Good Tuesday am from your Hometown Lender. Let’s get into today’s market analysis!

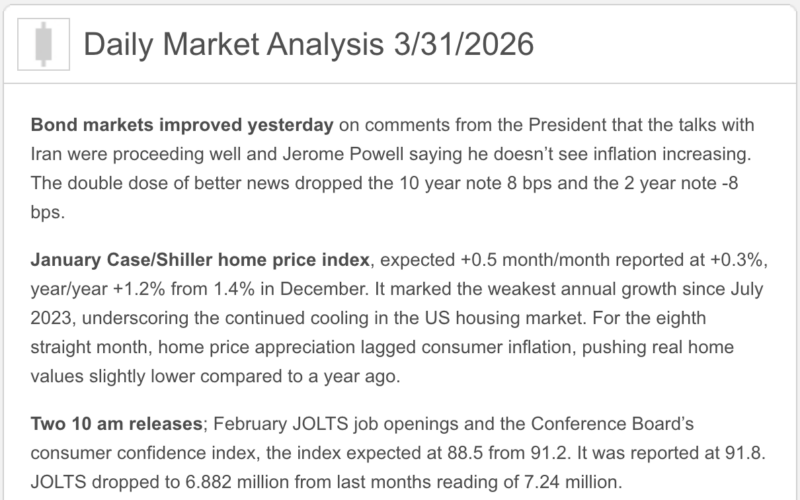

Bond markets improved yesterday on comments from the President that the talks with Iran were proceeding well and Jerome Powell saying he doesn’t see inflation increasing. The double dose of better news dropped the 10-year note 8 bps.

Even though gas has topped $4/gallon (or .9 of a gallon, as we all seem to forget what the pumps deliver for the price), markets are shifting their gaze from the immediate impact of higher inflation to concerns of what happens if the economy slows. This is a more normalized lens and is helping bonds improve yet again today.

I am not sure the improvement will continue through the week, as we have a lot of economic data to come. Today’s Jobs Opening Report (JOLTS) was weak and about 5% below expectations. More people are looking for jobs than there are jobs available. That pendulum has swung.

Be careful floating as most data comes out early, and by the time the markets open, the die is cast.

Market Analysis – From a higher and better view:

Market Analysis – Quick Snapshot (Tuesday, March 31, 2026)

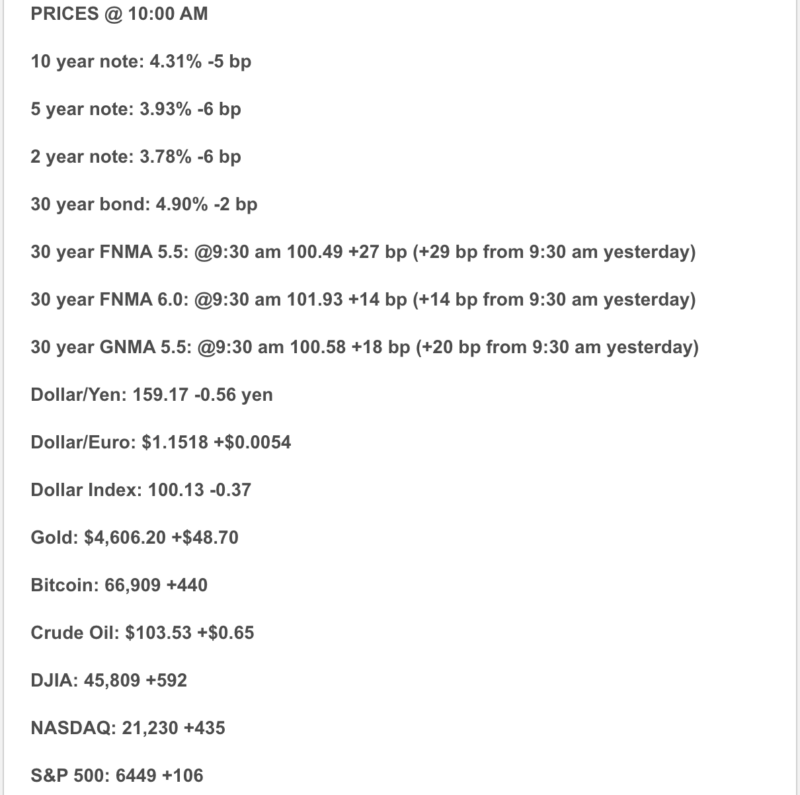

- 10-year Treasury: 4.304% (-4.8 bps) — a meaningful rally this morning.

- MBS (UMBS 30yr 5.0): 98.58 (+0.34) — MBS are firmer, which is the ingredient for better rate sheets.

