Good Thursday AM from your Hometown Lender. Let’s get into today’s market analysis!

Yesterday saw bonds improved throughout the day after news broke that a deal was close between the US and Iran, and oil dropped. Rate sheets today should continue to improve, matching pricing we saw back on April 17th as bonds continue to improve. As long as nothing happens to derail optimism around peace talks with Iran we should be ok.

As far as locking and floating today, remember that tomorrow brings the BLS jobs data which could cause some pullback (at least temporarily) if it comes in stronger than expected. For loans closing farther out it’s not even something to worry about, but for the outlook for rates and pricing today and tomorrow it comes into play.

Market Analysis – From a higher and better view:

Market Analysis – Quick Snapshot

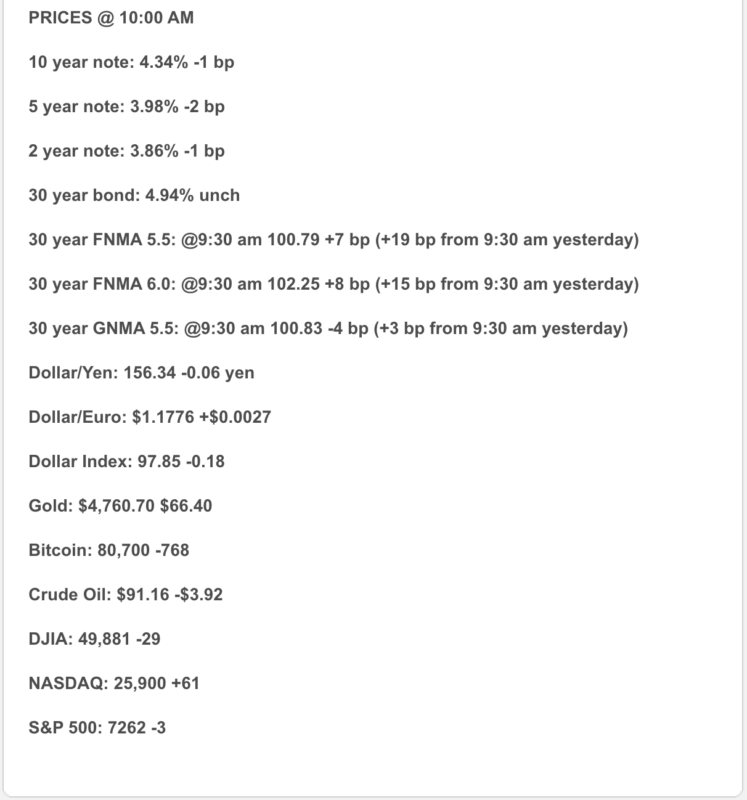

- Labor still looks steady. Initial jobless claims rose to 200,000 for the week ending May 2, while continuing claims fell to 1.766 million. That is still a “low fire, low drama” labor market.

- Productivity cooled, but labor costs did not flare up. Q1 nonfarm productivity rose at a 0.8% annualized rate, down from 1.6% in Q4, while unit labor costs rose 2.3%, a bit softer than expected.

- Markets like the oil move. Hopes for a temporary U.S.-Iran deal pushed Brent down to about $96.62, and stocks stayed near records, with the Dow up 0.08%, the S&P 500 up 0.07%, and the Nasdaq up 0.31% mid-morning.

- The Fed message is still “not anytime soon.” Cleveland Fed President Beth Hammack said rates are likely on hold for “quite some time,” reinforcing the idea that the bar for cuts remains high.

- Latest available Freddie Mac survey: the 30-year fixed is 6.30% and the 15-year fixed is 5.64% as of April 30. Freddie Mac’s page still showed April 30 as the latest published PMMS reading when I checked.

1) Market Analysis – What Hit This Morning

Today’s domestic read was fairly clean: claims remain low, productivity slowed, and labor costs stayed contained enough to avoid a fresh inflation scare. That is not weak enough to rescue bonds on its own, but it is also not the kind of report that forces the Fed to get more aggressive.

Narrative you can use:

“Today’s data said the labor market is still stable and productivity cooled a bit, but the bigger market mover is still oil. With crude pulling back on peace-talk optimism, rates are getting some breathing room — at least for today.”

2) Fed Watch

The Fed is still in hold mode, and today’s live messaging did not soften that stance. Hammack said rates will likely stay unchanged for quite a while, while traders are still betting the Fed stays put through year-end because the labor market is resilient and energy prices remain elevated versus prewar levels.

3) Where Mortgage Rates Actually Are (Market Analysis)

The latest available Freddie Mac benchmark remains 6.30% on the 30-year fixed and 5.64% on the 15-year. That is still better than the early-April spike, but mortgage pricing remains far more sensitive to oil, Treasury yields, and inflation expectations than to rate-cut wishcasting.

4) Market Analysis – Housing Market Check

No major fresh housing release is driving today’s tape. So the practical housing read is unchanged: rates are still mid-6s, buyer demand had been improving on modestly lower rates, and today’s oil pullback is helpful — but it is not a permanent hall pass for affordability. That last part is an inference based on Freddie Mac’s current rate level and the market’s strong reaction to oil.

5) Political Backdrop & Fed Independence

The macro story is still Iran, Hormuz, and whether a temporary deal becomes real. Reuters reported the U.S. and Iran are exploring a short-term framework to halt fighting and reopen the Strait of Hormuz, which is why oil is down and stocks are calmer today. But the key disputes are not fully resolved, so markets are treating this as progress, not closure.

6) Market Analysis – What This All Means for Rates Going Forward

Base case: rates stay choppy but a touch friendlier if oil keeps easing.

Better case: peace talks stick, Hormuz normalizes further, and Friday’s payrolls come in soft enough to calm the bond market.

Worse case: talks stall, oil snaps back up, and the labor data stay too firm to reopen the rate-cut conversation.

7) Market Analysis – Practical Takeaways

For buyers, this is still a market where structure beats hope. For agents and partners, today is constructive, but not conclusive: lower oil helps, stable claims help, and stocks like it — but none of that guarantees a straight-line improvement in mortgage pricing.

8) Lock vs Float

0–15 days: lean lock.

15–30 days: case by case.

30+ days: cautious float, but only if the borrower can handle headline-driven swings. Oil is quieter today, but it is still the loudest voice in the room.

Stay safe and make today great!