Good Tuesday morning from your Hometown Lender,

I hope you had a great weekend and took some time yesterday to thank those that have stood up for our freedom.

No data today but this will be a busy shortened week with CPI, PPI, Retail Sales, and a bunch of Fed speak kicking off tomorrow.

In anticipation, we are seeing bonds pull back a bit with rates up about .125% today. I think that is more about Bitcoin getting a huge steroid shot in the arm over the weekend with it topping 89k. It is on a tear and as often is the case, as Bitcoin surges (which is about the most volatile asset I can think of), bonds are less attractive and sell off. The data the rest of the week will either push us toward improvement or push us toward higher rates. Which do you think?

Speaking of rates, the MBA shared a good piece on the correlation of rates and the 10-yr note yield. It is worth a few minutes.

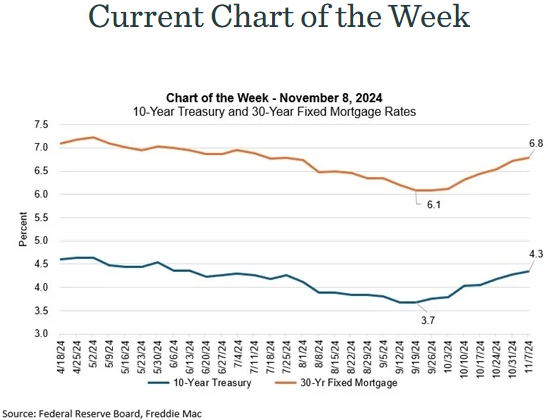

Both Treasury yields and mortgage rates declined from April to September 2024 in anticipation of the Federal Reserve’s first rate cut, influenced by the cooling job market and inflation moving towards the Fed’s 2 percent goal. The 10-year Treasury yield hit a low of 3.7 percent in mid-September and the 30-year fixed mortgage rate reached 6.1 percent.

However, rates began to increase in September shortly after the first rate cut, driven by stronger than expected economic data and expectations that further increases in government spending would add to an already historically large, federal budget deficit. In the last fiscal year, net interest payments on the outstanding debt exceeded spending for national defense.

Clearly, budget pressures are beginning to have an impact on market perceptions of future rates.

With a Trump victory, and particularly with what seems likely to be a “red wave,” there is likely to be somewhat faster economic growth, somewhat higher inflation, and larger deficits than what MBA expected in its October baseline forecast, all of which leads to higher rates today. The 10-year increased to over 4.4 percent after election day (November 5th) and mortgage rates have reached 6.8 percent, based on Freddie Mac’s survey results released yesterday, with many market quotes above 7 percent.

The FOMC cut rates by another 25 basis points at its November meeting, noting that risks to its inflation and employment goals are “roughly in balance.” Financial markets fully anticipated this rate cut, and the FOMC’s statement provides no new information regarding the likelihood of future cuts.

MBA expects that the trading range for mortgage rates has stepped up reflecting this new reality, which will dampen refinance demand somewhat. For purchase activity, these higher rates come at a seasonally slower time for homebuying so there will be less of an impact. Housing markets continue to be primed for a stronger spring homebuying season, boosted by more housing supply and slower home-price growth.

Stay safe and make today great!!!