Good Monday am from your Hometown Lender. Let’s dive into Monday market analysis!

Friday was a sunny day as rates continued to move lower on news that the Strait of Hormuz would once again be open to commercial traffic. Bonds rallied and rate sheets were the best we’d seen in a month. Although bonds did fall back a bit from the best levels of the day, it wasn’t enough to cause alarm or reprices worse. The outlook at the end of the day was that we had some positive momentum heading into this week, with some room for rates to improve further.

Unfortunately, this morning we wake up to bonds being a bit worse, but nowhere near as bad as one might expect when you look at the headlines from over the weekend. Commercial traffic through the Strait of Hormuz is back to a standstill this morning after the brief reopening ended with the US seizure of an Iranian vessel. Despite Iran’s announcement that it would not impede traffic through the strait, President Trump did not remove the naval blockade on Iranian ports, and Iran responded by shutting the strait down again.

The ceasefire is holding, however, and although oil prices jumped there remains some optimism among traders. Mortgage bonds are down only a few basis points right now. The expectation to news like this would be that bonds would be much worse… and we should pay attention to the story that traders are telling us right now. Basically, traders seem to expect the bumps in the road that have come and are still betting on a deal getting done soon. Even a Trump post about knocking out “every single Power Plant, and every single Bridge, in Iran” doesn’t seem to have shaken markets much. We have to be ready for more selling in bonds if things escalate with Iran through the day or if traders change their minds.

I think locking is a good idea.

Market Analysis – From a higher and better view:

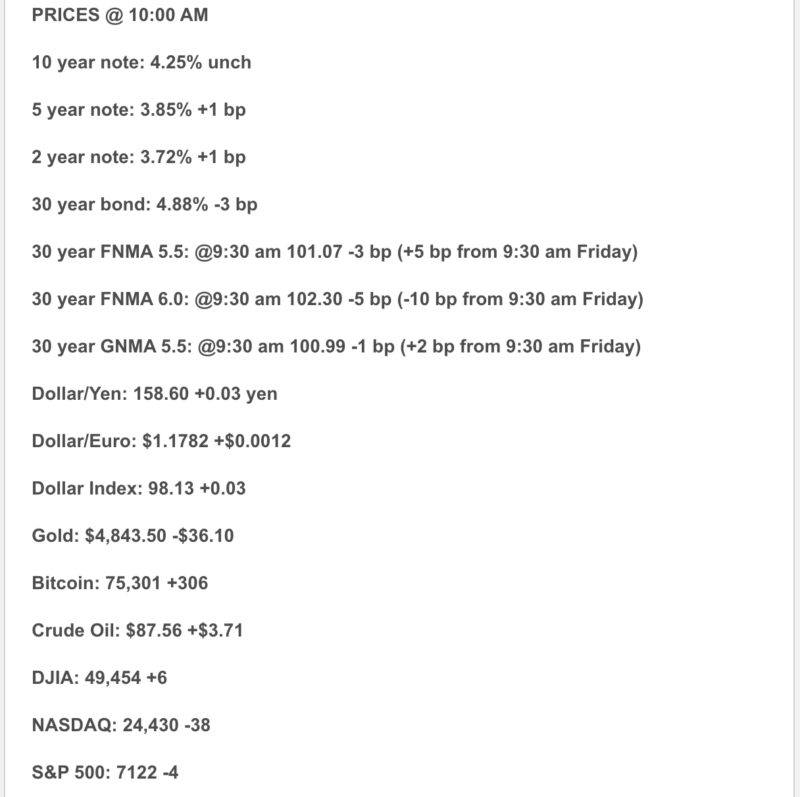

Market Analysis – Quick Snapshot

- The market opened the week in a risk-off mood after renewed U.S.-Iran tensions rattled the ceasefire story. At 10:05 a.m. ET, the Dow was up 0.01%, the S&P 500 was down 0.10%, and the Nasdaq was down 0.24%.

- Oil is back in the driver’s seat. Reuters reported Brent at $94.75 and WTI at $88.61 by late morning GMT, both up about 5%, as fears grew that the ceasefire could collapse and traffic through Hormuz remained badly disrupted.

- The 10-year Treasury yield was around 4.27% in early trading, up as oil and geopolitical risk pushed inflation nerves back onto center stage.

- The Fed’s target range remains 3.50% to 3.75%, and the next major political/Fed event is Kevin Warsh’s Senate Banking Committee hearing on Tuesday, with Jerome Powell’s chair term still set to end on May 15.

- Mortgage rates are a little better than the early-April spike, with Freddie Mac’s latest weekly survey showing the 30-year fixed at 6.30% and the 15-year fixed at 5.65%.

- There was no fresh retail-sales report today because the March release was delayed to April 21, and there was no fresh housing-starts report because March new residential construction was delayed to April 29.

- Housing still looks soft around the edges: existing-home sales fell 3.6% in March to 3.98 million, while builder sentiment dropped to 34 in April, a seven-month low.

1) Market Analysis – What Hit This Morning

There was no major top-tier U.S. data release this morning, so markets took their cues from the thing that has been bossing rates around for weeks: oil and the Middle East. Over the weekend, the U.S. seizure of an Iranian cargo ship and Tehran’s renewed hard line threw fresh doubt on whether the ceasefire would hold. That pushed oil up, stocks off their highs, the dollar firmer, and Treasury yields higher.

That does not mean the U.S. data backdrop disappeared. It just means today’s market is trading geopolitics first, economics second. The next hard domestic checkpoint is March retail sales on Tuesday, April 21, after Census delayed the release from last week.

