Good Thursday morning from your Hometown Lender. Let’s get the latest market analysis, shall we?

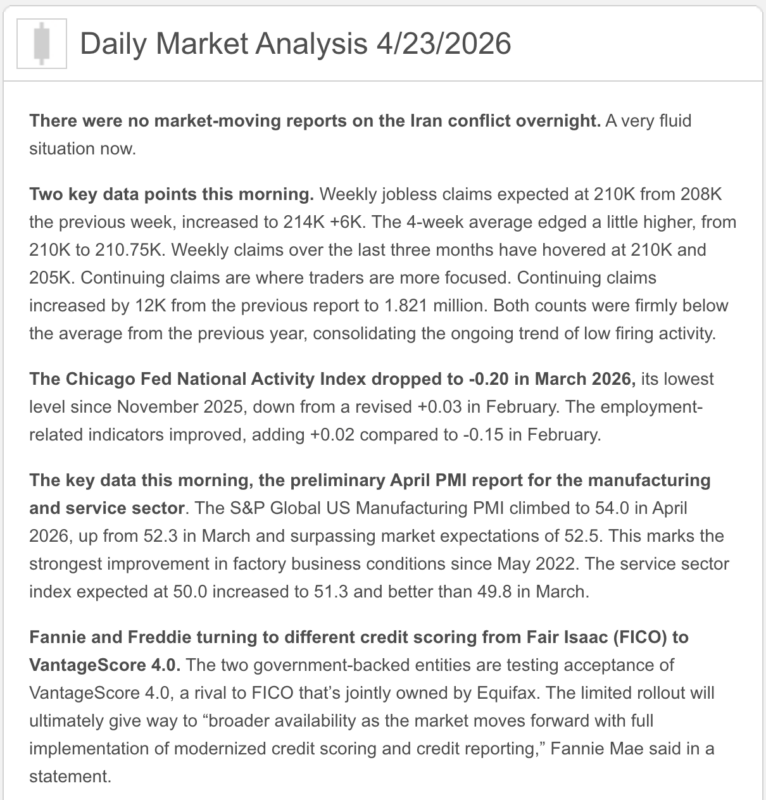

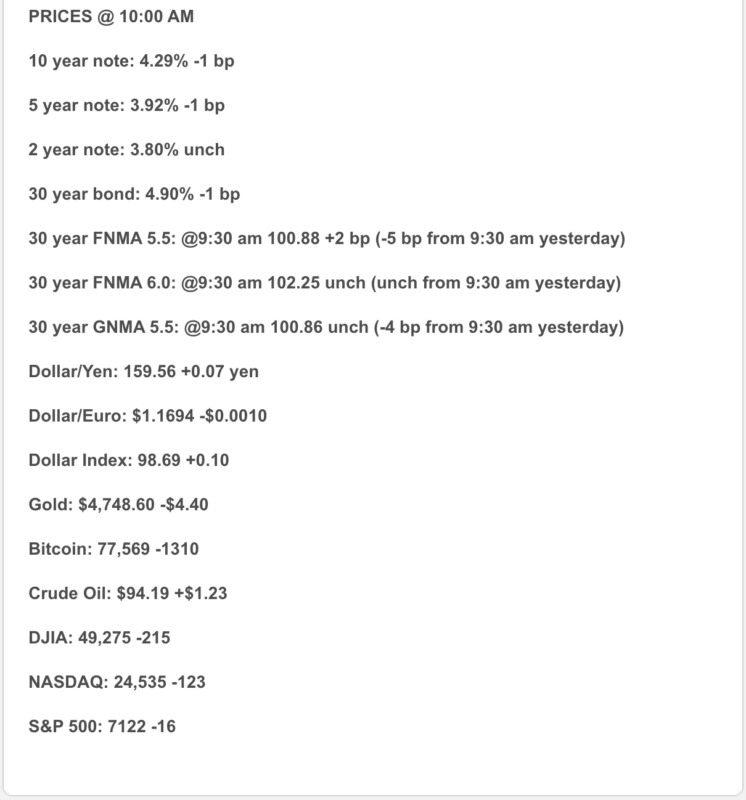

Yesterday saw bonds start the day with some gains, however the afternoon told a different story. Bonds dropped to their worst level of the day and ended down a couple basis points. Rates today are slightly worse than yesterday. Jobless claims this morning came in at 214,000, which translates to slightly higher than the previous week but still consistent with low layoffs. There was no real reaction by bonds to the news.

