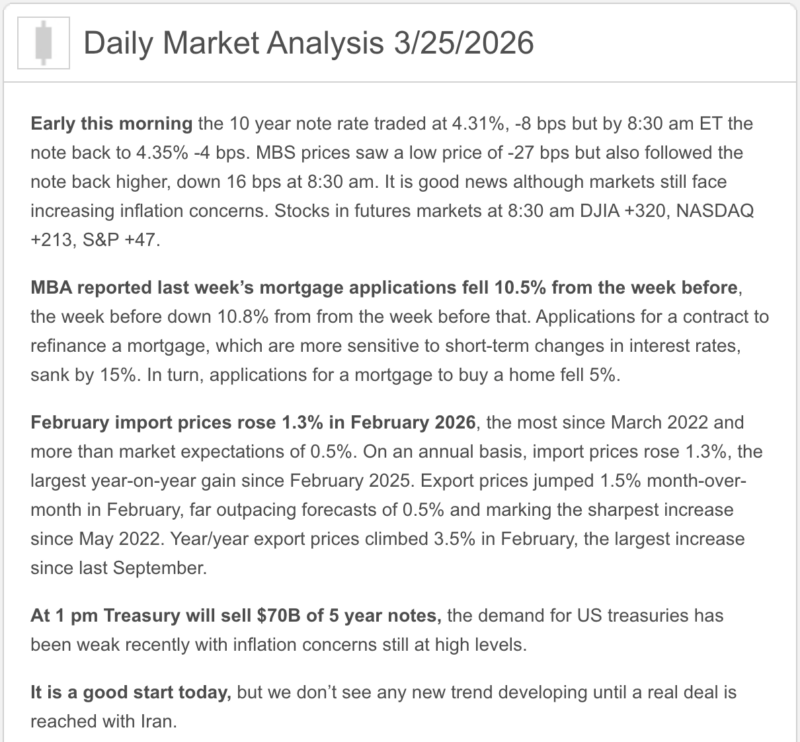

Good morning on this best day of the week, Wednesday from your Hometown Lender. Here’s today’s market analysis.

Yesterday showed just how crazy bonds like to get. Up, down, up, down… and then see bonds jump in the last 20 minutes of the day to end with gains after being about the same as when pricing came out.

Volatility. It’s not just a word; it’s become a way of life.

Rate sheets today should start the day a little better as oil prices fall back below $100 a barrel for the first time in days and bonds got a bit of a boost from talk of stepped-up efforts to bring the Middle East conflict to a close. However, reprice risk remain high as bonds will react to any new news of boots on the ground or a breakdown in talks.

The big question today is do we risk it, and hold out to see if there is an actual cease fire announced? Are we close enough to a deal to risk rates moving higher?

Market Analysis – From a higher and better view:

Wednesday Market Pulse: Rates, Oil, Fed Drama, and Housing Doing Its Best

🚀 Quick Snapshot Market Analysis

Here’s the fast version before the coffee fully kicks in:

- Fed: Still sitting at 3.50% to 3.75%

- Inflation: Still above target, still annoying

- Mortgage rates: Back up a bit after recent improvement

- Housing: Hanging in there, but affordability is still the party pooper

- Big drivers today: Oil, geopolitics, Fed uncertainty, and rate volatility

The big takeaway:

Mortgage rates had started to improve, but global tension and inflation concerns pushed them back higher again. So today’s market story is less about one economic report and more about the broader “don’t do anything weird, world” backdrop.

🎯 Market Analysis – What Happened Today?

Normally, we’d be reacting to a major economic report this morning, but Durable Goods got bumped to April 7.

So instead, the market is focused on:

- Higher oil prices

- Middle East tensions

- Sticky inflation concerns

- Fed officials sounding in no rush to cut rates

Translation: bond markets are nervous, and when bond markets get nervous, mortgage pricing usually gets less friendly.

🏦 Fed Watch Market Analysis: No Cut Fever Yet

The Fed held rates steady at its last meeting, and while the official forecast still shows one rate cut in 2026, the tone is basically:

- “We’re not cutting until we’re really sure inflation behaves.”

- That matters because the market is becoming less convinced cuts are coming anytime soon.

- So even if the Fed still leaves the door cracked open, traders are looking at inflation, oil, and global risk and saying:

- “Yeah… maybe not so fast.”

Plain English:

The Fed is not trying to rescue borrowers right now.

Their focus is still inflation first.

