Good Monday morning from your Hometown Lender. Let’s dive into today’s Market Analysis!

Friday saw rates hit the highest level of the year despite bonds rallying on the day from early heavy losses. The recovery for bonds was enough that many lenders repriced better, a rare enough occurrence, but one even more rare on a Friday.

Rate sheets will be better today, as bonds start the week surprisingly strong out of the gate. The strong start is even more surprising when you factor in that oil has hit $115 a barrel today. So why the strong start? An argument can be made about end-of-month trading, but I put more stock in traders starting to panic that there will be further escalation with Iran, and it will drag on. That means the fear of inflation is starting to turn into a fear of the conflict’s impact on the economy this year.

Traders seem to be dialing back bets on higher interest rates, instead betting on an economic slowdown (even a possible recession). This argument is supported by Fed futures, which have pulled back some from pricing in Fed rate hikes this year. There is a lot of data coming out this week, most importantly Employment reports (ADP, Unemployment claims, BLS Jobs report), but also Retail Sales, Consumer Confidence, etc.

There will be a lot of volatility. If you held off locking, there is/will be a window here to correct that.

Market Analysis – Quick Snapshot (Monday, March 30, 2026)

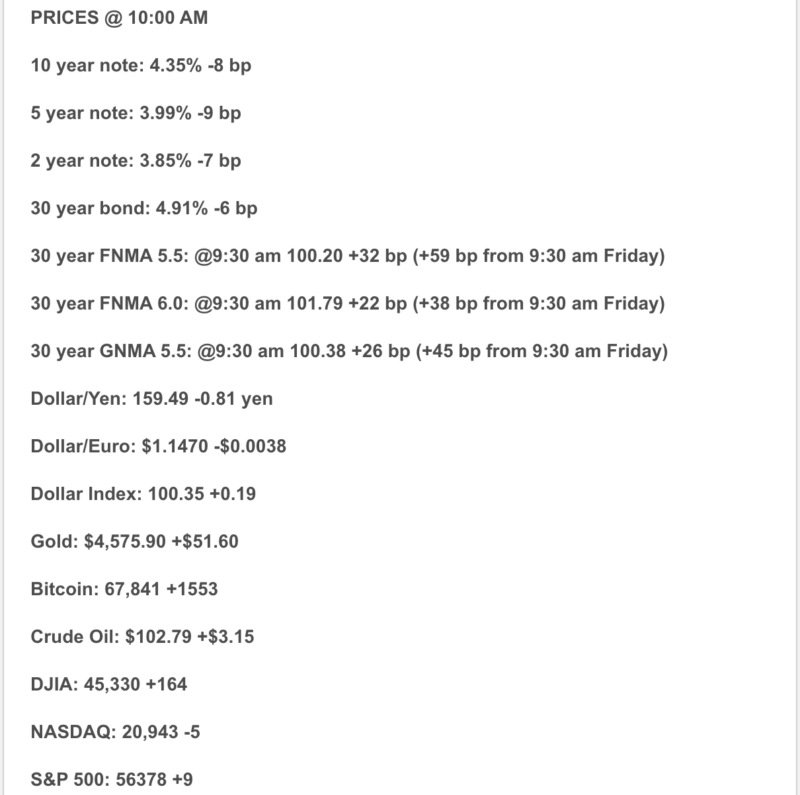

- 10-year Treasury: ~4.345% (down ~9 bps on the day) as growth fears/safe-haven bids offset inflation headlines.

- MBS (UMBS 30yr 5.0): 98.33 (+0.46) — modest support this morning.

- Mortgage rates (MND daily, top-tier): 30Y fixed 6.55% (-0.09) | 15Y fixed 6.12% (-0.03).

- Freddie benchmark (weekly, lagging): 30Y 6.38% | 15Y 5.75% (as of Thu, Mar 26).

- Oil / inflation headline: Brent ~$115 at the open, +59% in March (largest disruption narrative still centered on Hormuz).

- Market mood: liquidity is thinner, bid/ask spreads wider, and volatility is spilling into “normally boring” places like Treasuries.

1) Market Analysis – What Hit This Morning (CPI)

- No CPI today.

- This is another “macro headlines beat the calendar” day: energy shock + risk-off trading is doing the work of an inflation report in real time.

Narrative you can use:

“Rates aren’t trading Tuesday’s data—they’re trading today’s headlines. When oil is moving like this and liquidity is thinner, mortgage pricing can swing on sentiment before any report even prints.”

2) Fed Watch

- The big near-term Fed issue is the same: oil-driven inflation risk vs. growth/financial-conditions tightening.

- Why the 10Y can fall while oil rises: investors are increasingly treating this as stagflation risk (inflation up, growth down), which can pull money into Treasuries even while inflation fears are elevated.

3) Market Analysis – Where Mortgage Rates Actually Are

- Today’s “street” read: 6.55% top-tier 30Y fixed on MND (down from Friday’s highs but still elevated).

- Why your borrowers feel whiplash: liquidity is part of the story now—dealers are less willing to warehouse risk, spreads widen, and rate sheets can reprice faster.

- Weekly averages (Freddie) still useful for trend: 6.38% on the latest PMMS print, but it won’t capture intraday tape bombs.

4) Market Analysis – Housing Market Check

- “Under contract” demand showed a pulse pre-shock: Feb pending home sales +1.8% MoM (-0.8% YoY).

- The risk now is simple: if energy keeps rates volatile into peak spring shopping weeks, confidence gets taxed even when the math almost works.

5) Political Backdrop & Market Implications

- IMF warning shot: the war shock is tightening financial conditions and the IMF’s view is it points toward higher prices and slower growth if it persists.

- Governments are already responding to the fuel shock (example: Australia cutting fuel taxes and underwriting spot cargoes).

- Market plumbing note: volatility + risk reduction is making trading harder and costlier, which can amplify swings in rates.

6) Market Analysis – What This All Means for Rates Going Forward

| Scenario | What happens next | Mortgage-rate bias (next 1–3 weeks) |

| Base case (most likely) | Oil stays high; intermittent “risk-off” rallies in Treasuries | Mid-6s with sharp day-to-day swings |

| Better-rate case | Credible de-escalation + liquidity improves | Back toward low-6s (fast reprices lower possible) |

| Worse-rate case | Prolonged disruption + inflation expectations lift | Upper-6s risk + lenders get more defensive |

Grounding: oil above $100, stagflation framing, and elevated volatility/liquidity stress.

7) Practical Takeaways

- For agents: win deals with certainty + structure (credits, temp buydown, program fit). In a headline tape, “rate shopping” becomes “confidence shopping.”

- For buyers: run two payment paths now (Plan A fixed, Plan B structured) so a single reprice doesn’t derail momentum.

- For refis: expect “windows,” not “trends.” Be ready to lock quickly on down-days.

8) Lock vs Float

This week’s scheduled catalysts: JOLTS (Tue, Mar 31) and Jobs Report (Fri, Apr 3).

- Closing ≤ 30 days: lock bias. Volatility + wider spreads = higher chance of surprise reprices.

- Closing 31–60 days: float only with guardrails (target rate, max pain threshold, and a “headline escalation → lock” rule).

Stay safe and make today great!