Good Friday morning from your Hometown Lender. Let’s get into Friday’s market analysis!

Yesterday bonds started to sell off almost immediately after the open. We can blame the move on some headlines about some skirmishes between the US and Iran that didn’t break the ceasefire but more likely which we can see now that today’s pricing is better after the data, traders were getting ahead of the jobs data.

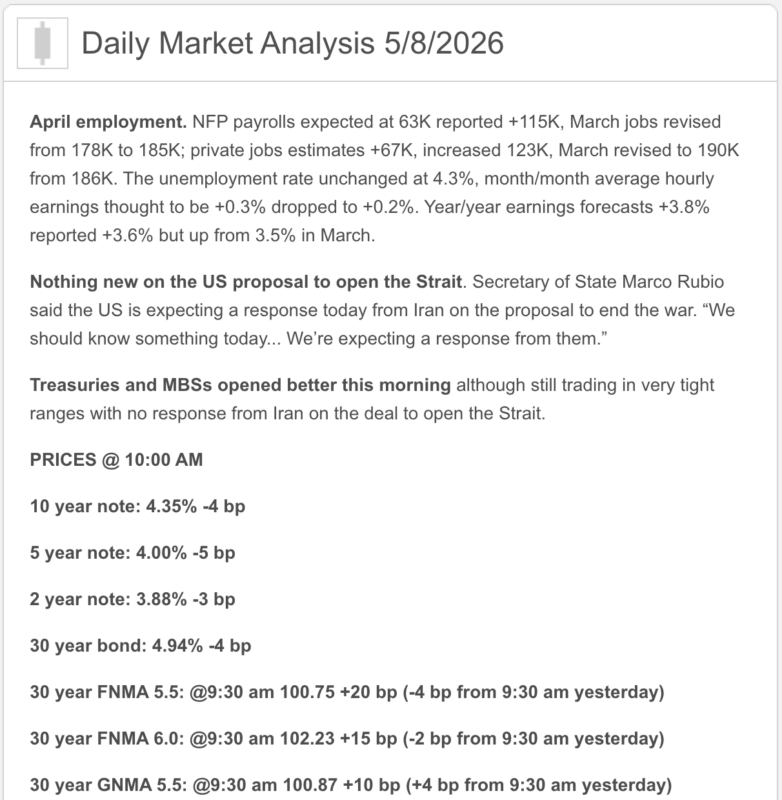

No matter the reason, we saw bonds go from up on the day to sold off, and it wasn’t any fun. The BLS jobs data came in stronger than expected this morning, with 115,000 new jobs instead of the 65,000 that were expected, although unemployment stayed at 4.3%. That should have pressured bonds at least a little bit… but didn’t. Instead, bonds have been improving all morning. Headlines about Iran will continue to drive markets, this morning the headlines say a response from Iran to President Trump’s latest proposal will come in today.

Will that happen? Who knows. Both sides seem to want to get this over with, yet both sides blather on.

Market Analysis – From a higher and better view:

Market Analysis –Quick Snapshot

- Jobs came in better than expected. The U.S. added 115,000 jobs in April, above the 62,000 economists expected. Unemployment held at 4.3%, average hourly earnings rose 0.2% month over month and 3.6% year over year, and the average workweek edged up to 34.3 hours. Job gains were led by health care, transportation and warehousing, and retail trade, while federal government employment declined.

- There was a little softness under the hood. Reuters noted household employment fell, labor-force dropouts helped keep the unemployment rate steady, and the number of people working part-time for economic reasons jumped by 445,000 to 4.9 million.