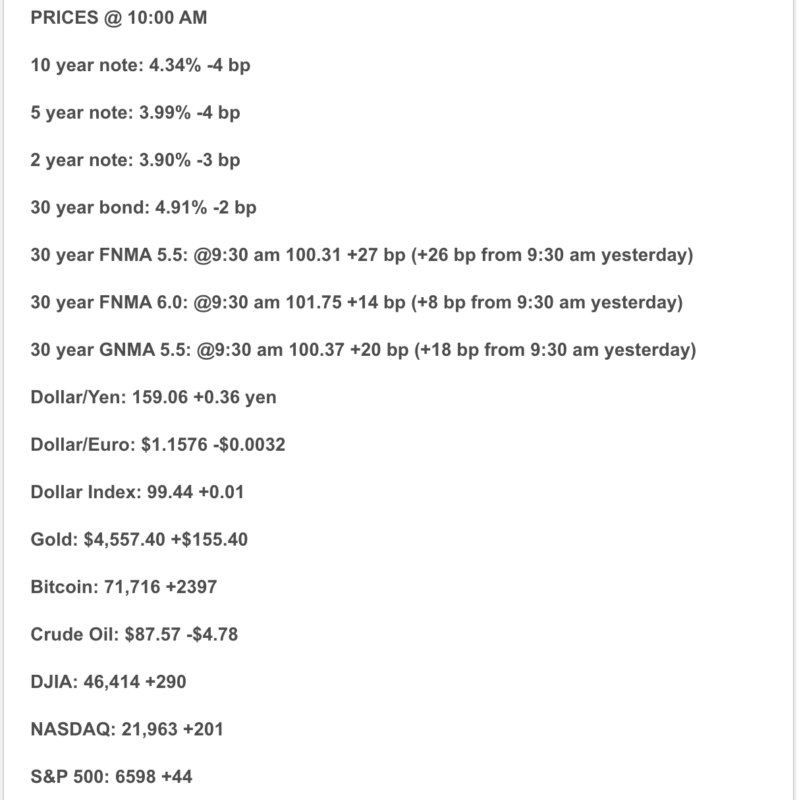

📈 Market Analysis – Where Mortgage Rates Actually Are

This is where consumers get confused, because there are always different rate numbers floating around.

The clean version:

- Freddie Mac weekly average: 6.22% for a 30-year fixed

- MBA application market rate: 6.43%

So yes, rates had improved earlier in the month, but this week they’ve backed up again.

Real-world takeaway:

- Rates are still bouncing around.

- That’s why some borrowers feel like they heard “things are getting better” and then suddenly got hit with a less-fun quote. Mortgage pricing has all the emotional stability of a toddler with no nap.

🏠 Housing Market Check

Housing is not collapsing. It’s just… working harder than it should have to.

The good news:

- Existing home sales improved

- Pending home sales also moved higher

- There are still buyers in the market when rates give them even a little breathing room

The not-as-fun news:

- Affordability is still tight

- Entry-level inventory is still limited

- Builders are still using incentives and price cuts to keep deals moving

What that means:

- Demand is there, but it is very payment-sensitive.

- When rates improve, activity picks up.

- When rates move up again, buyers get cautious fast.

🌍 Market Analysis – Political + Global Market Backdrop

This is the part many borrowers don’t realize matters to mortgage rates.

Today’s market is being heavily influenced by:

- Ongoing Middle East tensions

- Oil price volatility

- Continued concerns about inflation staying higher for longer

- Trade and tariff uncertainty still floating around in the background

Why that matters:

- When oil rises, inflation fears usually rise with it.

- When inflation fears rise, bond yields tend to rise.

- When bond yields rise, mortgage rates often follow.

It’s all connected. Fun, right?

🔮 What This Means for Rates Going Forward: Market Analysis

Base Case

- Rates stay choppy and a little elevated in the near term.

- We probably keep seeing headline-driven swings until inflation cools more clearly or geopolitical tension eases.

Best Case

- Oil calms down, global tensions cool off, inflation fears ease, and mortgage rates improve again.

Worst Case

- Conflict drags on, oil stays elevated, inflation sticks, and the market pushes rate cuts farther out.

- That would keep pressure on mortgage rates.

Bottom line:

We are still in a market where one decent week can get erased by one ugly headline.

🧠 Practical Takeaways

For buyers:

This is still a strategy market, not a “wait for perfection” market.

If the home works, the numbers work, and the structure is smart, there are still opportunities.

For agents:

Spring momentum is real, but it is fragile.

Payment conversations, concessions, buydowns, and loan structure matter more than ever.

For homeowners thinking about refinancing:

This is another reminder that rate improvements can disappear quickly.

When opportunity shows up, it does not always send a calendar invite first.

🔒 Lock vs. Float

Lock if:

- Closing is within 30 days

- The borrower is payment-sensitive

- Qualification gets tight quickly

- The deal doesn’t have room for surprise

Float cautiously if:

- There is more time before closing

- The borrower has strong flexibility

- Everyone understands this market can turn fast on global headlines

Simple rules:

- If a worse rate creates a problem, lock.

- If the borrower can tolerate some movement and has time, a cautious float may still be reasonable.

🗣️ Easy Talking Points You Can Use Today

Consumer-friendly:

“Mortgage rates had started to improve, but recent global events pushed them back up a bit. Right now, oil prices, inflation concerns, and Fed uncertainty are all keeping pressure on rates.”

Agent-friendly:

“Housing data showed some encouraging signs, but the recent move higher in mortgage rates could slow momentum if inflation and geopolitical risks stay elevated.”

Market-savvy:

“The Fed still projects one cut, but the bond market is acting a lot more skeptical. Until inflation and oil calm down, mortgage pricing will probably stay volatile.”

👀 What We’re Watching Next

Market Analysis – Here are the next big potential market movers:

- Jobs report

- Durable Goods on April 7

- PCE inflation

- Any major Fed commentary

- And of course, anything that moves oil or geopolitical risk

Because in this market, one headline can change the tone faster than a buyer asking, “Can we also keep the payment under rent?”

✅ Today’s Bottom Line

Housing is still moving.

- Buyers are still buying.

- But rates are once again dealing with inflation pressure, global tension, and a Fed that is in no hurry to ride in like a hero.

So for now:

- Be strategic. Be realistic. Be ready.

- And if you’re financing, structure matters just as much as rate.

Stay safe and make today great!