Good Morning on this best day of the week Wednesday from your Hometown Lender. Let’s dive into today’s market analysis with some better news.

Yesterday saw bonds recover just a little of what was lost on Monday, with rate sheets showing a small improvement. The gains held through the day, with no real risk of reprices.

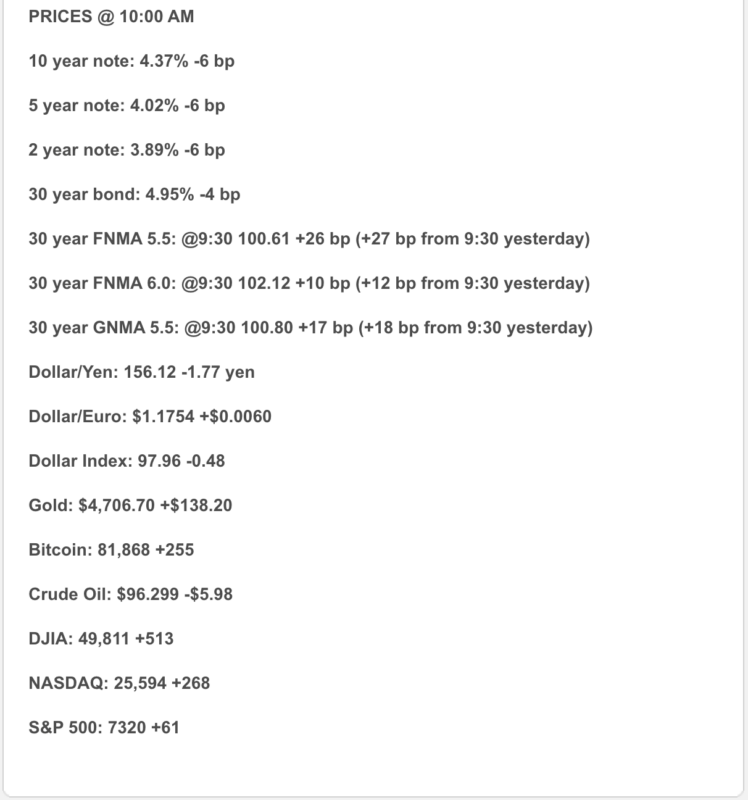

It wasn’t looking like we would see much change heading into today. However, rates today are much better as bonds improve on the news that a deal could be close between the US and Iran. Oil prices slid lower (below $100 a barrel) after Axios reported we were close to an agreement. Also President Trump paused “Project Freedom“, his push to force the reopening of the Strait of Hormuz, saying there was “great progress” in working out a deal.

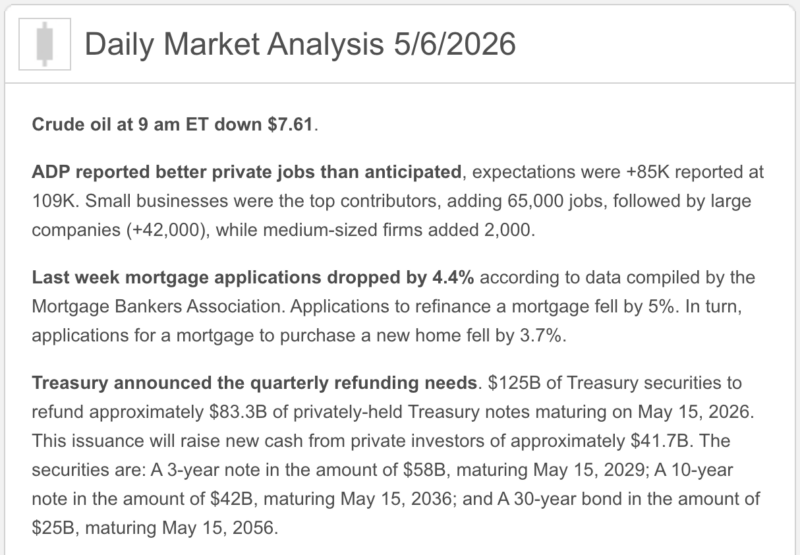

One little add since this is employment week, ADP came out showing more jobs created than expected, but markets didn’t care so it had no effect on rates today.