Although the ceasefire with Iran remains in place, tensions are climbing in the Strait of Hormuz. The US military said it intercepted two Iranian oil supertankers that tried to evade its blockade, and President Trump has ordered the navy to ‘shoot and kill any boat‘ laying mines. Stocks have shaken off the chaos in the Middle East though, and bonds don’t seem to mind that oil is back above $100 a barrel.

For today, it looks like rates will continue treading water, possibly drifting a bit worse through the day. It is unlikely that something will happen today to improve rates.

Market Analysis – From a higher and better view:

Market Analysis – Quick Snapshot

- Today’s big story was “growth is hanging in, but inflation pressure is heating back up.” Weekly jobless claims rose only slightly to 214,000, continuing claims increased to 1.821 million, and S&P Global’s flash Composite PMI rose to 52.0 from 50.3 in March. Manufacturing jumped to 54.0, while services rebounded to 51.3.

- The inflation wrinkle is getting louder. S&P Global’s output-price index rose to 59.9, the highest since July 2022, and input prices hit an 11-month high, largely tied to supply delays and higher commodity costs from the Middle East conflict.

- Oil is back over $100 on Brent. Reuters reported Brent at $103.17 and WTI at $93.68 after Trump threatened to attack ships laying mines in the Strait of Hormuz and peace talks remained stalled.

- Stocks are modestly lower, not melting down. The Dow was down 0.06%, the S&P 500 down 0.03%, and the Nasdaq down 0.29% in morning trading, while the 10-year Treasury yield was about 4.288%.

- The Fed is still parked at 3.50% to 3.75%. The March FOMC statement said inflation remains somewhat elevated and uncertainty about the Middle East implications remains elevated.

- Mortgage rates finally gave buyers a little something. Freddie Mac’s latest weekly survey shows the 30-year fixed at 6.23% and the 15-year fixed at 5.58%, both down from last week.

1) Market Analysis – What Hit This Morning

Today’s data gave us a very 2026-style message: the economy is still expanding, the labor market is still stable, and inflation is still refusing to act house-trained. Claims stayed low enough to say layoffs are contained, while the PMI data showed business activity improving in April after March nearly stalled out.

But the internals were not exactly bond-friendly. Manufacturing strength looked tied partly to stockpiling ahead of supply worries and price hikes, supplier delivery times were the longest since August 2022, and price measures surged. That is growth, yes, but growth wearing an inflation backpack full of bricks.

Narrative you can use:

“Today’s reports showed the economy still has a pulse, but not the kind of pulse that makes the Fed comfortable. Business activity improved and layoffs stayed low, but price pressure heated up again, which keeps mortgage-rate relief from arriving in any dramatic fashion.”

2) Market Analysis – Fed Watch

Officially, nothing changed. The Fed’s target range remains 3.50% to 3.75%, and its March statement said inflation remains somewhat elevated while uncertainty around the economic outlook and developments in the Middle East is elevated.

Unofficially, the market has pushed the easing story further out. A Reuters poll published this week found economists now expect the Fed will wait at least six months before cutting, with 56 of 103 economists expecting the policy rate to still be in the 3.50%–3.75% range at the end of September. The median forecast is now for just one cut this year, and nearly a third of economists expect no change at all in 2026.

Kevin Warsh is now part of the Fed story too. Reuters reported that during this week’s confirmation hearing, he said Trump did not ask him to commit to rate cuts, but he also argued for a “data project” to better measure “underlying” inflation and pushed for a smaller Fed balance sheet over time. That matters because markets are now trying to figure out not just when the Fed might move, but also how a Warsh-led Fed might define inflation pressure.

3) Market Analysis – Where Mortgage Rates Actually Are

This week’s Freddie Mac survey is better. The 30-year fixed averaged 6.23%, down from 6.30%, and the 15-year fixed averaged 5.58%, down from 5.65%. That is the third straight weekly decline and the lowest 30-year reading since mid-March.