Narrative you can use:

“Today’s bond-market story is simple: higher oil is acting like a tax on optimism. We did not get a big U.S. economic report this morning, so markets are reacting mostly to renewed Iran risk, higher crude, and the possibility that inflation stays sticky longer than hoped.”

2) Fed Watch

Officially, nothing changed. The Fed is still in a 3.50% to 3.75% target range and said in March that it would carefully assess incoming data, the evolving outlook, and the balance of risks.

Unofficially, the Fed story is getting more political. Kevin Warsh faces lawmakers on Tuesday as Trump’s nominee for Fed chair, and Reuters notes that lawmakers are likely to press him on Fed independence, inflation targeting, balance-sheet policy, and political influence at a time when Trump is openly demanding much lower rates. Powell’s final day as chair is still expected to be May 15, which keeps this from being background noise.

The market is also still split on cuts. Reuters reported on April 17 that Deutsche Bank now expects no Fed cuts in 2026, while Goldman Sachs, BofA, and Barclays still expect the first cut in September; Reuters also said money markets were no longer pricing in easing this year as of that report. Today’s rebound in oil does not exactly make the dovish case easier.

3) Market Analysis – Where Mortgage Rates Actually Are

Freddie Mac’s latest survey shows the 30-year fixed at 6.30% and the 15-year fixed at 5.65%, down from 6.37% and 5.74% the prior week. So yes, mortgage rates improved. No, nobody should start acting like the bond market found inner peace.

The bigger issue is that mortgage pricing is still being pushed around more by oil, inflation expectations, and Treasury yields than by happy talk about future Fed cuts. With crude back up around the mid-$90s for Brent and the 10-year higher again, today is a reminder that last Friday’s relief rally did not come with a lifetime warranty.

4) Market Analysis – Housing Market Check

The latest hard resale data are still not exactly cheerful. Reuters reported March existing-home sales fell 3.6% to a 3.98 million annual pace, the weakest since June 2025. Inventory rose to 1.36 million and the median price climbed to $408,800, but NAR also cut its 2026 existing-home sales growth forecast from 14% to 4%.

The builder side is not throwing a parade either. Builder sentiment fell to 34 in April, with current sales at 37, future sales expectations at 42, and buyer traffic at 22. NAHB said builders are dealing with rising material costs, higher rates, and economic uncertainty.

Today added another useful wrinkle: Reuters reported homebuilders are bracing for another tough year as tariffs, the Iran war, and higher input costs squeeze margins, while many are leaning on mortgage-rate buydowns to keep buyers in the game. That is a very mortgage-market sentence if there ever was one.

5) Market Analysis – Political Backdrop & Fed Independence

The biggest political and macro story is still the same one wearing a slightly different costume: the U.S.-Iran ceasefire may be wobbling, but diplomacy is not completely dead. Reuters reported Monday that Iran is positively reviewing participation in new peace talks in Pakistan, though no final decision has been made, and a Pakistani source said the ceasefire expires at 8 p.m. EST Tuesday.

At the same time, the blockade remains, the Strait of Hormuz is still badly impaired, and Reuters reported traffic was down to just three crossings in 12 hours even as oil stayed 3%–4% up on the day in that story. Since Hormuz normally handles about one-fifth of the world’s oil and liquefied gas supply, this is not just foreign-policy theater. It is directly tied to inflation, rates, and housing affordability here at home.

Then there is the Fed-independence angle. Warsh’s hearing tomorrow is not just about who gets Powell’s chair. It is also about whether markets believe the next Fed leader will defend the inflation target and institutional independence while the White House keeps pushing for aggressive rate cuts. That is why this hearing matters to bonds and mortgage pricing even before a single vote happens.

6) What This All Means for Rates Going Forward

Base case: mortgage rates stay choppy and a touch vulnerable near term. Last week’s relief came from lower oil and hopes for diplomacy. Today’s reversal shows how fragile that relief still is. Higher crude, higher yields, and a still-cautious Fed are not a clean recipe for a big rate rally.

Better case for rates: Iran joins the talks, the ceasefire gets extended, oil cools back down, and Tuesday’s retail-sales report shows a consumer who is not overheating. In that setup, bonds could breathe again and mortgage pricing could improve further. That is an inference, but it is grounded in how sharply markets reacted both to the Friday reopening of Hormuz and Monday’s renewed tensions.

Worse case for rates: talks fall apart, the ceasefire expires Tuesday night, oil moves higher again, and the Fed-chair drama starts to look less like noise and more like policy risk. In that world, the market leans harder into “higher for longer,” and the mid-6s on mortgage rates stick around like an unwanted houseguest.

7) Market Analysis – Practical Takeaways

For buyers, this is still a market where structure beats hope. Freddie Mac looks a little better, but affordability is still fragile, builders are still leaning on incentives, and the next few headlines can move pricing fast. Buydowns, concessions, and product choice still matter a lot.

For agents, the message is balanced: inventory is better than it was, but both existing-home sales and builder sentiment still say this spring is softer than people wanted. The market is moving. It is just doing so with one eyebrow raised.

For refi and move-up conversations, the honest message is still not “rates are about to tumble.” The better message is that windows may open, but they are being driven more by oil and bond sentiment than by any clear Fed pivot.

8) Lock vs Float

- 0–15 days from closing: I would still lean lock. Today’s oil move and ceasefire uncertainty are exactly the kind of things that can undo a little progress in a hurry.

- 15–30 days: this is still case by case. If the borrower is tight on DTI or very payment-sensitive, I would favor protection. If they have room, tomorrow’s retail-sales report and Warsh hearing are real catalysts worth watching.

- 30+ days: a cautious float can make sense, but only with discipline. Right now this market is trading oil, ceasefire credibility, and Fed politics all at once.

Stay safe and make today great!