the mood check, and it was not cheerful. Consumer sentiment dropped to a record low 47.6, and inflation expectations moved sharply higher. That matters because even if today’s CPI was mostly an energy story, rising inflation expectations are exactly the kind of thing the Fed does not like to leave unattended.

Narrative you can use:

“Today’s inflation report was loud on the surface because of energy, but the inside of the report was less ugly than the headline. The problem is that rising gas prices, falling consumer confidence, and higher inflation expectations still make it very hard for the Fed to sound comfortable, and that keeps mortgage-rate relief on a short leash.”

2) Market Analysis – Fed Watch

Officially, the Fed is still planted at 3.50% to 3.75%, and its March 18 statement said economic activity has been expanding at a solid pace while inflation remains “somewhat elevated.”

The bigger shift is in tone and market pricing. The March 17–18 FOMC minutes said the Middle East conflict pushed up energy prices, raised near-term inflation projections, and moved rate expectations higher, with the Desk survey showing a cut not fully priced until December and the modal path shifting to no rate change this year.

Today added another layer. San Francisco Fed President Mary Daly told Reuters the oil shock from the Iran war extends the timeline for getting inflation back to 2% and may keep the Fed in a holding pattern, even though she still sees policy as restrictive and in a “good place.” Traders kept bets centered on no cuts in 2026, with only about a one-in-three chance of a December cut. That is not a full-blown hawkish pivot, but it is definitely not a dovish wink either.

3) Market Analysis – Where Mortgage Rates Actually Are

Freddie Mac’s weekly survey now has the 30-year fixed at 6.37% and the 15-year fixed at 5.74%, both slightly lower than a week ago. So yes, rates improved a little. No, nobody should start doing cartwheels in the closing department just yet.

The more market-sensitive MBA survey showed the average contract rate on a 30-year mortgage at 6.51% for the week ended April 3. Reuters reported refinance applications fell 2.8%, purchase applications rose only about 1%, and purchase demand was still 7% below a year earlier. MBA separately said total applications were down 0.8% week over week.

The practical takeaway is the same as it has been for weeks: mortgage pricing is still being driven more by headline inflation, oil, Treasury yields, and Fed timing expectations than by any happy talk about future cuts. Today’s CPI and the jump in consumer inflation expectations do not change that story in a borrower-friendly direction.

4) Market Analysis – Housing Market Check

The latest hard housing data still say the market is moving, just not gliding. February existing-home sales rose 1.7% to a 4.09 million annual pace. Inventory increased to 1.29 million homes, which is 3.8 months of supply, and the median existing-home price was $398,000, up 0.3% from a year earlier.

There is a genuinely encouraging piece in there: NAR said affordability improved for the eighth straight month, with the Housing Affordability Index rising to 117.6, the highest level since March 2022. First-time buyers also made up 34% of transactions in February, up from 31% in January. That does not mean housing is easy, but it does mean conditions are less punishing than they were. Slightly fewer broken ankles on the obstacle course.

For Western-market conversations, the regional split remains useful. The West saw sales rise 8.2% month over month, while the regional median price was down 1.9% year over year to $603,100. That is a good reminder that national housing headlines and local market reality are still not identical twins.

5) Political Backdrop & Fed Independence

The biggest political-macro story remains the fragile U.S.-Iran ceasefire and the damage around the Strait of Hormuz. Reuters reported traffic through the strait was still well below 10% of normal volume on Thursday, with ships requiring Iranian approval, while Saudi Arabia said attacks cut its oil production capacity by about 600,000 barrels per day and reduced East-West Pipeline throughput by about 700,000 bpd.

That matters because this is not just a headline problem. Reuters reported Brent settled at $95.92 on Thursday even after some ceasefire optimism, and the Saudi disruptions hit the very pipeline the kingdom has been relying on while Hormuz flows remain constrained. In other words, markets got a truce headline but not a clean supply-chain fix.

There is also still a trade-policy angle in the background. Reuters said today’s CPI increase reflected not only war-boosted oil prices but also the ongoing pass-through from tariffs. That means the inflation story is not purely geopolitical; policy still has fingerprints on it too.

6) Market Analysis – What This All Means for Rates Going Forward

Base case:

Mortgage rates stay choppy and relatively elevated in the near term. Today’s CPI was hot enough to keep the Fed patient, consumer inflation expectations moved the wrong way, and the energy backdrop is still unstable. That is not a recipe for a clean bond rally.

Better case for rates:

The better path would be a more durable ceasefire, improved Hormuz traffic, lower oil, and a couple of future inflation reports showing that today’s spike was mostly a one-month energy punch rather than a broader re-acceleration. That is an inference, but it is grounded in the fact that core CPI was still just 0.2% in March and BLS data still show much of the damage was energy-led.

Worse case for rates:

If the truce weakens further, Saudi disruptions linger, and higher gas prices start feeding through more fully into April and May data, the Fed could stay sidelined all year and mortgage pricing could remain stubbornly in the mid-6s or worse. Reuters already reported traders are centered on no cuts in 2026, and Daly said the oil shock simply means the inflation fight takes longer.

7) Market Analysis – Practical Takeaways

For buyers, this is still a market where strategy beats wishful thinking. Small changes in rate or structure still matter, and today’s data argue for planning around payment sensitivity instead of betting on sudden rate relief.

For agents, the message is balanced: housing is still moving, inventory is better than it was, and affordability has improved. But confidence is fragile, consumers are rattled, and inflation headlines are still capable of freezing momentum for a few days at a time.

For referral partners, this is not a “rates are about to fall fast” environment. The smarter message is that opportunities still exist, but structure, product choice, concessions, and lock timing matter more than trying to predict every Fed headline from a crystal ball and a caffeine habit.

8) Lock vs Float

- 0–15 days from closing:

I would still lean lock. Today’s CPI, higher inflation expectations, and the still-messy Middle East backdrop are not ideal ingredients for gambling with a near-term closing. - 15–30 days:

This is still case by case. If the borrower is tight on DTI or very payment-sensitive, I would lean protective. If they have room and can handle volatility, there is at least a case for cautious patience if the energy shock fades. - 30+ days:

A cautious float can still make sense, but only with discipline and a stop-loss mindset. Right now this market can turn on one shipping headline, one oil move, or one inflation expectation survey. Not exactly a nap-friendly setup.

Stay safe and make today great!