That said, mortgage pricing is still being pushed around more by oil, inflation expectations, and Treasury yields than by cheerful speculation about Fed cuts. With Brent back above $103 and price gauges heating up again, today is not exactly a “victory lap for lower rates” kind of day. More like “helpful progress, now please don’t jinx it.”

4) Market Analysis – Housing Market Check

The freshest housing signal is mixed, but not dead. Pending home sales rose 1.5% in March to 73.7, beating expectations, which says buyers were still stepping into contracts before the full effect of April’s oil-and-rate volatility hit.

At the same time, the broader housing backdrop still looks rate-sensitive. Existing-home sales fell 3.6% in March to 3.98 million, while builder sentiment dropped to 34 in April, a seven-month low. Reuters also reported today that PulteGroup posted a drop in first-quarter profit and revenue, with management pointing to affordability worries and economic concerns among buyers.

So housing is still doing what housing has been doing for a while now: moving, but not gliding. Buyers are there, but they are more payment-sensitive, more cautious, and more likely to need incentives or structure to make the math work.

5) Political Backdrop & Fed Independence

The macro-political story is still oil, shipping, and Hormuz. Reuters reported Trump threatened to attack ships laying mines in the Strait of Hormuz, Iran continues to restrict shipping, and both sides are still constraining traffic through a corridor that handled about 20% of daily global oil supplies before the war.

That is why the inflation story is still so sticky. Reuters reported the Iran war’s energy shock is seeping deeper into the global economy, raising production costs, disrupting deliveries, and reviving concerns that inflation could accelerate again even if growth only muddles along.

The Fed-independence layer is now live, not theoretical. Warsh’s hearing this week reassured markets a bit on independence because he said Trump did not ask for a rate-cut promise, but his comments about redefining “underlying” inflation and shrinking the balance sheet also signal that the next Fed chapter may look stylistically different even if immediate cuts are still hard to justify.

6) Market Analysis – What This All Means for Rates Going Forward

Base case:

Mortgage rates stay choppy, with a slight downward bias only if oil stops behaving like a toddler with a drum set. Claims are still low, PMI says the economy is still expanding, and the price data inside that PMI report are hot enough to keep the Fed cautious.

Better case for rates:

The better path is that shipping stress eases, oil backs off from triple digits on Brent, and the next inflation reads prove today’s PMI price spike is more supply-shock noise than broad demand-driven reacceleration. That is an inference, but it is grounded in the fact that economists in the Reuters poll still mostly expect at least one cut this year if inflation behaves better later on.

Worse case for rates:

If Hormuz stays jammed, oil climbs further, and the PMI price spike starts showing up more clearly in PCE and consumer inflation data, the Fed likely stays on hold longer and mortgage rates can easily lose some of this week’s improvement. Reuters’ poll already shows a meaningful jump in economists expecting no cuts at all in 2026.

The next big macro checkpoints are March PCE on April 30 and the Employment Cost Index for Q1 on April 30, both official releases that matter a lot for the Fed’s inflation and labor-cost outlook.

7) Practical Takeaways From Market Analysis

For buyers, today’s setup still says structure beats hope. The Freddie Mac rate move is encouraging, but monthly payment strategy still matters more than betting your deal on a perfect macro headline.

For agents, the message is balanced: pending sales improved, which is good, but builder sentiment, existing-home sales, and homebuilder earnings still say affordability is doing damage. The market is alive, just not exactly moonwalking.

For refi and move-up conversations, the honest message is still not “rates are about to tumble.” The smarter message is that windows may open, but they are likely to open because oil calms down and inflation expectations cool off, not because the Fed suddenly becomes everyone’s favorite uncle.

8) Lock vs Float

0–15 days from closing:

I would still lean lock. This week’s mortgage-rate improvement is real, but today’s oil and PMI price data are a reminder that the market can reverse fast.

15–30 days:

This is still case by case. If the borrower is tight on DTI or highly payment-sensitive, I would still favor protection. If they have room, there is at least a reasoned case for cautious patience, but only if you are watching the tape closely.

30+ days:

A cautious float can make sense, but only with discipline. Right now the market is trading labor resilience, oil, shipping risk, and Fed politics all at once.

Stay safe and make today great!