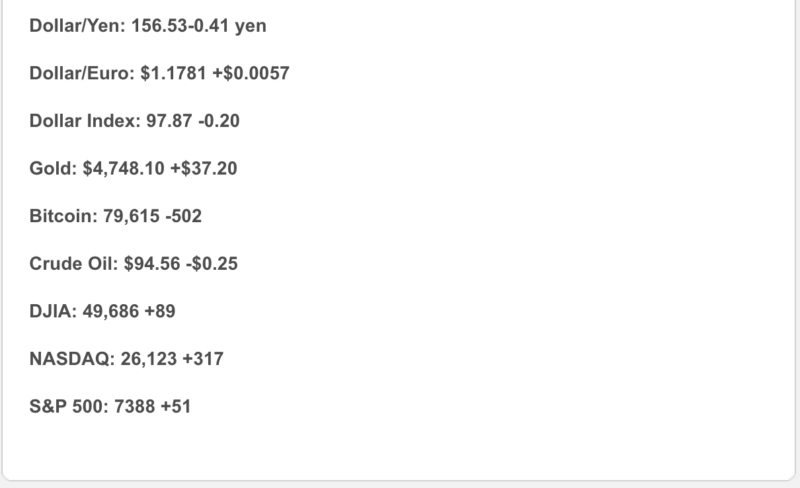

- Markets liked the report. At 11:44 a.m. ET, the Dow was up 0.05%, the S&P 500 up 0.74%, and the Nasdaq up 1.32%. The 10-year Treasury yield fell to 4.35%, and the dollar index slipped to 97.90.

- The Fed story is still “hold.” Reuters said the stronger jobs report reinforced expectations that the Fed will keep rates unchanged for some time, with markets leaning toward no near-term cuts.

- Mortgage rates moved up this week. Freddie Mac’s latest survey shows the 30-year fixed at 6.37% and the 15-year fixed at 5.72% as of May 7, both up from last week. Freddie Mac also said recent data still point to slightly better conditions for buyers thanks to better inventory and new-home conditions.

1) Market Analysis -What Hit This Morning

Today’s report was a classic “better headline than feared” number. Payroll growth was not spectacular, but it was strong enough to calm recession nerves and weak enough on wages to avoid a fresh wage-inflation panic. That is why stocks liked it and bonds did not melt down.

Narrative you can use:

“Today’s jobs report said the labor market is still holding up better than expected. That is good news for the economy, but it also means the Fed is not getting much pressure to cut rates anytime soon.”

2) Fed Watch

The big takeaway this morning is simple: a decent jobs report plus still-elevated inflation keeps the Fed on hold. Reuters said the April jobs data reinforced the view that rates will stay unchanged for some time, and some market commentary is now leaning toward the Fed staying put well beyond 2026.

3) Where Mortgage Rates Actually Are (Market Analysis)

Freddie Mac’s latest published survey is now 6.37% on the 30-year fixed and 5.72% on the 15-year fixed. That is up from last week’s 6.30% and 5.64%, so mortgage pricing took a small step backward.

The bigger point remains the same: mortgage rates are still being pushed around more by Fed timing, inflation expectations, oil, and Treasury yields than by wishful thinking. Today’s jobs number supports economic stability, but it does not exactly hand borrowers an immediate discount.

4) Market Analysis -Housing Market Check

There was no major fresh housing release driving today’s tape. The best current read is Freddie Mac’s own commentary that higher inventory, stronger new-home sales, and lower median new-home prices than recent years are helping buyer conditions a bit, even with rates still in the mid-6s.

5) Market Analysis -Political Backdrop & Fed Independence

The market is still watching the Gulf. Reuters reported the U.S. was expecting an Iranian response to its latest peace proposal on Friday even as fighting flared in the region, and stocks were able to look past the tension for now because earnings and the jobs report were strong. Oil, however, remained above $100 a barrel, which keeps the inflation backdrop uncomfortably alive.

6) Market Analysis -What This All Means for Rates Going Forward

Base case: rates stay choppy and somewhat elevated because the labor market is stable enough to keep the Fed patient.

Better case: Middle East tensions cool, oil drifts lower, and upcoming inflation data cooperate.

Worse case: oil stays firm, inflation stays sticky, and strong labor data keep pushing the first cut farther out.

7) Practical Takeaways

For buyers, this is still a market where structure beats hope. The economy is not cracking, but rates are still high enough that monthly payment strategy matters.

For agents and partners, today’s report is constructive for confidence. The labor market is still standing, but not so strong that it screams overheating. The challenge is that “good for the economy” does not always mean “great for mortgage rates.”

8) Lock vs Float

0–15 days: lean lock.

15–30 days: case by case.

30+ days: cautious float, but only if the borrower can handle headline-driven swings. The Fed may be patient, but the market still is not.

Stay safe and make today great!