- Mortgage rates (street-level, top-tier): 30Y fixed 6.55% (-0.09) | 15Y 6.12% (-0.03).

- Today’s data/events: Consumer Confidence + JOLTS (both 10:00am ET) + multiple Fed speakers (Barr, Bowman, Goolsbee, Schmid).

- Current-events driver: Iran/Hormuz energy disruption continues to dominate inflation expectations and policy narrative.

1) Market Analysis – What Hit This Morning (CPI)

No CPI today, but we did get two “CPI-adjacent” reads that matter for rates:

A) JOLTS (Feb 2026 — released today)

- Job openings: 6.9M (little changed)

- Hires: down to 4.8M (big step down)

- Quits: about 3.0M (little changed)

- Layoffs/discharges: 1.7M (unchanged)

Why the bond market cares: Hiring rolling over supports the “growth is cooling” case (good for bonds), even while the war/oil shock keeps inflation fears alive (bad for bonds). Today, the “growth cooling” side is winning in Treasuries.

B) Consumer Confidence (March)

- Confidence edged up to 91.8 (vs 91.0 prior; expectations were lower), but households are bracing for higher inflation as gas prices surge and tariffs keep bleeding through.

Narrative you can use:

“Today’s story is a tug-of-war: the labor market is cooling on the hiring side, but consumers are getting hit with higher inflation expectations from energy and policy uncertainty.”

2) Fed Watch

- The Fed has to balance cooling labor signals with re-heating inflation expectations (energy + tariffs).

- Multiple Fed speakers today (Barr, Bowman, Goolsbee, Schmid) = headline risk, even if the data is already out.

What I’m watching: any language that hints the Fed is more worried about inflation expectations than softening hiring—that’s what would push yields back up.

3) Market Analysis – Where Mortgage Rates Actually Are

- The market setup this morning is friendly: 10Y down and MBS up.

- That’s why you’re seeing the MND index improve (30Y 6.55%, down from recent highs).

Translation: It’s one of those days where you can get a better quote at 10:30 than you could have at 4:30 yesterday.

4) Housing Market Check

No blockbuster housing print today, but the financing environment is the whole story:

- When rates are volatile, buyer confidence is usually the first casualty, not affordability spreadsheets.

- The next big “confidence/velocity” checkpoint is Friday’s jobs report (Mar employment) on April 3.

5) Market Analysis – Political Backdrop & Financing Implications

Two policy/war channels are now bleeding straight into borrowing costs:

A) War costs → deficit/issuance risk (the “financing” angle)

Reuters flagged the next concern after inflation: fiscal costs of a prolonged conflict plus tariff-refund mechanics. Highlights include:

- Deficit could drift from “just under 6% of GDP” toward ~8% if costs stack up

- National debt ~ $39T; net interest projected near $1T this fiscal year

- Pentagon seeking $200B+ supplemental war funding

- Potential ~$175B in tariff refunds after the Supreme Court tariff ruling, with replacement-tariff uncertainty

Why it matters: bigger deficits/issuance = investors demand more yield = mortgages feel it.

B) Energy shock → inflation expectations (the “rate sheet” angle)

- Analysts have jumped 2026 oil forecasts sharply; Reuters’ poll shows Brent forecast $82.85 (up from $63.85 pre-war poll), and notes the Hormuz choke point is ~20% of global oil & LNG transit.

- Consumers are already reacting: inflation expectations popped to levels last seen Aug 2025, with gas breaking $4/gal nationally per AAA (via Reuters).

6) Market Analysis – What This All Means for Rates Going Forward

| Scenario | What happens next | Mortgage-rate bias (near-term) |

| Base case | Hiring cools, but oil/expectations stay hot | Choppy mid-6s, good/bad days |

| Better-rate case | De-escalation + oil cools + labor softens further | Push toward low-6s |

| Worse-rate case | Oil stays elevated + fiscal fear rises | Upper-6s risk (faster reprices) |

7) Practical Takeaways

- Agents: sell certainty. In this tape, structure + credit strategy beats “let’s hope rates behave.”

- Buyers: have two approvals / two payment paths ready (Plan A fixed; Plan B structured—temp buydown/ARM where appropriate).

- Refis: treat this like “catch the window” season. You don’t marry the rate—you date it and refinance later.

8) Lock vs Float

CPI: Apr 10

- Closing ≤ 30 days: lock bias, especially if payment is tight.

- Closing 31–60 days: float only with hard triggers (target rate + maximum pain threshold).

Next scheduled landmines:

- Jobs report: Apr 3

Stay safe and make today great!