Market Analysis – From a higher and better view:

Market Analysis – Quick Snapshot

- ADP came in better than expected. Private payrolls rose 109,000 in April, up from a revised 61,000 in March, which reinforces the idea that the labor market is still steady rather than cracking.

- Stocks are acting optimistic. The Dow was up 0.91%, the S&P 500 up 0.79%, and the Nasdaq up 1.01% by mid-morning as AI enthusiasm and reports of a possible U.S.-Iran peace framework pushed risk appetite higher.

- Oil finally exhaled. Reuters said Brent fell 6.6%, and after the EIA report crude was around $101.96 while WTI was about $95.13. That is helpful for rates, even if nobody should start naming their children “Disinflation” just yet.

- The Fed is still on hold. The FOMC kept the target range at 3.50% to 3.75% on April 29 and said inflation remains elevated, in part because of higher global energy prices, while Middle East developments are contributing to a high level of uncertainty.

- Mortgage rates remain improved from early April. Freddie Mac’s latest weekly survey still shows the 30-year fixed at 6.30% and the 15-year fixed at 5.64% as of April 30.

1) Market Analysis – What Hit This Morning

The real story this morning was a better-than-expected jobs read plus a relief move in oil. ADP showed 109,000 private-sector jobs added in April, which says the labor market still has a pulse, while falling oil gave stocks and bonds room to breathe.

Narrative you can use:

“Today’s market likes two things: the labor market is still stable, and oil finally moved lower. That combination does not guarantee better mortgage pricing, but it does give the bond market something friendlier to work with than we had last week.”

2) Fed Watch

The Fed is still in wait-and-see mode. Its April 29 statement kept rates at 3.50% to 3.75% and made clear that inflation and Middle East uncertainty remain the two big reasons policymakers are not rushing toward cuts.

The next real checkpoint for the Fed is Friday’s jobs report. Reuters noted that markets are watching labor data closely because the path to any future cuts still depends on visible labor-market softness, not just wishful thinking and good vibes.

3) Market Analysis – Where Mortgage Rates Actually Are

Freddie Mac’s latest read has the 30-year fixed at 6.30% and the 15-year fixed at 5.64%. Freddie Mac also said purchase applications were running more than 20% above a year ago, which tells you buyers are still engaging even with rates in the mid-6s.

The caution flag is simple: mortgage pricing is still being pushed around more by oil, inflation expectations, and Treasury sentiment than by chatter about future Fed cuts. Today is better, but this market still changes moods faster than a toddler denied a cookie.

4) Market Analysis – Housing Market Check

There was no major fresh housing release this morning, so the best current housing signal is still yesterday’s new-home-sales report. New home sales rose to 682,000 in March, while the median new-home price fell 6.2% year over year to $387,400, which says builders are still finding ways to make deals work.

That is constructive, but not a full victory lap. The spring market is functioning, just still very payment-sensitive.

5) Market Analysis – Political Backdrop & Fed Independence

The political macro story is still Iran and the Strait of Hormuz, but today’s tone improved. Reuters reported that the U.S. and Iran are said to be getting closer to a preliminary memo, which is why oil dropped and both stocks and bonds rallied. Reuters also made clear that no final agreement has been signed yet.

That means the inflation pressure tied to energy has eased for the day, not necessarily for good. Markets are trading peace hopes right now, and peace hopes are not the same thing as peace.

6) Market Analysis – What This All Means for Rates Going Forward

Base case: rates stay choppy but a little friendlier if oil keeps drifting lower and Friday’s jobs report does not come in hot.

Better case: peace progress becomes real, oil falls further, and the bond market starts believing the inflation shock is fading rather than spreading.

Worse case: talks stall again, oil snaps back higher, and a firm payroll number keeps the “higher for longer” camp firmly in charge.

7) Practical Takeaways

For buyers, this is still a market where structure beats hope. Rates are better than the uglier early-April stretch, but not low enough to make payment sensitivity disappear.

For agents and partners, today’s message is balanced: labor looks stable, stocks are happy, oil is calmer, and housing still has a pulse. That is better than panic, but not the same thing as easy mode.

8) Lock vs Float

0–15 days: lean lock.

15–30 days: case by case.

30+ days: cautious float, but only if the borrower can handle headline-driven swings. Oil is quieter today, but it is still the loudest voice in the room.

Stay safe and make today great!